The United States Economy and Politics in 2019: The return to a bipolar world

The United States economy broke out of its decade-long slough in 2018 with its strongest growth since the financial crisis and recession. Unemployment declined to the lowest level in a generation as the labor market steadily produced more jobs than could be filled. Manufacturing, said by many to be a dying sector had its best year in a quarter century. Equities reached an all-time high then gave back the entire year’s advance in two months. Domestic oil drillers pumped more crude than had ever been extracted on the continent making the United State an energy exporter for the first time in 40 years. Inflation remained under control. As Jerome Powell, the Chairman of the Federal Reserve said near the end of the year, “These are the good times for the US economy.”

There was no shortage of concerns. China and the United States engaged in competitive tariffs as the Trump administration tried to change decades-old trade practices between the world’s two largest economies. Global economic growth weakened as the year aged dragged lower by slowdowns in China and the European Union. The EU was captivated by the Brexit drama, the Italian–EU Commission budget spat and in December French street protests which forced President Macron to rescind his fuel tax along with most of his popularity.

The Federal Reserve’s three-year-old effort to return interest rates to a normal range after seven years at the zero bound courted fears that the central bank would put an end to the economic expansion. While last year’s tax reform bill and the continuing reductions to government regulation provided an undoubted boost to the economy it was unclear whether they would result in a sustained level of higher growth.

Domestic US politics remained acrimonious with Democrats objecting to virtually every Republican initiative. Control of Congress and the Presidency by the Republicans did not result in a GOP sweep of legislation with some of the most telling opposition to President Trump’s policies as with the defeat of health care reform coming from within his own party.

The change of control in the House of Representatives after the November election which will give the Democrats legislative power for the first time in four years promises to complicate the political picture in 2019 and 2020.

Economic trends in the US at year-end appeared vibrant but with a number of potentially damaging developments in the global environment and domestic politics that could inhibit or thwart continued success.

We will look at the political changes first, assess the state of the US economy as reflected in statistics then ascertain the likely impact of domestic and global conditions on the US economy and Federal Reserve policy.

US Politics: Elections have consequences

The Democratic victory in the House will become a major distraction for the Trump administration. With certainty, various House Committees will open investigations into the President, members of his administration and his family. Whether the inquiries are justified is a political question and irrelevant. They and the subpoenas they will issue are legal and will have to be answered by the administration. This will be a burden on its time and impede the functioning of the executive. From a political perspective that is one of their main purposes.

If the House decides to draw up Articles of Impeachment and provokes a Senate trial this will further drain the resources of the Trump administration. The potential for the President to be convicted in a Senate trial and removed from office is very small. The bar for conviction is a two-thirds majority of the 100 member Senate. There will be 53 Republicans, the President’s party in the upper house in 2019

The Democratic and Republican agendas will find little common ground in the House next year where all budget bills must originate. It will be a major challenge for the leadership of both parties simply to pass the necessary budget bills to fund the operations of the government.

There will be few initiatives of either party passed into law. Democratic bills from the House will die in the Senate and Republican ideas from the Senate will terminate in the House

Gridlock on Capitol Hill is not necessarily bad for the economy. If no beneficial legislation is passed neither is anything detrimental enacted. The equity markets have a good record in divided Congresses. This may be especially true next year as the tax bill of 2017 will continue to provide economic benefits and the administration’s regulatory reform and other executive policy changes will continue unimpeded.

The major political threat to the economy is psychological. Will the rhetorical and legal contests between the parties in Congress and between the Democratic House and the Trump administration become so damaging that they undermine the business and consumer optimism in the country at large? The nation has a good history of ignoring the political squabbles in Washington. But the din next year will likely be unprecedented since the resignation of Richard Nixon in 1974.

US Economy: The past is prologue

The economy should finish with its best year of growth since 3.15% in 2004. As of this writing in the third week of December gross domestic product (GDP) in the first three quarters averaged 3.3%. The Atlanta Fed GDPNow model estimates 2.7% annualized in the final three months which gives a year at 3.1%. The fourth quarter need only finish at 2.2% to insure a 3% average in 2018.

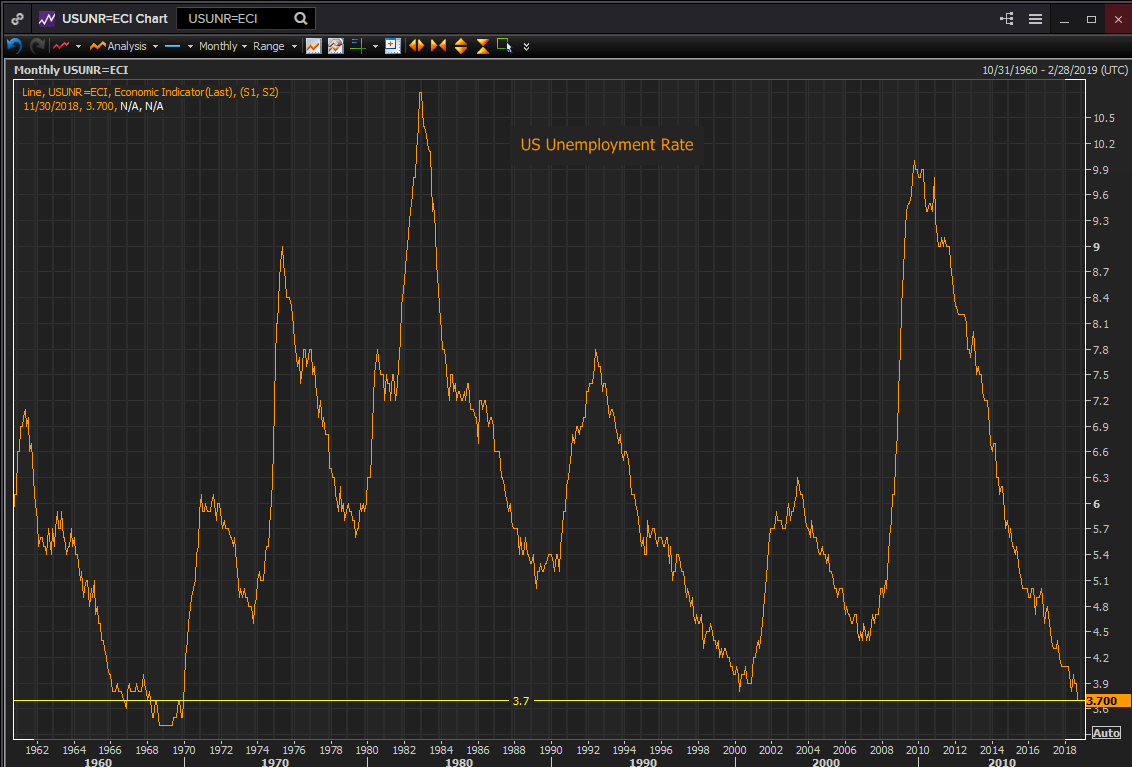

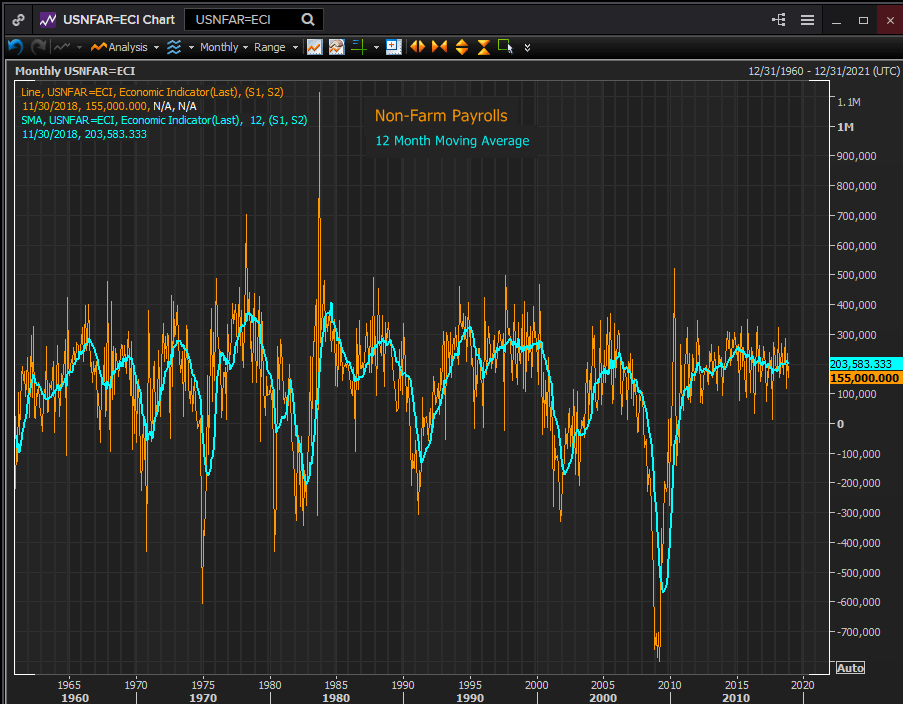

Most major US economic statistics and indicators improved or remained at high levels this year. Unemployment declined from 4.1% in December 2017 to 3.7% in November a 49 year record. Non-Farm payrolls averaged 206,000 a month through November. That is the best job creation since 2015 and well above the 75,000-100,000 needed monthly to give jobs to new market entrants.

Reuters

Average hourly earnings moved from 2.5% in December 2017 to 3.1% in October and November, which though below pre-recession ranges is the highest since the financial crash. Personal income which includes investment and transfer earning to give a wider picture of household income improved at a steady 0.35% monthly pace through October.

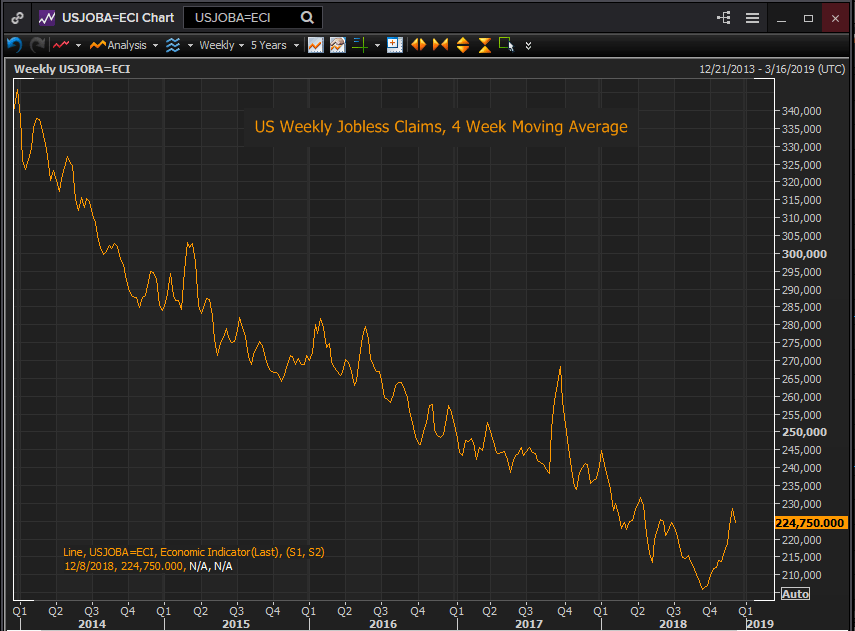

One counter indicator to the health of the labor market has been the sharp rise in the number of weekly jobless claims in the past three months. The four week moving average has gone from 206,000 on September 15th to 228,500 in the first week of December. It has since fallen to 222,000 in the week of Decmber 15th. One reason this statistic has not raised alarms is that claims are at levels not seen since the early 1970s. When claims began their rapid rise in late 2007 in the run into the financial crisis they began from a base at 320,000.

Reuters

Consumption numbers were buoyant. Retail sales saw the strongest annual growth in five years as did the monthly control group component of gross domestic product. Durable goods orders excluding the transportation sector, in practice the civilian airplane business of Boeing Company of Chicago, were heftier in the first six months of the year but still had the best averages since the middle of 2013. Likewise the 12 month moving average for real personal consumption expenditures moved to its best level in three years in August before dropping back as the fourth quarter began.

Inflation: Gone before you know it

Inflation remained contained. The core PCE price index, the Fed’s elected measure was at 1.9% in October having touched but not broken 2% four times during the year. The 12 month moving average was at 1.83% in October the highest it has been since early 2013. Overall PCE inflation moved to 2.3% for three months in the middle of the year largely on oil prices as West Texas Intermediate traded above $74 a barrel in July and then topped at $76.41 on October 3rd. By September and October inflation was back to 2% and set to move lower. Oil prices fell steeply from that October peak down 38% to $47.41 on December 18th.

US Dollar: Luck is as good as being right

The dollar’s strength in the second half of 2018 was based on the Fed’s interest rate policy and the self-inflicted wounds of the euro and the sterling. Risk aversion played to the dollar’s safe haven status and the risks posed by Brexit and the various political and economic problems of the EU. Political considerations allied with fading economic growth make it highly unlikely that the ECB would move from its accommodative policy even after it ends bond purchases in December. The dollar will begin the New Year on the upbeat with the Fed moderating its rate policy but still tightening and the euro facing two quarters of Brexit turmoil.

Forward Indicators: When the going is good don't stop

Consumer Sentiment

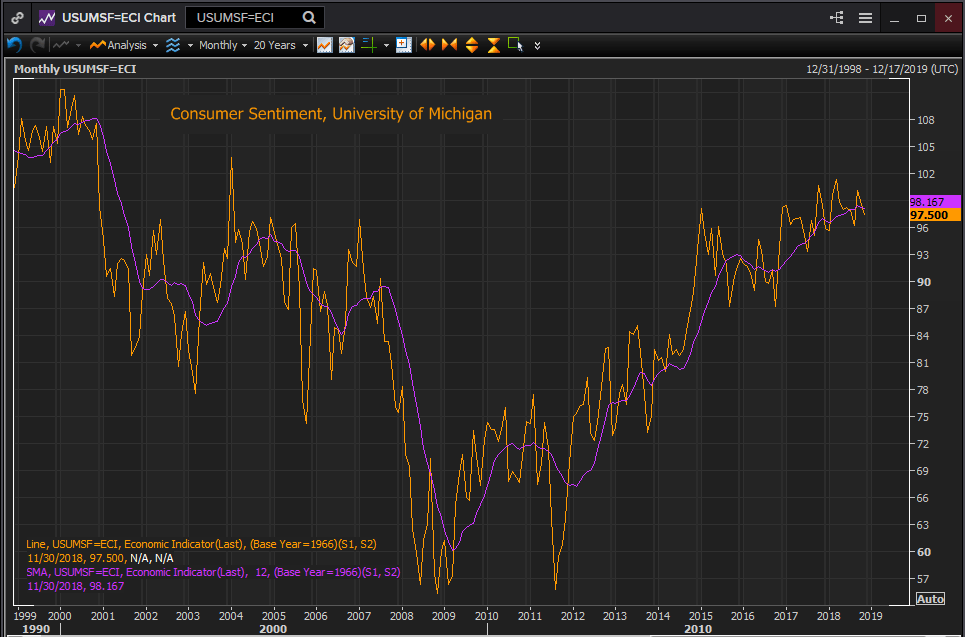

The University of Michigan overall Consumer Sentiment Index ran at its highest scores since 2001 throughout the year. The annual moving average in November of 98.17 was the best since June 2001.The measures for current conditions and six-month expectations were at 18 year and 13 year peaks respectively.

Reuters

Consumer confidence as gauged by the Conference Board, a business group, reflected the same optimism. The 12 month moving average in November of 129.78 was the highest since April 2001. Early holiday sales were up 0.9% in the control group in November, the best in a year.

Consumption will be aided by the more than one-third drop in the price of crude oil in the last quarter. The price of oil is expected to remain under pressure next year as the US becomes the world’s premier producer of energy.

Business Sentiment

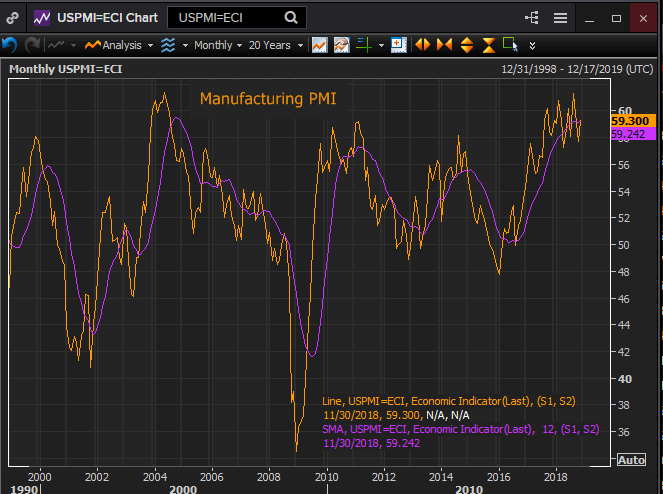

Business sentiment also was highly positive throughout the year. Purchasing managers’ indexes in the manufacturing and service sectors from the Institute for Supply Management exhibited resilient optimism all year. Manufacturing PMI was 59.3 in November with the annual moving average at its highest in 14 years. New orders saw their strongest sustained surge this year since 2005 and employment had its best 12 months following the hiring recovery in 2010 and 2011.

Reuters

Business sentiment in the much larger service sector was even more ebullient. September’s score of 61.6 in the index was the second highest in the 21 year history of the series. The 12 month moving average was the highest on record. Similar heights were reached by averages for new orders, the strongest in 13 years, and employment, also the most positive since the start of the series in July 1997.

The Small Business Optimism Index from the National Federation of Independent Business, a gauge that dates to January 1975 saw the highest result on record in August at 108.80 and the highest annual moving average in November at 106.72.

Business investment which had been active in the second and third quarters retreated somewhat in September and October. Non-defense capital goods minus aircraft, known for short as Cap-Ex, a closely watched proxy for business capital spending, dipped from its 0.7% 12 month moving average in July to 0.3% in October. This spending could recover if the inventory produced in the third quarter, which was a large part of GDP, moves to sale quickly.

Annual gains in industrial production have risen sharply since the beginning of 2016. They reached 5.5% in September, the highest since the recession recovery in 2011 and posted the best 12 month moving average at 3.8 % in November.

Housing has been the one exception to an overall strong economy. Existing home sales, about 90% of the US market, peaked in November 2017 at 5.72 million annualized units. Sales have fallen 10% to 5.15 million in September though they recovered to 5.32 million in November. Rising mortgage rates have taken their toll on home buyers. The rate of a 30-year fixed mortgage jumped more than a point from 4.16% in early December 2017 to 5.17% on November 9th. Rates have since eased to below 5%. Though 30-year fixed rates are well below historical averages the long period of extremely low cost borrowing may have conditioned purchasers to expect the exceptional in home purchase interest expenses. That expectation may take some time to disappear.

Of the three legs of the economy, consumption, business investment and government spending the first is growing at a healthy rate, the second will expand as long as the first does and the third should remain stable, as political gridlock takes over Washington.

Equities: Sometimes the herd goes over a cliff

The one major set of indicators that had a negative image of the immediate future for the US economy were the equity averages. The S&P 500, the Dow and the NASDAQ were all negative for the year by mid-December having lost all of their 2018 gains since October. Despite the losses all remained substantially higher from their early 2016 lows. The S&P for instance closed at 2,416.62 on December 21st 34% above its February 11, 2016 low.

Reuters

Equities can price as a discount for future economic activity. In the long run stocks rise because the economy expands. But in shorter time frames, especially at year end after a tremendous two year rally, profit is the prime motive.

The late fall sell-off in the US and around the world had more to do with the global economic and trade concerns than with specific US economic topics. Those worries were a catalyst for the rapid decline in the equity averages. The proximity to the end of the year and the desire of managers to preserve positive returns also played a heavy part in the volatility of the selling.

Stocks do have a feedback loop to the US economy which over time can impact economic performance. As prices fall the investor class is less wealthy and less inclined to spend. If the sell-off becomes a bear market, generally considered 20% from recent highs, then the pessimism of the market can infect the overall economy, postponing or eliminating consumption and investment. Magnified and repeated through the media this pessimism can act as a retardant on growth.

Credit Markets: The adult in the room

One of the surprises of the year has been the resiliency of the bond market. Throughout most of the year as the Fed projected the Fed Funds to 3% and beyond the benchmark 10-year Treasury was assumed to be headed back to more historical range above 3.5%. In October and early November it looked possible with the yield reaching 3.25% and above several times.

By the second week in November prices had reversed sharply driven higher by the combination of equity declines, global trade, economic growth concerns and the evident shifting of Fed policy. The yield on the generic 10-year Treasury had fallen 51 points to 2.75% by December 19th.

The credit markets are historically known to be the earliest readers of economic portents. This year the bond traders seem to have known the Fed governors’ minds even before they did themselves.

Reuters

Federal Reserve Policy: Circumspect in all things

The Federal Open Market Committee (FOMC) raised the Fed Funds rate 25 basis points to 2.5% at the December 19th meeting. It was the fourth increase of the year and the highest base rate since March 2008.

The bank reduced by one the number of projected increases next year. The new 2.9% Fed Funds estimate for December 2019 needs only two to get there from 2.5%. It also reduced the terminal rate in 2020 and 2021 to 3.1% from 3.4%, keeping one incease in 2020. The bank also dropped its 2018 GDP projection to 3% from 3.1% and its 2019 forecast to 2.3% from 2.5% while keeping 2020 at 2% and 2021 at 1.8%.

The US central bank began this rate cycle in December 2015 having kept the Fed Funds upper target rate at 0.25% for seven years in the aftermath of the financial crisis. The governors hiked just once in 2016, delayed by the sharp equity fall in the first two months of the year and worried about the strength of the recovery, three times in 2017 and four this year.

The US economy is performing well and with inflation just below the Fed's 2% target there has been considerable public discussion about the terminus or neutral rate for Fed policy. This is the level at which interest rates neither encourage nor inhibit economic activity. The rate is presumed to be between 2.5% and 3.25%, the upper end of the current rate projections. Fed Chairman Powell said as much when he stated that the Fed Funds (then 2.25%) were just below the neutral level. Mr. Powell also stated that the bank has become more 'data dependent' as it approaches the end of its tightening cycle.

Data Dependency

'Data dependent' means taking your cues from the economy. But it also means adressing threats to the economy as they appear. December's FOMC did both. The healthy US economy let the Fed add one more 0.25% increase to its normalization total. The "Projection Materials" temporized on the future, reducing September's three 2019 inceases to two while leaving one in 2020 and none in 2021.

Although the US economy seems to be bearing higher rates well the Fed is clearly taking out an insurance policy on the future and the global economy.

If the US begins to slow next year will it be due to the cumulative effect of higher US interest rates or from the gathering drag from the global decline in economic growth? Will the trade dispute with China or a Brexit recession in Europe bring US GDP to the Fed's projected 2.3% in 2019?

A further consideration for the bank governors is the sharp equity sell off in the past ten weeks. The major US average are all now down for the year though even with the recent decline US equities remain more than 20% higher since the 2016 election.

The Fed’s newly asserted data dependency is reinforced by the additional press conferences in 2019. Instead of the usual four after the FOMC meeting scheduled with ecoonomic projections, Chairman Powell will make a statement and take questions after all eight meetings.

The Fed clearly feels that rates are approaching an inflection point, the neutral rate and intends to keep its public stance more current. As that point nears it paradoxically makes the Fed ‘dot plot’ of rate projections less important. The Chairman’s comments will overtake any intention gleaned from the older information.

One interesting note on the Fed Funds rate is that in its relation to inflation it is essentially zero. The Fed Funds rate is 2.5% and CPI in November was 2.2%.

Projection Materials

At the September release the estimates for US economic growth were 3.1% in 2018, 2.5% in 2019, 2.0% in 2020, and 1.8% in 2021 and in the ‘longer run’, as the bank phrases it. As of the December FOMC the estimates are 3.0% in 2018, 2.3% in 2019, 2.0% in 2020 and 1.8% in 2021. The 'longer run gets 1.9%.

Annualized GDP is currently running at 3.125%, taking the Atlanta Fed’s 2.7% current estimate for the fourth quarter.

The key to the projections is their change over time. Until the December materials the estimates for US growth had been rising. The September GDP figures were higher than the June numbers which were 2.8% for 2018 and 2.4% in 2019. The later years were unchanged,

Although the economic prospects improved from June to September the rate projections did not change that month except in the imprecise ‘longer run’ category beyond 2021.

In the September materials the Fed Funds rate was projected at 2.4% at the end of this year which was achieved with the hike on Wednesday. They were projected at 3.1% in December 2019, 3.4% in 2020 and 2021. The December materials now posit 2.9% at the end of 2019, and 3.1% in 2020 and 2021. This implies two 0.25% hikes next year and one in the two years after.

US Economic Performance and Risks in 2019:

Don't kill the golden goose

The American economy has shown no evident signs of a lapse this year. On the consumption side the job market is steadily creating more jobs than can be filled. Slowly gathering wage increases coupled with low inflation have given the consumer a rare period of modestly increasing purchasing power. This should continue into next year as the labor market shows no sign of retreat.

The consumer is the heart and soul of the American economy. As long as spending continues to be strong most other effects on the economy are secondary. Readings from the University of Michigan and the Conference Board indicate that sentiment remains buoyant. Low inflation and stable, particularly with the soon to retreat gasoline prices, will add to the sense of economic well-being.

Judging from the relative decline in GDP from the second quarter's 4.2% to the fourth's 2.7% (estimated) and the fact that no further tax reform or stimulus will be forthcoming from a Democratic House and until the China trade dispute is settled, GDP will likely slip into the 2.5% to 3.0% range. After the trade issue is disposed of GDP could return to 3.0% to 3.5%.

Once the old year is gone and with it the equity markets' obsession with annual performance metrics, attention will turn to the still vibrant state of the US economy. As with GDP, when the China trade issue is removed as a source of worry, equities should regain much of the year end losses.

The anticipated Fed relaxation in its pace of rate increases, with two now likely next year, should help the housing market to revive. Housing sales are suffering an emotional hangover from having been the beneficiary of historically low rates for the past five years. The current rate on the 30-year mortgage is low by past standards though the rise in home prices has made purchases expensive for many people.

Business spending responds to demands from the consumer sector. The second and third quarters had some of the strongest investment since the recession. Here also the consumer will set the pace. Sentiment indexes remain strong. Purchasing managers’ indexes in manufacturing and services are close to their record highs as is the small business sentiment index.

2019 Risks: Only fear itself

Domestic Risks

There are several accumulating risks for the US economy. Domestic risks are primarily political and psychological in nature. Global risks are based in politics and trade but their economic effects are more immediate and evident.

In the US the risk is that the soon to escalate fight between the Democratic House and the Trump administration will so paralyze the government that its essential functions are affected and these carry over into the real economy.

Americans are largely inured to the machinations of the inhabitants of what is called the DC Beltway, for the highway that runs in a circle around the capital. But ignore the government as Americans might prefer, a prolonged government shutdown will have an effect, even if, as is true, only about one-quarter of the Federal government's operations actually cease temporarily. The psychological effect of unrestrained political warfare in Washington has an insidious but hard to quantify effect on the nation's economic optimism.

Global Risks

The trade dispute with China and the potential slowdown in the world’s second largest economy are the biggest economic risks for the US in the New Year. A large percentage of American consumer products are made in China, either by domestic Chinese producers or US manufacturers based on the mainland. American farmers sell vast amounts of their production to the Chinese. The trade is more important to the Chinese economy than to the US and the recent slowing in China’s GDP can be largely blamed on the argument with the US. But the impact of a weaker China is a risk for the global economy.

The terms of trade between the US and China were founded in an earlier economic world, when China was truly a developing economy. That is no longer the case. China understandably is reluctant to surrender some of her advantages, and the fact that no US administration in 30 years has tried makes this attempt more difficult.

The importance of the relationship to both sides is such that it is almost certain that a deal will eventually come forth. The dependence of China on US markets provides an incentive for a solution and the recent tariff truce provides a method.

Europe’s problems are more intractable. Slow growth and unemployment is endemic in much though not all of the EU. It is the disparities in economic success since the advent of the euro and the Maastricht Treaty and the disagreements over immigration between the governing elites and large sections of the populace that are creating the political tensions within the EU.

The British departure, provided that it occurs, will have a negative impact on EU and UK economic growth. If the exit is without a negotiated agreement it will likely precipitate a recession on both sides of the Channel.

Italy’s dispute with the EU Commission has been mollified. Rome will be allowed to spend more than the last government promised and the Commission will point to the reduction of the deficit as its achievement but Italy’s basic problem with the euro and a stagnant economy will not change.

The Organization for Economic Cooperation and Development (OECD) has reduced its projection for 2019 global growth to 3.5% from 3.7% indicating concern in this generally optimistic assessment.

Conclusion

Return to a bipolar world

The US economy should continue its strong performance in the first half of 2019. The domestic economy is robust enough, particularly the labor and consumer sectors to roll through June on momentum alone. In the second half of the year the impact of the global economic environment could begin to tell. The US economy can probably weather a serious slowdown in China or an EU recession alone without losing much in GDP expansion, but together they would seriously impact growth.

The Fed reduction in its 2019 rate increases from three to two in the December projections aknowledges the uncertainty created by Brexit, China and declining global economic growth. With these risks to the global economy unsettled, caution came to FOMC along with dependency. When the threats to growth from Brexit and Europe subside and trade with China is mediated the second half of the year could see a pickup in gobal and US growth and a resumption of Fed tightening.

The dollar will retain moderate strength in the first half of the year despite the Fed's tactical retreat on rates. Safe haven flows and negative pressure on the sterling and euro with episodes of volatility will continue to aid the US currency as long as the manner of the British exit from the EU is undecided. In the second half the dollar will fade as the worst fears for Brexit do not come to pass leading to a recovery in the euro and sterling. A US-China trade deal will revive risk markets and drain dollar strength.

The trade dispute between the US and China is the key to global economic performance in 2019. Together, the US and China can power global growth even if the EU and Britain fall into recession. If that relationship can be restored to pre-dispute activity and eliminated as a drag on real growth and a psychological drag on markets then the all may be relatively well.

RELATED FORECAST 2019

EUR/USD: At the starting line of a long and bumpy road

GBP/USD: Imprisoned by Brexit darkness Sterling is set to chart a check mark

USD/JPY: A barometer of global growth and markets

AUD/USD: Collateral damage from the US-China trade war

USD/CAD: CAD comeback on the cards

USD/MXN: Volatility set to remain elevated

Gold: Focus on US real interest rates

Oil: Dwindling demand and substantial supply likely to pressure petrol

The European Union Economy and Politics: Conflict at home

China and International Trade: The crossroads of a great power

Dollar Index: A stumble is not a fall

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.