USD/JPY Forecast 2019: A barometer of global growth and markets

2018 saw contradicting forces eventually balancing each other and returning Dollar/Yen close to its starting line for the year. The robust US economy, Fed hawkishness, the detente around North Korea and rising bond yields supported the pair. Fears about international trade, a global downturn, Brexit, and hiccups in stock markets kept the pair depressed.i

2019 will likely see a resynchronization of the US with the rest of the world. USD/JPY will probably encapsulate the prospects for the whole world, with all the other central factors such as the Fed policy, stocks, and bonds all aligned. All in all, this currency pair is set to serve as a global barometer.

2018 - 1000 pips round trip

At the time of writing, in the last month of the year, USD/JPY is within some 100 pips of its price at the end of the year. However, the story is more complicated.

At the wake of 2018, it was unclear how the US economy would react to Donald Trump's tax cuts and the extra spending by the government. Moreover, Janet Yellen was still at the helm of the Federal Reserve, and conventional wisdom was that Jerome Powell would provide continuity and nothing else. Also, to top it off, Trump was still exchanging insults with North Korean Leader Kim Jong-un. A stock market crash in February triggered a significant risk-off sentiment that was well reflected in USD/JPY falling below 105.

A recovery in the stock market marked the beginning of substantial improvement. By the spring, the US economy was blossoming, enjoying a growth rate of 4.2% annualized, last seen in 2014. Moreover, it became clear that the Fed under Powell, with a new composition, was more hawkish than beforehand. Besides, relations between South Korea and the rogue regime up north warmed up and eventually led to a historic summit between Trump and Kim in June. The olive branches diminished demand for the safe-haven Japanese yen. The pair not only pared its losses but completed a gain of around 1,000 pips, nearing 115.00.

Yet while Washington offered olive branches to Pyongyang, relations with Beijing deteriorated. The Administration slapped tariffs on Canada, Mexico, the European Union, Japan, and also China. A trade truce was reached with Europe in July, and a new trade deal was reached in North America, called USMCA, in October. However, Trump hit China with new duties, and the world's second-largest economy struck back.

Vice President Mike Pence outlined a long list of US grievances in early October, and this coincided with jitters in stock markets, signs of slowdown outside the US, fears that the Brexit deal will not pass, an ongoing clash between Italy and the EU, and no progress around North Korea. All these adverse developments weigh on USD/JPY.

The year ends with a balance between a still resilient US economy and a hawkish Fed on the one hand, and a global slowdown, and trade uncertainty on the other side.

In this overview of 2018, one factor may seem absent when talking about USD/JPY: the Bank of Japan. Inflation remained depressed in the Land of the Rising Sun, resulting in only minor tweaks in the policies of the Tokyo-based institution. At one point, Prime Minister Shinzo Abe suggested that loose monetary policy is not forever, but BOJ Governor Haruhiko Kuroda ignored it.

2019 - a more synchronized year

As mentioned in the introduction, we may see a re-synchronization of the world economy, stocks, trade policy, and the USD/JPY currency pair.

Here are the factors to watch in 2019

Fed to pause at some point

Markets have doubts if the Fed will raise rates in 2019, but these doubts seem exaggerated. Powell and the new voting composition of the FOMC will likely raise interest rates at least once and perhaps twice. However, these could be dovish hikes.

The Fed has two mandates. Inflation is not running too hot and nor are inflation expectations. Employment is advancing at a healthy pace, but the low participation rate continues implying that full employment is not that close.

Other economic indicators also point to a slowdown. Home sales are softening, and investment has not been ramped up despite the tax cuts.

After four hikes in 2018, the central bank may decide to take a pause and see the impact of its moves. Monetary policy reaches the economy with a lag and Powell may pause.

More importantly, in a globalized world, the US cannot remain immune to the global slowdown for too long. And the same goes for the central bank.

When the Federal Reserve stops standing out in its hawkish stance, the US Dollar will likely peak. While a consequent advance in stocks is positive for USD/JPY

Trade will keep on talking

Trade will likely remain a dominant theme also in 2019. The first date to circle is March 2nd when the 90 days from the declaration of the US-Chinese trade truce expires. This date may move, but relations between the world's largest economies will continue having a considerable impact on the global economy, equity markets, and USD/JPY.

The US shares grievances about China's practices with other countries which will undoubtedly be glad if the Middle Kingdom opens up. However, Trump managed to anger allies with duties and also by describing them as foes.

While the US President wants to move forward with balancing the enormous trade deficit, he also cares about the performance of stock markets. If he goes too far with China, shares could slide, and he may slow down his efforts.

China suffers more than the US from the trade war. An authoritarian regime needs content citizens and stability in order to maintain order. However, President Xi may choose to play on time or play the long game, waiting for markets to reverse Trump's efforts and waiting for him to go away.

Therefore, while China has more to lose from the ongoing tensions, it may have better cards in the negotiations.

For USD/JPY, the better things get, the higher it goes. The worse relations get, the lower it goes.

US politics and fiscal policy

Trump passed the massive cuts in 2017 under a unified Republican government. He kicked off the trade war in 2018. One missing piece from his economic promises is infrastructure spending. While Congress is split, Democrats have been supportive of infrastructure spending that the US needs. A massive government investment plan could boost the US economy alongside stocks, and USD/JPY.

However, there is a dearth of bipartisanship in Washington. Trump and Pelosi clash quite frequently. Various politicians from the Democratic Party have expressed their desire to open investigations on Trump's business dealings, his conflicts of interest, actions that the Administration took, and other issues. They are happy with their subpoena power.

Also, the Mueller investigation into Russian involvement in 2016 continues at full force and some in the Democratic base are calling for an impeachment of Trump. During the course of 2019, several politicians will present themselves as presidential candidates, some adhering to the base.

Yet the American public is not supportive of ousting Trump and Trump prides himself as a dealmaker. He could strike a deal with Dems that would keep him safe from unpleasant probes while the opposition gets to advance their priorities. At the current environment, this sounds remote, but anything can happen in politics, such an accord could lift the pair.

Stocks, bonds - it is all there

The Fed, trade, and politics will likely be well-reflected in the value of shares, with the S&P leading the way, and in bonds. The benchmark 10-year Treasury bond yield is the leader, but if the economic situation deteriorates, the yield curve will grow in importance.

An inversion of the yield curve has been a reliable indicator of a looming recession down the road. The financial world is focused on the 10-2 spread, which narrowed to single digits of basis points in late 2018. In 2019, the 10-year /3-month yield will likely grow in importance, as it has proven to be a better gauge of a recession.

The correlation between stocks, bonds, and USD/JPY will likely tighten in 2019.

Abe's legacy

The Bank of Japan will likely continue its loose monetary policy as inflation remains low and the 2% core inflation target remains elusive. Small tweaks to the QQE policy are unlikely to move the needle for the pair.

However, the Japanese government may have a greater say. Prime Minister Shinzo Abe is entering his seventh year as head of state and may be in his final term at the helm. The veteran politician may try to set his legacy.

"Abenomics," Abe's economic plan, consisted of three "arrows": monetary, already delivered, fiscal, mostly delivered, and reforms, in which he lagged. Without any noteworthy opponents within his LDP Party or the opposition DJP, he may push with changes to the economy that will boost the economy. That could strengthen the yen.

The boldest move would be to open the country to immigration. With an aging and shrinking population, growth and inflation could be seen alongside a boost to the population. Consequently, the yen could rally as well. Such a move has meager chances. The Japanese society may not be ready for a radical change, and the global backlash against immigration does not help either. However, given Abe's grip on power and his desire to make his mark, such a move cannot be ruled out.

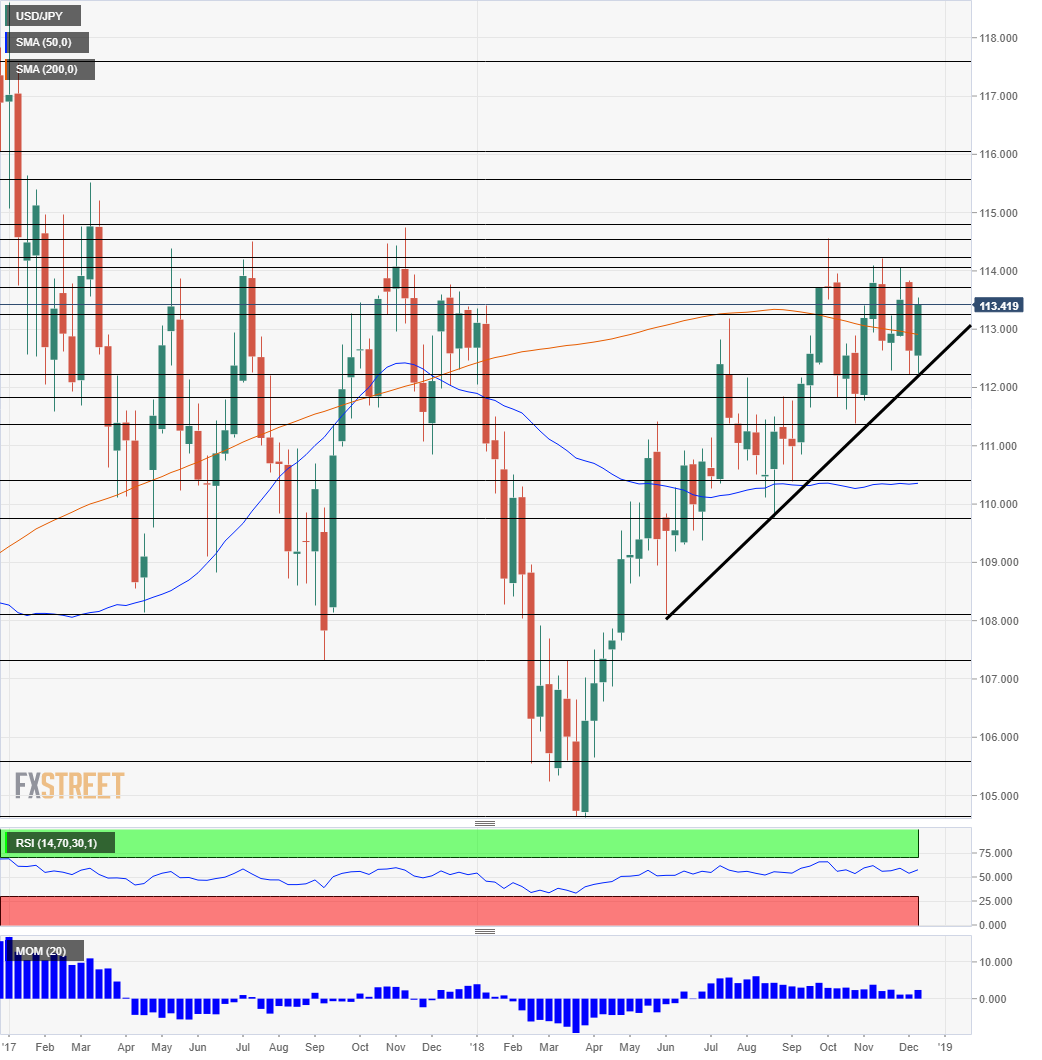

USD/JPY Long-Term Technical Analysis

For this yearly outlook, we use the weekly chart to get the big picture. The pair trends higher since bottoming out early in the year but has gone sideways in recent months. It holds onto uptrend support (thick black line on the chart). USD/JPY is trading above the 50-week Simple Moving Average after falling below it earlier this year. The 200-week SMA is well below the current price.

However, Momentum waned and the Relative Strength Index (RSI) does not point to any direction.

Here is a broad range of technical levels to watch from top to bottom:

118.70 was a peak back in December 2016. 117.60 capped the pair in early 2017, when it was heading lower.

116 is a round number that also served as support in late 2016. Close by, 115.60 was a support line in March 2017.

114.80 was a peak in November 2017 and the next line is already from this year: 114.55 which was the 2018 peak seen in October.

The following levels are from more recent times. 114.25 was a high point in November and so was 114.05 in its vicinity.

113.70 was a substantial cap back in December 2017. 113.25 held the pair down in the summer of 2018. 112.20 was a low point in December and 111.85 held it down at the end of the summer.

111.30 was the low point in October and 110.40 was a swing low in September. Below the round number of 110, 109.70 was the trough of August.

Much lower, 108.10 is where the uptrend support line began back in June. 107.30 shows us back to a critical swing low in September 2017.

105.60 provided support in March and the last line to watch is the 2018 low at 104.60.

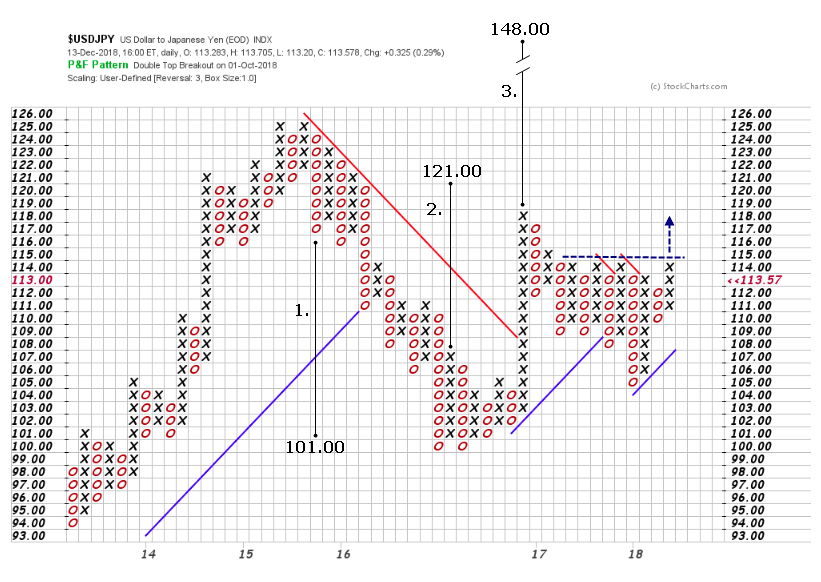

Gonçalo Moreira, CMT, applies Point and Figure analysis and eyes the 115 level as a key hurdle for an upside potential:

USD/JPY Point & Figure Chart

Count 1 has already reached its target at 101.00 a year later from its origin in 2015. The following year, an upward projection emerged from the reversal at the 100.00 level announced the 121.00 could be reached in the future. It almost reached that projection with an impressive upward column at the end of 2016, giving birth to the vertical count 3 which still has an unfilled higher projection at 148.00. A break of the 115.00 hurdles would increase the odds of the higher projections being filled.

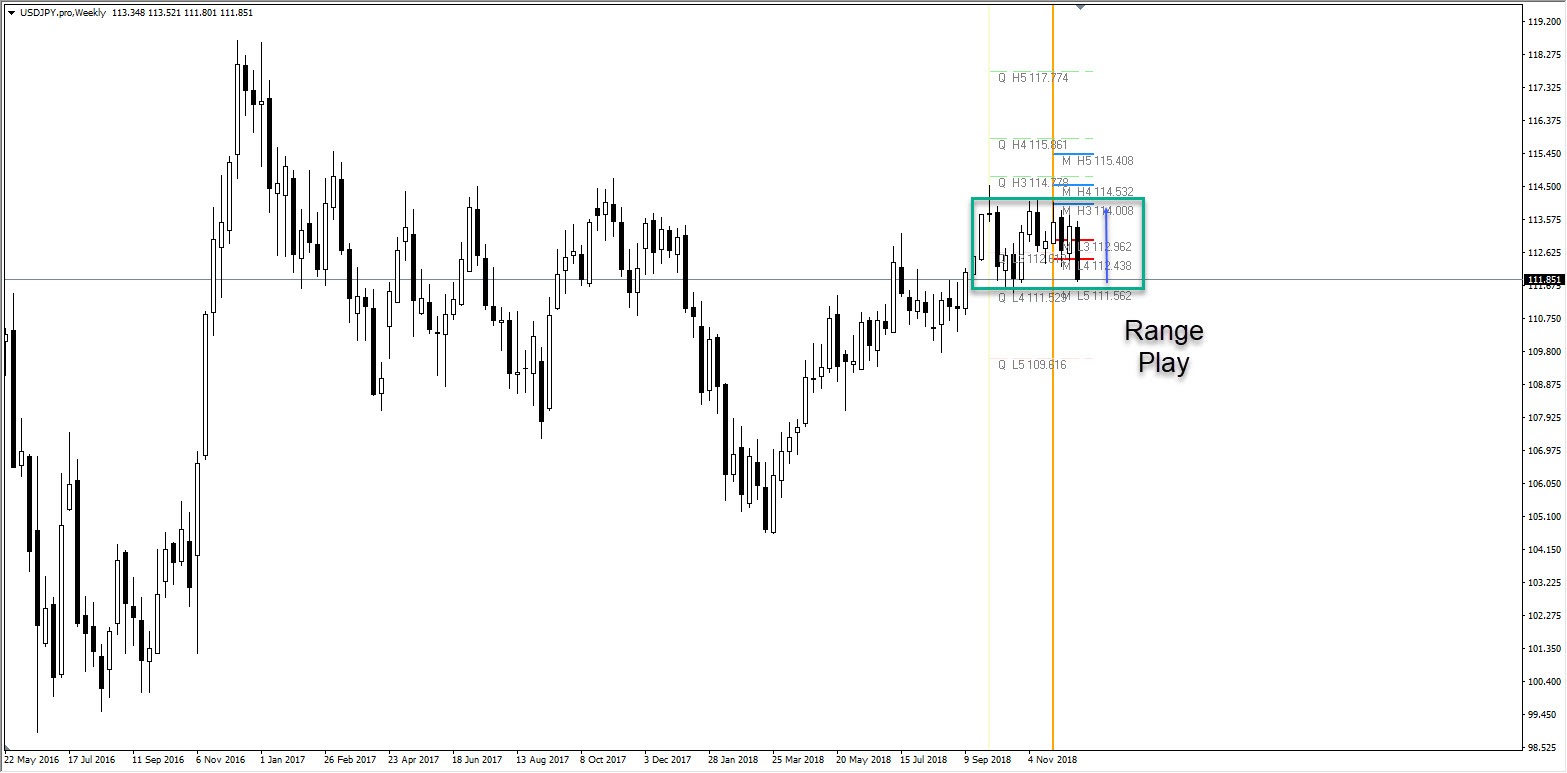

Nenad Kerkez provides his Camarilla Pivot Point Forecast sees some pressure in Q1 and a potential bounce in Q2:

USD/JPY Camarilla Pivot Point Forecast

See these clustered pivot points. This is suggesting another range play on this pair. I would say 111.50 could be the target for Q1 then we might see a bounce during Q2. Q2 target is 114.00. Honestly, trading the USDJPY is boring to me. I do trade but its ATR is so small, it’s really boring to trade it. We have much better markets to focus on.

Conclusion

After the US led the way in 2018, a resynchronization with the world is on the cards. A looser Fed policy could weigh on the greenback but support stocks, thus pushing the pair higher. Trade tensions may ease due to pressure from the stock market. US Politics will remain fascinating under a split government and a potential for infrastructure spending and ongoing legal troubles for Trump. And all in all, the correlation with stocks and bonds will likely strengthen. All in all, a lot of moving parts should be factored in.

Forecast Poll 2019

| Bullish | 37.5% |

|---|---|

| Bearish | 43.7% |

| Sideways | 18.8% |

| Average Forecast Price | 111.23 |

| EXPERTS | 1 YEAR |

|---|---|

| FXOpen team | 111.00 Sideways |

| Dmitriy Gurkovskiy | 120.20 Bullish |

| Brad Alexander | 118.00 Bullish |

| ForexGDP Team | 122.00 Bullish |

| Dmitry Lukashov | 123.00 Bullish |

| Chris Weston | 110.00 Bearish |

| Stoyan Mihaylov | 100.00 Bearish |

| Chris Svorcik | 107.50 Bearish |

| Nenad Kerkez | 113.30 Bullish |

| Joseph Trevisani | 110.00 Bearish |

| Ed Ponsi | 115.00 Bullish |

| HotForex Team | 114.00 Bullish |

| George Hallmey | 77.63 Bearish |

| Gianluca Privitera | 107.00 Bearish |

| Alberto Muñoz | 119.00 Bullish |

| Yohay Elam | 112.00 Sideways |

| Walid Salah El Din | 116.00 Bullish |

| OctaFx Analyst Team | 112.00 Sideways |

| Jeff Langin | 108.00 Bearish |

| Scott Barkley | 120.00 Sideways |

| TD Bank | 107.00 Bearish |

| ING Bank | 105.00 Bearish |

| Danske Bank | 115.00 Bullish |

| National Australia Bank | 106.00 Bearish |

| Royal Bank of Canada | 125.00 Bullish |

| WestPack Bank | 112.00 Sideways |

| Banque Nationale du Canada | 113.00 Bullish |

| La Caixa | 105.00 Bearish |

| BNP Paribas | 100.00 Bearish |

| BMO Capital Markets | 110.00 Bearish |

| CIBC Bank | 106.00 Bearish |

| Brown Brothers Harriman | 120.00 Sideways |

RELATED FORECAST 2019

EUR/USD: At the starting line of a long and bumpy road

GBP/USD: Imprisoned by Brexit darkness Sterling is set to chart a check mark

AUD/USD: Collateral damage from the US-China trade war

USD/CAD: CAD comeback on the cards

USD/MXN: Volatility set to remain elevated

Gold: Focus on US real interest rates

Oil: Dwindling demand and substantial supply likely to pressure petrol

The United States Economy and Politics: The return to a bipolar world

The European Union Economy and Politics: Conflict at home

China and International Trade: The crossroads of a great power

Dollar Index: A stumble is not a fall

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.