The European Union Economy and Politics in 2019: Conflict at home

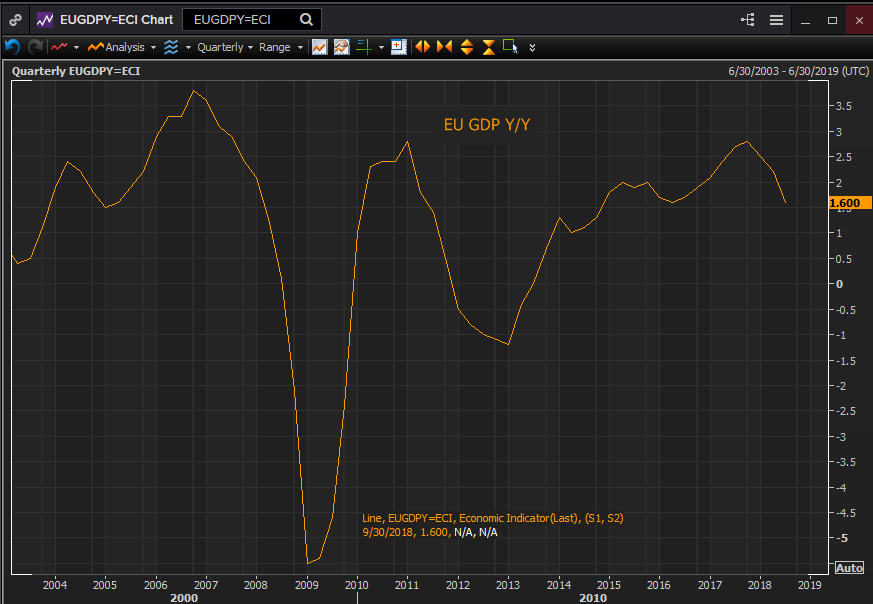

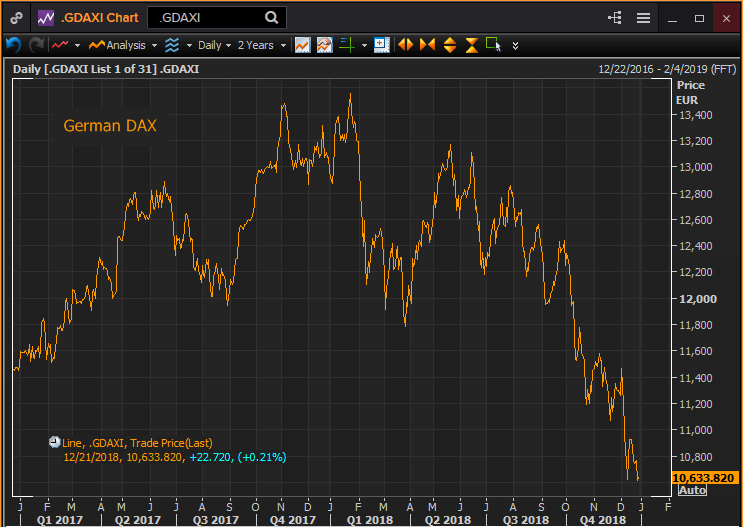

The European Union began 2018 in reasonable economic condition. Growth in the fourth quarter of 2017 had reached 2.8% annually, matching the best since the financial crisis. Unemployment in January was down to 8.6% from 9.6% a year earlier. Industrial production in December 2017 was 5% higher on the year. The European Central Bank had cautiously begun to reduce its bond purchases which it proposed to terminate at the end of the year citing the improving economic picture. Even inflation the problem child of EU statistics rose sharply in the second quarter from 1.2% in April to 2% in June.

By the end of the third quarter the economic picture had darkened. Growth declined steadily, 2.5% in the first quarter, 2.2% in the second and 1.6% in the third. Unemployment improved to 8.1% in July then stalled. Industrial production reversed sinking to 2.4% in February and continuing down to 0.5% by July, only recovering to 1.2% in October. Inflation touched 2.2% in October then slipped to 1.9% the next month. ECB optimism turned to renewed caution.

Reuters

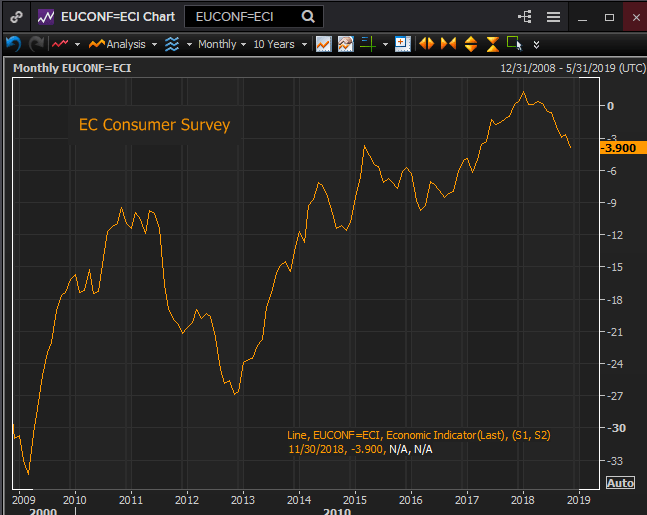

Sentiment indicators had collapsed. The Sentix index of investor attitudes dropped from 31.1 in December 2017 to -0.3 a year later. The Economic Sentiment Index from the EU Directorate for Economic and Financial Affairs fell from 115.2 in December 2017 to 109.5 eleven months later. The industrial outlook skidded from 9.7 to 3.4 in November 2018. Consumer confidence had plunged from 1.4 in January 2018 to -3.9 by November.

Reuters

At the same time economic growth in the world’s other major centers the United States and China improved or dropped just slightly.

In the US GDP rose from 2.2% in the first quarter to 4.2% in the second and 3.4% in the third. China’s GDP inclined from 6.8% in the first quarter of 2018 to 6.5% in the third, largely under the flail of its trade dispute with the Washington. The OECD May forecast for 3.7% global growth in 2018 and 2019 had fallen slightly to 3.5% for 2019 by November.

The most direct explanation for the about turn in the EU economy is politics. The Italians had elected an overtly euro-skeptic government in the heart of the European Union.

Two endemic problems of the EU, the uneven distribution of prosperity and the rules and regulations of the EU Commission, long sources of resentment for many, had finally found a political voice that could not be ignored or silenced. Coupled with the British exit, an English language version of the same set of complaints, the potential for economic and political disruption of the EU soared.

Origin of the European Union

The challenge for the EU went deeper than the immediate confrontation with Italy and the United Kingdom. The political forces represented in Rome and Westminster are present throughout the EU.

The European Union was founded as the European Coal and Steel Community in 1951 to prevent the repetition of the calamitous first half of the 20th century. It has been remarkably successful. Another European war is unthinkable.

But its founders had a more encompassing purpose. They desired to create a federal Europe. The method chosen was to build an organization that slowly enmeshed its national units in an irrevocable web of economic reality. Departure, as the UK is discovering, would be extremely difficult.

The creation of an economic bloc that serves its citizens and is rewarded with their loyalty has proven elusive. While the EU exists it does so largely without direct democratic approval. When people feel ill-served by the policies of the EU Commission, they don’t address their questions to the parliament in Brussels, they turn to their national government for relief.

It will be a serious challenge for the EU to placate the unleashed political forces now that they have tasted power and sensed the weakness of the establishment. European economic growth will suffer as the continent turns its attention and energies inward to its political future

We will look at several of the countries whose politics have been transformed by these conflicts, assess the economic and political impact on the EU and measure their interaction with the global economy and ECB policy.

European Politics:

The old gives way to what?

Italy, France and Germany, the central countries of the EU, have held national elections in the last two years and each in a different way has spectacularly upended the post-war status quo.

In March of this year the Italians voted in an unusual coalition of left and right parties, the 5 Star Movement and the League, on promises of economic revival. Between the anti-establishment 5 Star at 32.9% and the League, formerly the anti-immigration Northern League at 17.4% just over half of the electorate approved of two parties which had never held national office. After three months of negotiation a joint administration of Luigi Di Maio of 5 Star and Matteo Salvini of the League took over in Rome.

In May 2017 France elected political neophyte Emmanuel Macron at the head of a new party En Marche purposefully formed to escape the taint of the Socialists and the Republicans. In the run-off against Marine Le Pen of the National Rally, Macron, Minister of the Economy under the previous Socialist President Hollande, captured two-thirds of the vote.

Germany’s Chancellor Angela Merkel, Europe’s longest serving head of state, did not lose her post in the September 2017 elections but her Christian Democratic Union (CDU) lost 65 sets in the Bundestag and 8% of their prior vote receiving just 33% in the biggest swing in post-war politics.

The Social Democrat Party their erstwhile coalition partner before the election had its worst result since the Second World War getting just 20% of the vote. Alternative for Germany (AfD), a four year old conservative nationalist party won 12.5% and their first ever representation in the Bundestag at 94 seats. It took almost six months for Ms Merkel to engineer a functional coalition with the Social Democrats who had rejected her initial offer and after a failed attempt with two smaller parties the Greens and the Free Democrats. It was the longest government interregnum in post-war German politics.

The specific issues in each country were different. In Italy it was dissatisfaction with the economy stagnant since the financial crises and the inability of successive national government to improve its performance.

In France the outgoing President Francois Hollande had the lowest approval of any president since the Second World War, disapproval of his economic and immigration policies being the largest parts of his unpopularity. He chose not to run for re-election becoming the first French President to decline eligibility. Macron’s victory was assisted by the timely destruction of the Republican candidate Francois Fillon’s campaign in a political scandal.

In Germany Merkel’s immigration policy that opened the borders to two million Middle Eastern and African immigrant proved to be a spectacular miscalculation. It was the direct cause of the failure of the CDU and the rise of the AfD.

The common thread of the three elections was the electorate’s exasperation with the governing classes and its willingness to reach for new and untried parties and leaders. It is notable that Italy, the country with the worst economic record had the longest grasp, installing two new national parties in Rome.

European Political Economy:

Elections have consequences

If we construct a timeline of the three elections France is first voting in Macron in May 2017. Next is Germany with the federal election in September of the same year. Italy is last with its March 2018 vote.

It was nearly six months before Chancellor Merkel took office on March 14th just ten days after the surprise in Italy. The new Italian government took up power in June. Sometime in the nine months between the German election in September 2017 and the Italian coalition installation in June many Europeans may have realized that the old politics were under serious threat.

The half way point in that period is the middle of February. Let us see how that compares with EU statistics.

As noted above GDP peaked in the last quarter of 2017 at 2.7%. Nine months later the third quarter came in at 1.6%. The three month moving average of retail sales registered 0.667 in November 2017, in October 2018 it was 0.067%. Annual figures show the same decline, 2.4% in January 2018 and 1.4% in October.

Unemployment across the Union was 8.6% in January. It dropped to 8.1% in July, and in October it was still there. That was the longest period without improvement in five years.

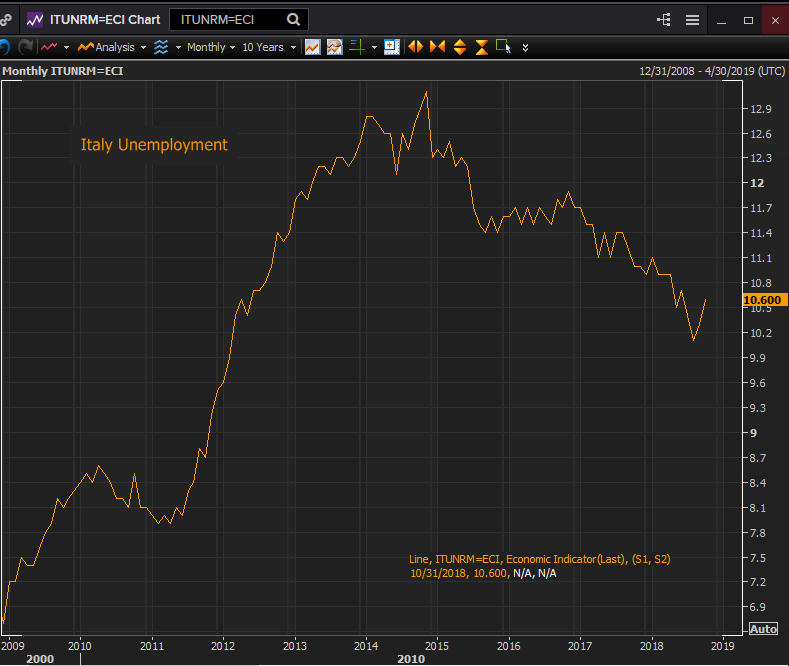

The unemployment numbers for the three individual countries vary. Italy’s are the worst. In January the jobless rate was 11.1%, by August it had fallen to 10.1%. But then in two months it lost half of the year’s advance jumping back to 10.6%. In France the rate in the fourth quarter of last year was 8.9%. That rose to 9.2% in the first three months of the New Year and leveled at 9.1% in the second and third quarters. In Germany the unemployment rate moved from 5.4% in January to 5% in November.

Reuters

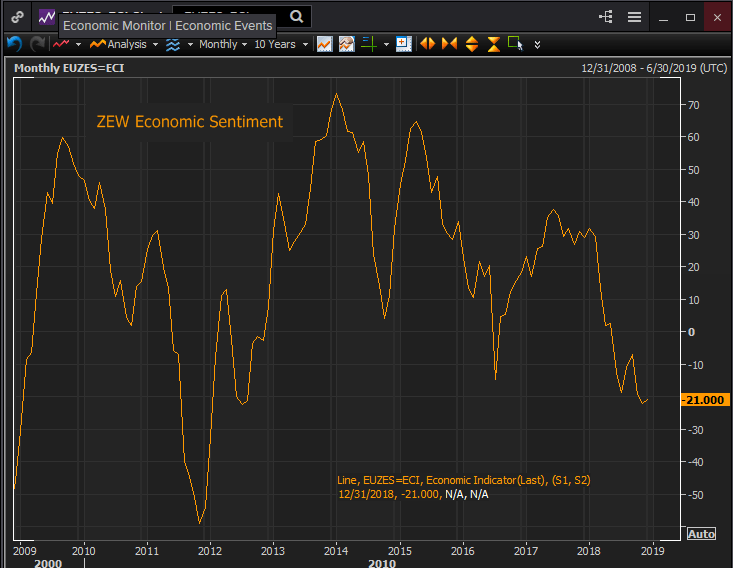

Sentiment indexes exhibited the same pattern across the EU. The ZEW Survey of economic sentiment was at 31.8 in January, in December -21.0. Consumer confidence surveyed by the EU Directorate was 1.3 in January, in November -3.9.

Reuters

Business attitudes took an even sharper tumble. Markit’s manufacturing purchasing managers’ index was 59.6 in January. In November it was at 51.8 just above the 50 contraction line. Services dropped from 58.0 in January to 53.4 in November.

Naturally there was more happening in the world than just European elections that might have affected business and consumer attitudes. The event closest to home was the departure of the UK from the EU.

British media was replete with assertions that a no-deal exit would be a catastrophe for the UK economy. The continental media less so. Attitudes on the European side of La Manche seemed to partake of the confidence of the EU Commission that the economics of Brexit were a British problem.

The trade dispute between the US and China was also a media favorite. But while it might give American manufacturers and importers headaches it has little bearing on Europe. In the last quarter equities were pummeled in Europe as elsewhere and were a serious market concern but the European economic malaise had begun in the first quarter not the fourth.

Reuters

Despite a busy world the origin of the EU’s economic decline in 2018 was home grown.

EU Economy in 2019:

Paying the piper

The primary question for the EU economy is whether the New Year will bring a recession. The omens are not good. Economic growth in the 28 member organization has declined sharply in the first three quarters from 2017’s close at 2.7% to 1.6% in the third quarter of this year. Quarterly expansion has halved from 0.4% to 0.2%. It is possible that when GDP figures for the final three months of 2018 are reported on January 31st a contraction will have started. German growth was already -0.2% in the third quarter, Italian GDP was flat.

Sentiment indicators saw the sharpest deterioration. Several like the Sentix which dropped from 32.9 to -0.3 over the course of the year, the EC Consumer Survey which fell from 1.3 in January to -3.9 in November and the EC Manufacturing Confidence Indicator down from 9.7 to 3.4, had pitched from post-recession highs.

Herein lies the biggest problem for the EU. The political and economic news is not likely to get much better next year. Problems are rife in the EU’s four largest economies.

In Germany for decades the power plant of the EU, growth has slowed. The country’s Council of Economic Experts expects just 1.6% this year and 1.5% next year. Part of the reason is that the country’s automakers are having trouble adapting to the EU targets for greenhouse gas emissions which may also be behind the third quarter contraction.

In France the violent and unexpected protests of the “yellow vests”, so–called for the safety vests all French motorists are required to carry, against President Macron’s fuel tax has upended the nation’s political calculations. The protests could halve fourth quarter GDP to 0.2% from 0.4%. Retailers are thought to have lost 1 billion euros in revenue since the protests began in November. President Macron’s surrender on the fuel tax has reduced but not yet ended the protest. It has however, reduced his leadership immeasurably.

The Italian budget dispute with the EU Commission seems to have been resolved with a compromise that lets both sides walk away pleased. The coalition government in Rome will spend about 2 percent of GDP to support the economy. That is less than their original 2.4% plan but far more than the 0.8% deficit promised by the previous Renzi government. Despite the agreement the coalition of 5 Star and the League remains euro-skeptic in origin and far outside the normal run of EU politics.

Finally there is the problem of Brexit. The uncertainty over the nature and even the fact of the UK exit will weigh ever more heavily as the March 29th departure approaches. EU and national officials on the continent have to know that an unregulated exit would be as damaging for the EU as for the UK. A recession on both sides of the Channel would result. One can only hope that the EU Commission’s intransigence is a negotiating tactic and not economic insouciance.

It is true that in high stakes negotiations compromise often takes place at the last minute. But the run up to that minute, and the ever more frantic emergency planning, even if an agreement is forthcoming will be nerve wracking and damaging for the economies on both sides.

European Credit Markets:

Surprisingly stable

One of the surprises in the second half of the year was the lack of market excitement over the Italian budget dispute. At its height in September and October rates on the Italian 10-year bond approached 4%, a level that if sustained could cause serious problems for Italian government finances. The moment was brief and there was no contagion in EU credit markets. Spanish, Portuguese even Greek rates responded minimally if at all. The Italian debt to GDP ratio of 132%, well beyond EU advice, is a problem for another day.

European Central Bank:

Will the wait be worth it?

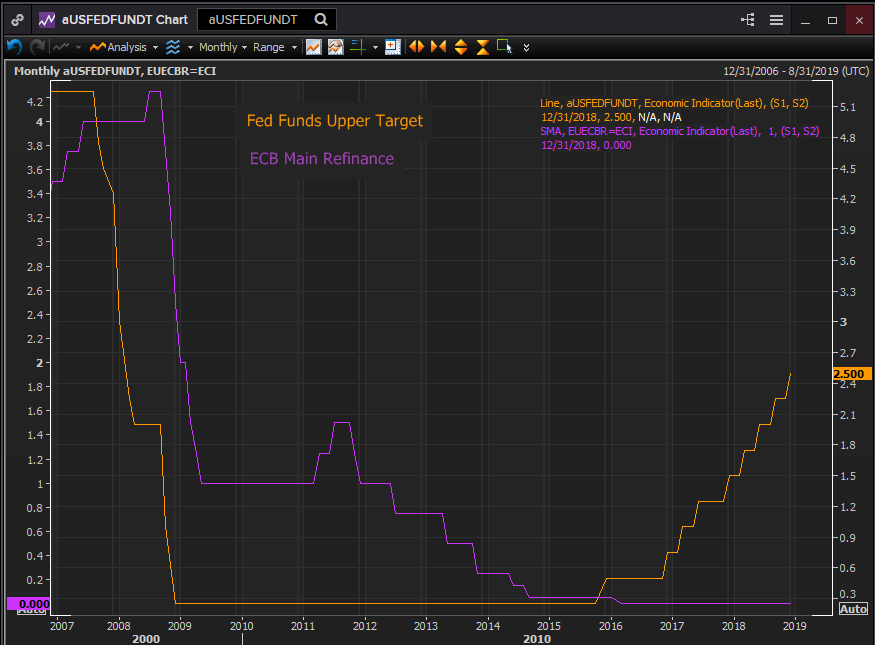

The ECB under Mario Draghi has prolonged its financial crisis response longer than any other central bank. The Federal Reserve began raising rates from the zero bound three years ago. The ECB is just ending it bond purchases this December.

Reuters

The Federal Reserve rate normalization program has been periodically criticized because at no point in the past three years has the US economy exhibited the need for higher rates. Inflation was quiescent, growth moderate, and wages were not rising.

The point of the Fed’s insistence on raising rates must be painfully evident to the ECB. If the US economy slows or if buffeted by external events, the Fed has a rate cushion. It is not perhaps as large as in the past or as a cautious FOMC might like but it is something. The ECB is still at the zero bound.

The duration the ECB program says a great deal about the unstated weakness of the EU economy of the past half-decade and of the recurring political and financial problems beginning with the Greek crisis that have kept the ECB as the EU’s backstop. It is a role the bank would probably have eschewed if it could.

If the EU economy slips into recession next year, a distinct possibility what can the ECB do? Will the bank revive its bond purchases within months of having ended them? Will it begin negative rates?

Euro Prognosis:

The counter to weakness

The European currency has been under pressure in the second half of 2018 from the Fed’s ongoing rate hikes and the self-inflicted wounds of Brexit and the Italian debt dispute. The EU agreement with Italy and the modest recent rise in the euro will be a temporary respite.

The united currency is facing a first half full of fundamental dangers. The intertwined problems of sharply slowing economic growth and the dangers of a disorderly Brexit will resume as soon as the year changes. If the euro is in a slightly better position in relation to Brexit than the sterling, it is in a far worse situation related to the dollar. The US economy is stronger and the Fed can support growth if need be. The ECB cannot. The euro will pay the price. Parity is not out of the question.

Conclusion:

Global Risks and the European Union

The EU enters 2019 with a full case load of internal political and economic problems. Election results in Germany, France and Italy highlight the weakness of the traditional leaders and their policy responses. The electoral dissatisfaction that brought the euro-skeptics to power in Italy, humbled Angela Merkel in Germany and Emanuel Macron in France is founded in the uneven distribution of prosperity within the EU and within individual countries, and with immigration policies that seem to be beyond the reach of national governments.

Ten years after the financial crisis the Italian economy has not fully recovered. If the government in Rome cannot find a way to return growth within the structure of the EU, the time is approaching when the Italian voters will look for solutions outside the EU.

A serious recession in the EU will compound the antipathy many votes have for the traditional political parties. If street riots in Paris can force the French President to back down, if an anti-immigration party is the fastest growing political force in Germany then the EU itself is not immune.

If the global economy stumbles and drags the EU into recession or if one arrives from the British exit or some other source the political ramifications for Europe could be more dangerous than mere economic dislocation.

Not all is gloom. Although internal stresses will put Europe in low growth or in the worst case recession the rest of the world is not automatically slated for a drastic slowing in 2019. The key is the US China trade dispute. If the world’s two largest economics can settle their disagreement their economics can power global growth. A strong world economy might keep the EU from recession but it will not solve the EU’s spreading political discord.

The risk for the EU is not outright defiance by national governments it is creeping desuetude. The model is not de Gaulle’s opposition to NATO but the League of Nations.

RELATED FORECAST 2019

EUR/USD: At the starting line of a long and bumpy road

GBP/USD: Imprisoned by Brexit darkness Sterling is set to chart a check mark

USD/JPY: A barometer of global growth and markets

AUD/USD: Collateral damage from the US-China trade war

USD/CAD: CAD comeback on the cards

USD/MXN: Volatility set to remain elevated

Gold: Focus on US real interest rates

Oil: Dwindling demand and substantial supply likely to pressure petrol

The United States Economy and Politics: The return to a bipolar world

China and International Trade: The crossroads of a great power

Dollar Index: A stumble is not a fall

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.