China and International Trade in 2019: The crossroads of a great power

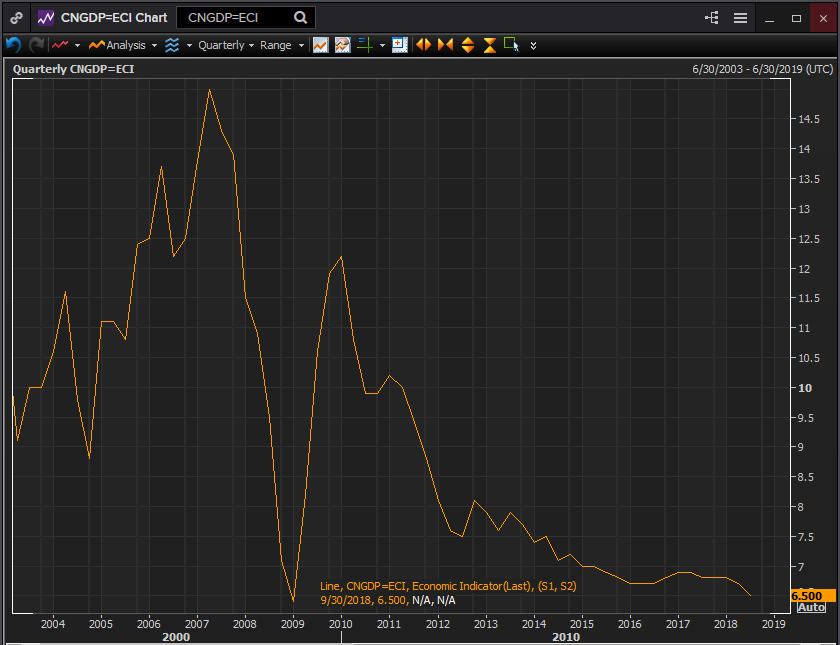

The Chinese economy was slowing long before Donald Trump decided to change the terms of trade between the world's two largest economies. China's last quarter of 7% expansion ended in June 2015. This year GDP has fallen from 6.8% in the first quarter to 6.5% in the third. Economic growth on the mainland has been slipping for most of the past eight years with only the occasional quarterly improvement.

The reason for that evolution is the Chinese economy is maturing. No economy, even one as dynamic as China’s has been over the past generation can maintain the frenetic 10.2% pace of the decade before 2008. The bigger the economy becomes the scarcer are the domestic opportunities for large-scale growth. Targeting foreign markets becomes more difficult as products move up the chain of sophistication and and expense.

A mass consumer society, much like the United States is the obvious answer. But with per capita income less than a third that of her Western competitor China's economy is far more dependent on the consumers of other nations than is the United States. Tariffs on imports may cost the American consumer a higher purchase price but they will not take many American jobs. For most of the products that the US imports from the mainland the only advantage is price. There are domestic or non-Chinese sourced alternatives for almost all Chinese goods.

Chinese Employment: Vulnerable to tariffs

For Chinese manufacturers replacing the US market, even if their sales decline is in percentages rather than absolute is much more difficult. There is no ready alternative to the US consumer in the time frame needed to preserve Chinese jobs. A prolonged trade dispute with the United States will cost mainland factory employment. The longer it continues the more workers will be furloughed. China's labor market is vulnerable to a prolonged tariff war with the United States.

After a generation of building up market penetration in the United States, China’s brands and US products manufactured on the mainland may find themselves replaced by competitors from elsewhere in Asia, Europe and the United States itself. With rising Chinese wages already pressuring the price advantage of mainland manufacturers Beijing’s economic planning divisions must be frantic that markets lost in the US will be difficult to recapture.

Global Trade: China vs the EU

The trade dispute with the United States is not the cause of Beijing’s long-term decline in growth rate but it is the source of the steep decline this year and the origin of the government’s largest worry leading into 2019. If the relationship with the United States is not restored, growth could slip to levels that Beijing finds extremely unsettling and unacceptable, and more importantly, could generate the type of domestic dissent that the authorities find dangerous to their rule.

The US-China trade issue is also the weightiest of the concerns for global economic growth, involving two of the world’s three largest economic blocs.

The European Union has its own share of problems from slowing growth and stagnant or falling populations, to the British exit, Italian economic discontent, political rebellions in France and Germany, immigration, disdain for EU rules in Poland and Hungary and the inability to make ECB policy work equally for all members.

Compared to the intractable problems in Europe the US-China trade dispute is amenable to solution.

First we will look at the state of the Chinese economy then examine the politics and economies of the trade issue with the United States and finally handicap the solution.

China's Economy: Climate cooling

Chinese economic activity and statistics have declined this year in whatever sector or type of metric is searched. Hard industrial and consumer statistics, sentiment numbers, trade, and retail sales have all edged lower. Government support for the economy has soared.

As noted above annual GDP dropped 0.3% to 6.5% in the third quarter from the first quarter’s 6.8% where it had been since the beginning of the second half in 2017.

The November growth in industrial output of 5.4% matched the lowest monthly growth since the financial crisis. The three-month moving average declined from 6.7% in April to 5.7% in November. This makes September, October, and November the weakest three months in China’s post-Deng history.

Industrial Output

The deteriorating production picture is seconded by the official purchasing managers’ indexes from the National Bureau of Statistics. The manufacturing index was 50 in November resting on the division between expansion and contraction. It was the weakest reading since July 2016. This gauge has been falling after posting 51.9 in April. The non-manufacturing index was 53.4 in November down from 55.3 in January.

NBS Manufacturing PMI

The private Caixin survey shows a similar decline. Manufacturing PMI dropped from 51.5 in January to 50.2 in November. PMI in services was down to 53.8 in November from 54.7 at the beginning of the year having dipped as low as 50.8 the month before.

Annual growth in retail sales skidded to 8.1% in November the smallest in over 15 years. China’s automotive market, the world’s largest is set for its first annual sales decline since the 1990s.

Retail Sales

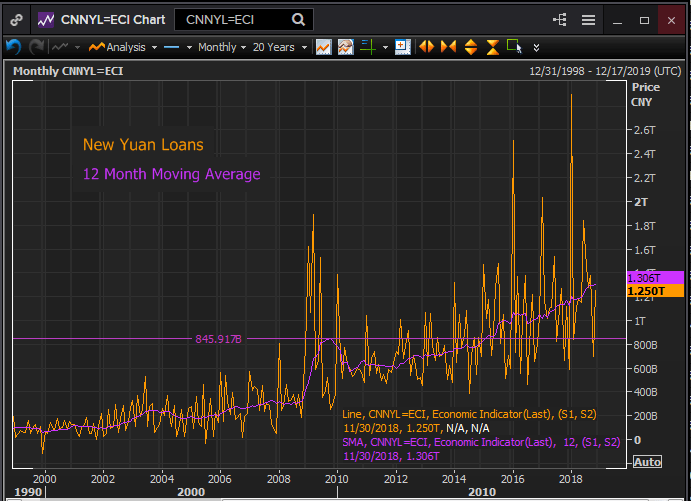

The industrial slide is in contrast to the dramatic surge in new yuan loans as the government attempts to stimulate the economy. The 12 monthly moving average of new credit this year of 1.306 trillion yuan is the highest on record. In the aftermath of the 2008 crisis, this average peaked at 845.917 billion yuan. New yuan loans have been above that level since July 2017.

The amount of money that the authorities are pumping into the economy in an effort to maintain growth is a sure indication of the underlying problems in the Chinese economy. The limited impact this deluge of cash has had on the economy is a sign that Beijing economic policy that has always favored industry and exports over domestic consumption has reached the limit of efficacy. What China needs are millions of people with the money and the disposition to spend on the products of Chinese factories. Unfortunately for the planners, factories are easier to build than a generation of free-spending consumers.

Foreign direct investment, another measure of industrial interest declined 1.3% in November, the first drop since last August.

Consumer inflation weakened to 2.2% annually in November, down from October’s 2.5%. From February 2017 at 0.8% CPI rose sharply to 2.9% a year later as the government’s directed loans washed through the financial system. The lack of sustained price increases is another measure of the inefficiency of the government’s attempt to maintain growth by expanding production.

China’s attempt to defend its economy from the impact of the trade dispute with the United States, while energetic and classically Keynesian does not seem to be having the desired effect. The Chinese consumer does not have the financial heft or consumption habits of his American cousins.

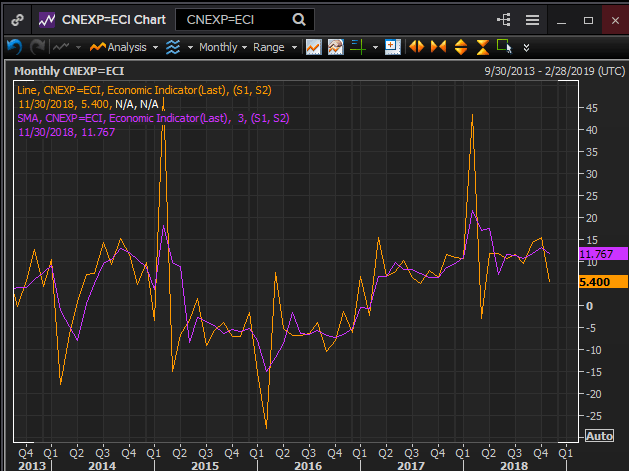

Chinese exports and imports have held up reasonably well. Annual exports were up 14.4% in September and 15.5% in October through they fell sharply in November to 5.4%. Imports, which includes many parts and items used in production for future exports also saw a precipitous drop to 3% in November from 20.8% in October. The three-month moving average for imports is at its lowest in 22 months.

Exports

The final gauge of the travails of the Chinese economy is the long slide of the Shanghai Composite Index, China’s largest stock exchange. Measuring from the June 2015 all-time high of 5,166.35 Thursday’s close (December 27) at 2,483.09 is a 52% devaluation. This year’s 30% drop is more indicative of the state of investing in China and the profound concerns many have for the economy than the fall from the bubble heights of 2015.

Trade Wars in Context: Both can win or lose

The trade dispute between the United States and China is one of the chief concerns hanging over the global economy in 2019. A healthy relationship feeding growth in the world’s two largest national economies would be strong enough to overcome a serious slowdown or recession in Europe.

European Union expansion will be stymied by the economic and political impact of the French street rebellion and the German political one, the uncertainties or perhaps dire certainties of the British exit, and the wait for the outsider coalition in Rome to revive the Italian economy.

The trading relations of China and the United States, in reality her interaction with all the technologically advanced states of the West and Asia, was founded in an earlier era when China was truly a developing nation and no economic threat to its trading partners. It was in everyone’s interest a generation ago to bring China into the political and economic mainstream of global culture. That has been done.

China is understandably reluctant to surrender practices that have served her economy well. That American President Donald Trump is the first leader of China’s trading partners to make a concerted effort to change the relationship to a more balanced system, may disguise the stake that all European, North American, Japanese, Korean and Taiwanese companies doing business in China have in his success. What the US achieves will soon be demanded by all of the mainland’s foreign investors.

US China Trade: Technology transfer is the rub

There are two main topics on the American trade agenda. Getting China to buy more US goods and services is the simpler task. As part of the truce agreed between the Presidents after the G-20 meeting in Buenos Aries, China has resumed and increased purchases of American agricultural products. Considering the efficiency and productivity of US farmers that is a win for both sides.

The second consideration, forced technology transfers as a price of Chinese market access and outright theft of industrial information by state and private actors, is a much more difficult prospect but one that is essential to the developed countries.

The primary advantage of American, German, Japanese and many other companies doing business in China is their technology. They are in China because it is still, in many cases cheaper to manufacture on the mainland. They are also there for access to China’s markets. The US Federal and many state governments encouraged Japanese, German and Korean manufacturers to build plants and jobs in the US. So does China. But China often demands that foreign firms enlist a local partner and that the Chinese firm have access to the proprietary industrial processes and technology.

President Xi Jinping’s very public “Made in China 2025” program to dominate a number of advanced industries probably had the unexpected effect of catalyzing opposition to China’s trade practices in the US government. On this one topic President Trump has the support of the Democratic leadership.

China in the New Century: Competitor and partner?

The confrontation between the US and China, may, depending on its outcome be a reversal of 40 years of American strategic policy. Since the two nations normalized relations in 1979 the US has assisted China’s entry into the world’s economic and political stages. The adoption by China under Deng Xiaoping of an essentially capitalist economy made US acquiescence relatively easy. It was assumed in Washington that making China an economic partner would also moderate the authoritarian traits of its central government.

While China’s economic ascent has been extraordinary her internal politics have changed little. Under President Xi, now President for life, China is less open and free than it has been in a decade. China has begun to assert her power throughout the Pacific, challenging the 75 year dominance of the United States.

The trade dispute is a barometer for the relationship that will emerge between the United States and China in the next decade, economically around the globe and militarily in the Western Pacific. The decision is largely China’s.

RELATED FORECAST 2019

EUR/USD: At the starting line of a long and bumpy road

GBP/USD: Imprisoned by Brexit darkness Sterling is set to chart a check mark

USD/JPY: A barometer of global growth and markets

AUD/USD: Collateral damage from the US-China trade war

USD/CAD: CAD comeback on the cards

USD/MXN: Volatility set to remain elevated

Gold: Focus on US real interest rates

Oil: Dwindling demand and substantial supply likely to pressure petrol

The United States Economy and Politics: The return to a bipolar world

The European Union Economy and Politics: Conflict at home

Dollar Index: A stumble is not a fall

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.