USD/CAD Weekly Forecast: Lumberjacks and pumpjacks

- Commodity prices at 6-year high drive USD/CAD down.

- USD/CAD closes at lowest level since September 2017.

- April Canadian jobs losses prove no impediment to loonie gains.

- FXStreet Forecast Poll sees a modest rebound brewing.

Commodity prices vaulted to their highest level since July 2015, taking the USD/CAD south despite dismal Canadian and US April employment reports.

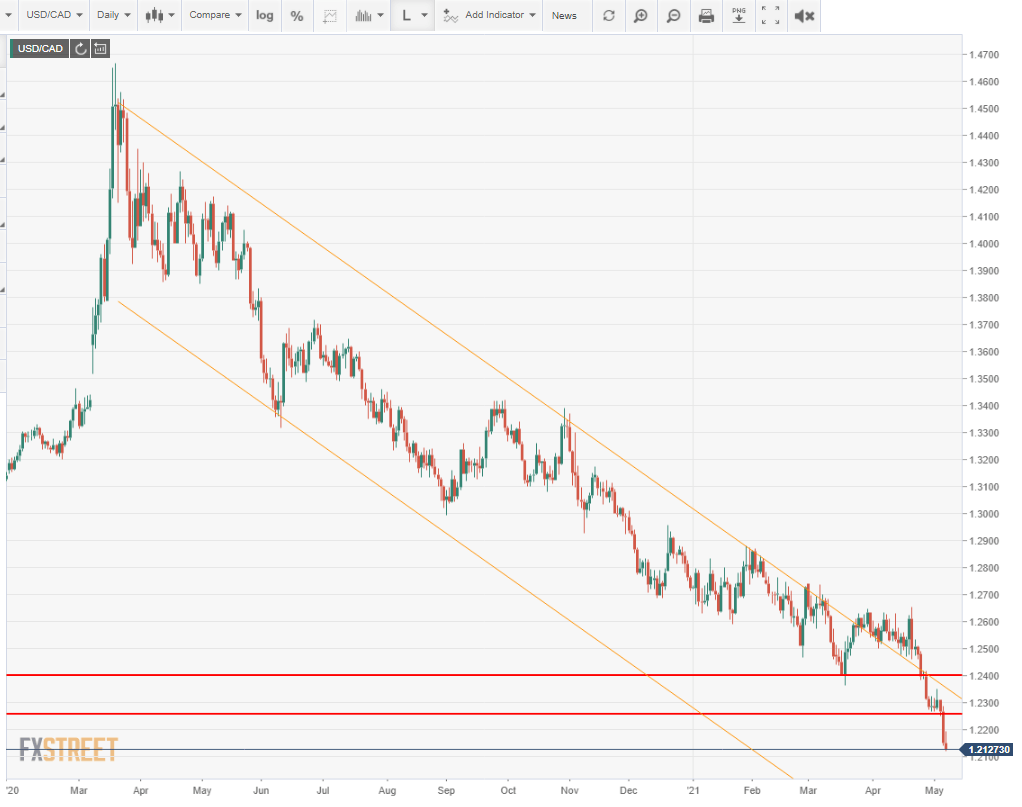

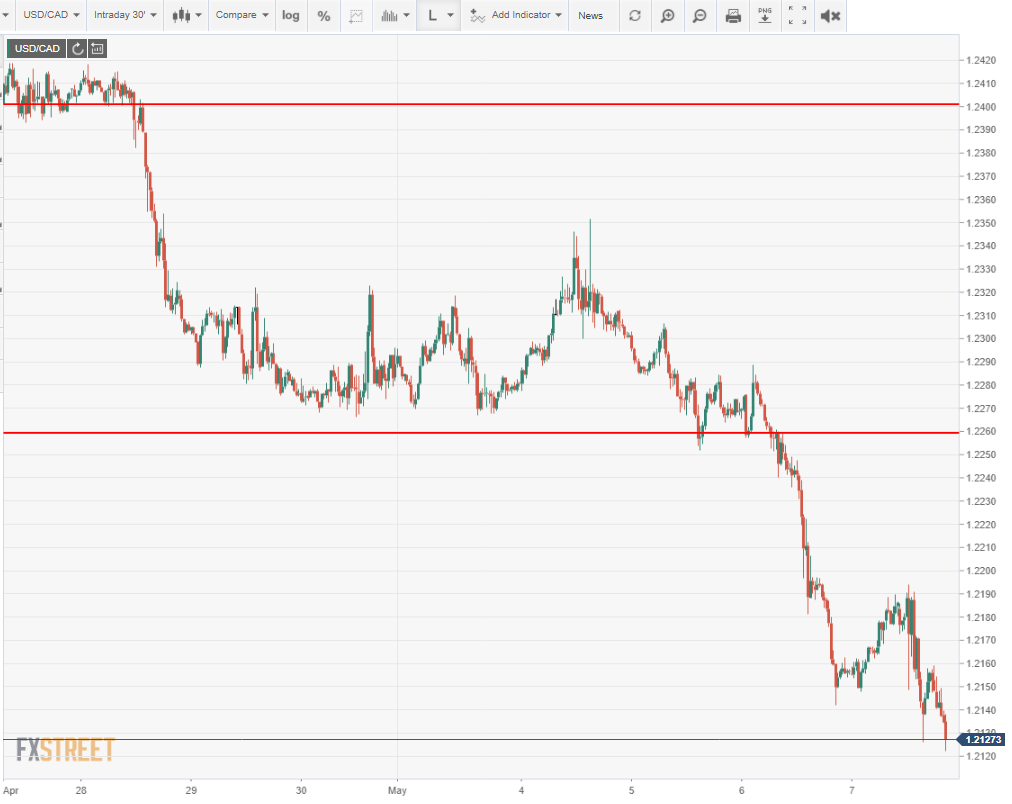

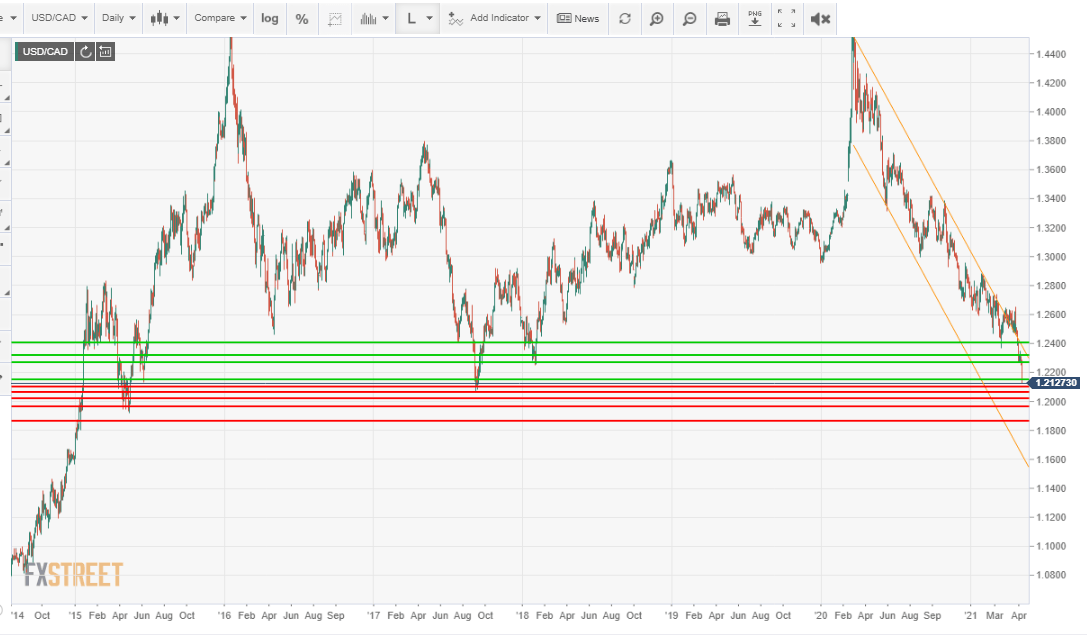

The USD/CAD closed the week at 1.2127, its lowest finish since September 2017. In the last two weeks, the US dollar has lost 2.8% against its Canadian rival, accelerating down as major support at 1.2400 broke on April 28 and then when 1.2240-60 gave way on May 6.

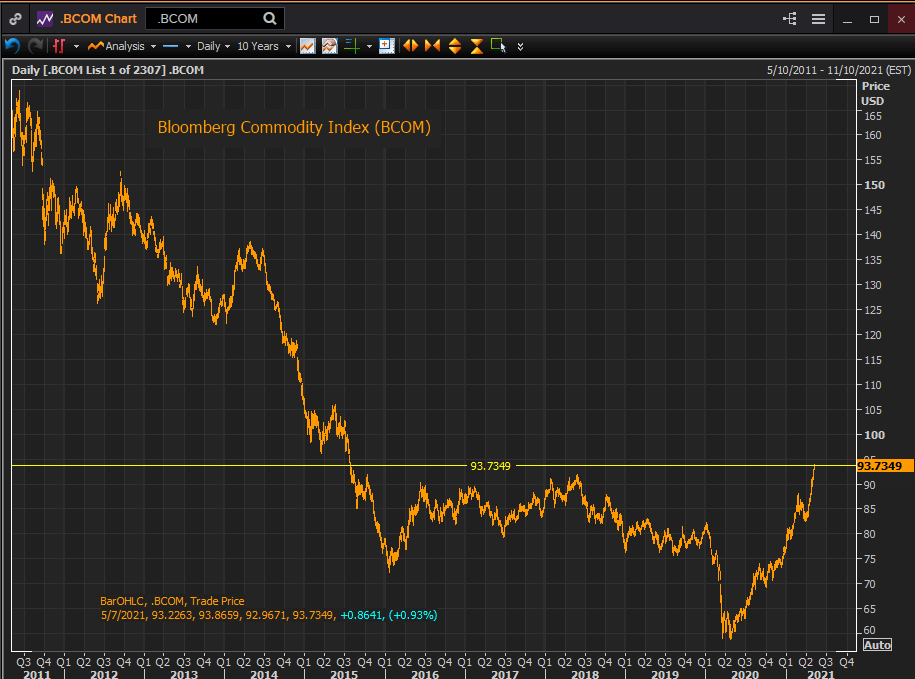

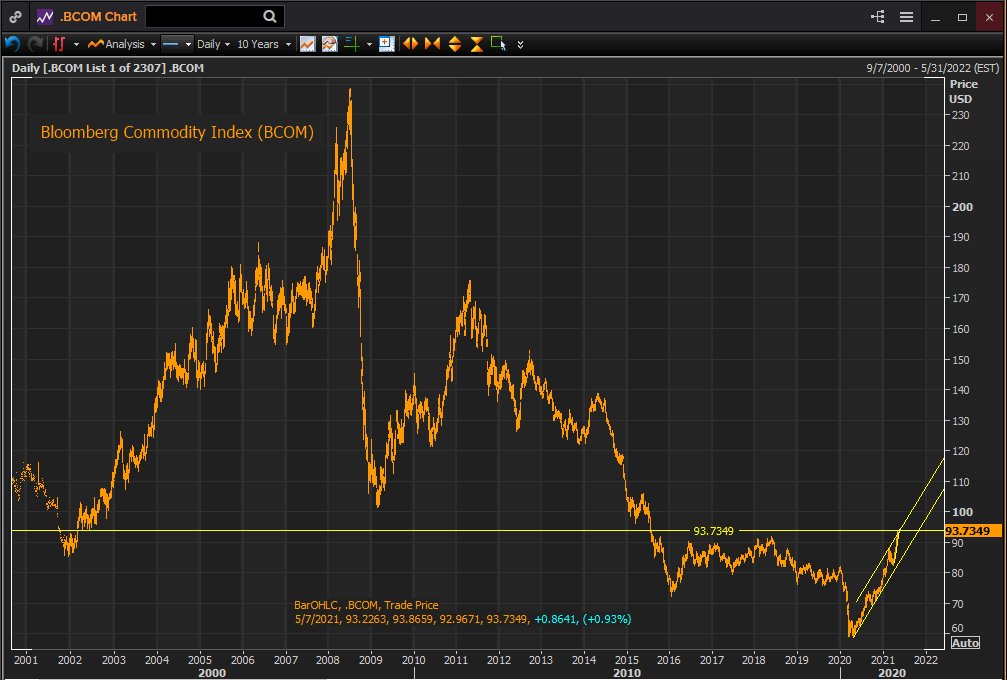

Prices for commodities have risen sharply in the past three weeks, capping a year-long climb, as the US economy shows every sign of a rapid growth spurt.

The Bloomberg Commodity Index (BCOM) has jumped 10.96% since opening at 84.47 on April 14 and added 3.14% this week alone.

Reuters

Friday’s BCOM finish at 93.73 was the highest for the index since July 23, 2015 and is an astonishing 57.6% above its pandemic and all-time low close of 59.47 on March 18, 2020.

Reuters

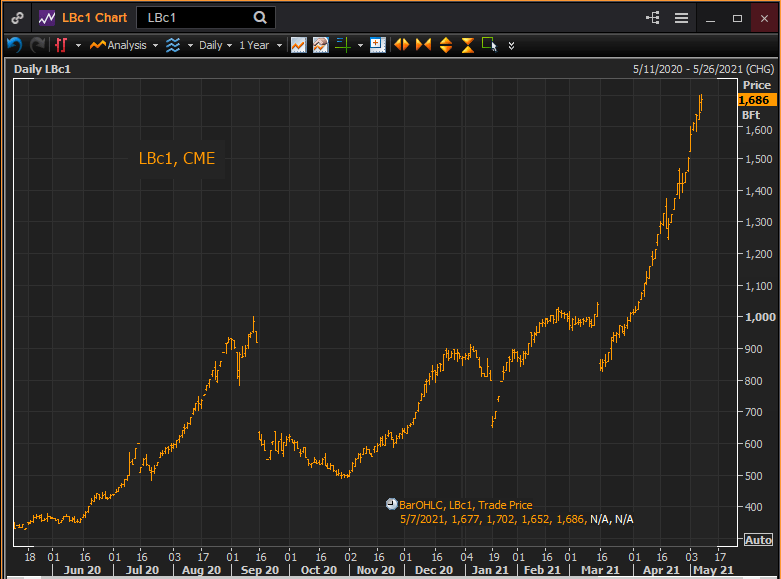

Emblematic of the surge in commodity prices is the doubling of the Chicago Mercantile Exchange’s (CME) Lumber Futures (LBc1) in seven weeks as the spring construction and remodeling season begins in the United States.

Reuters

Canada’s adjunct position to the US economy provides dual benefits. First, as strong US growth sources extra orders to Canadian manufacturers, and second, as the origin of many raw and processed material supplies to the far larger American economy.

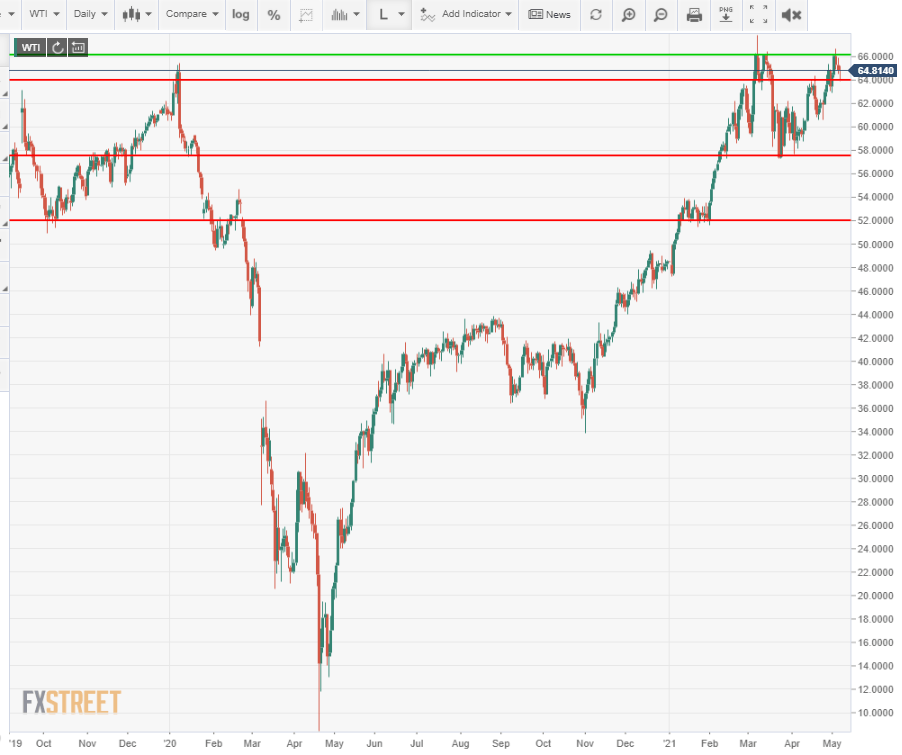

West Texas Intermediate (WTI), the North American crude pricing standard, rose $1.36 on the week to close at $64.81, holding above the important $64 support mark.

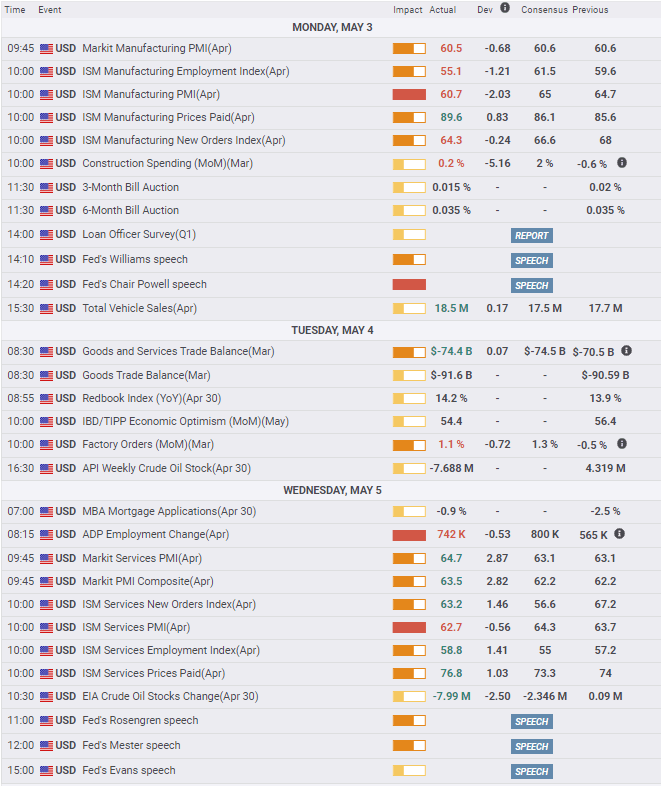

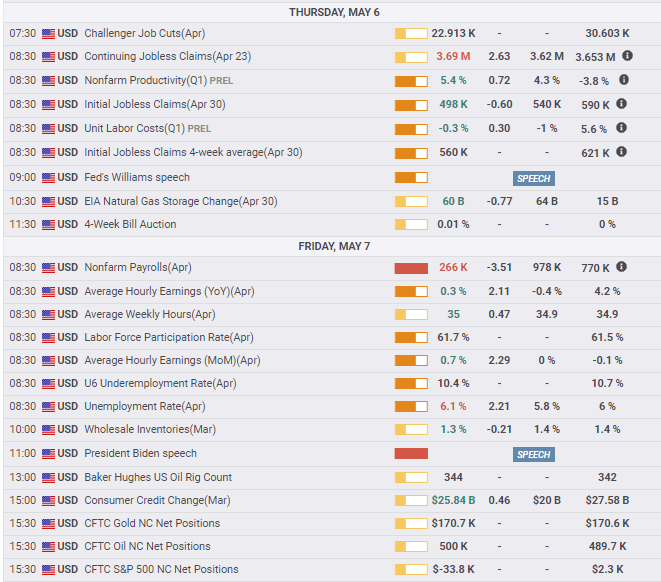

American Initial Jobless Claims on Thursday dropped below 500,000 for the first time in 14 months and the 498,000 figure seemed to promise that the last recalcitrant US statistic was headed for improvement. The USD/CAD promptly fell from 1.2240 having edged through 1.2260 support earlier in Europe, with an extension of the economic growth logic that has been pushing the USD/CAD lower this year.

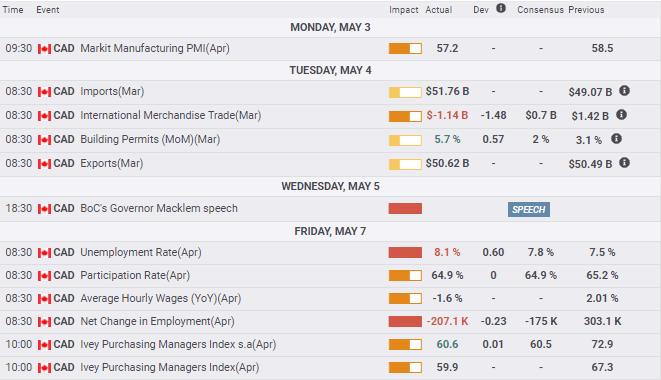

The Canadian April Employment Change report was even worse than the US one with an outright loss of 207,100 positions. It was, however, largely expected with the consensus estimate of -175,000. Canada’s far less widespread vaccination program and restrictions in several provinces enabled the negative expectation. The Ivey Purchasing Managers’ Index (PMI) for April fell 12.3 points to 60.6, but, like the payroll figure, was wholly expected.

American firms hired just 266,000 people in April and the unemployment rate rose to 6.1%, according to the US Department of Labor.

A far better report had been expected with a 978,000 consensus estimate for payrolls and a 5.8% unemployment rate.

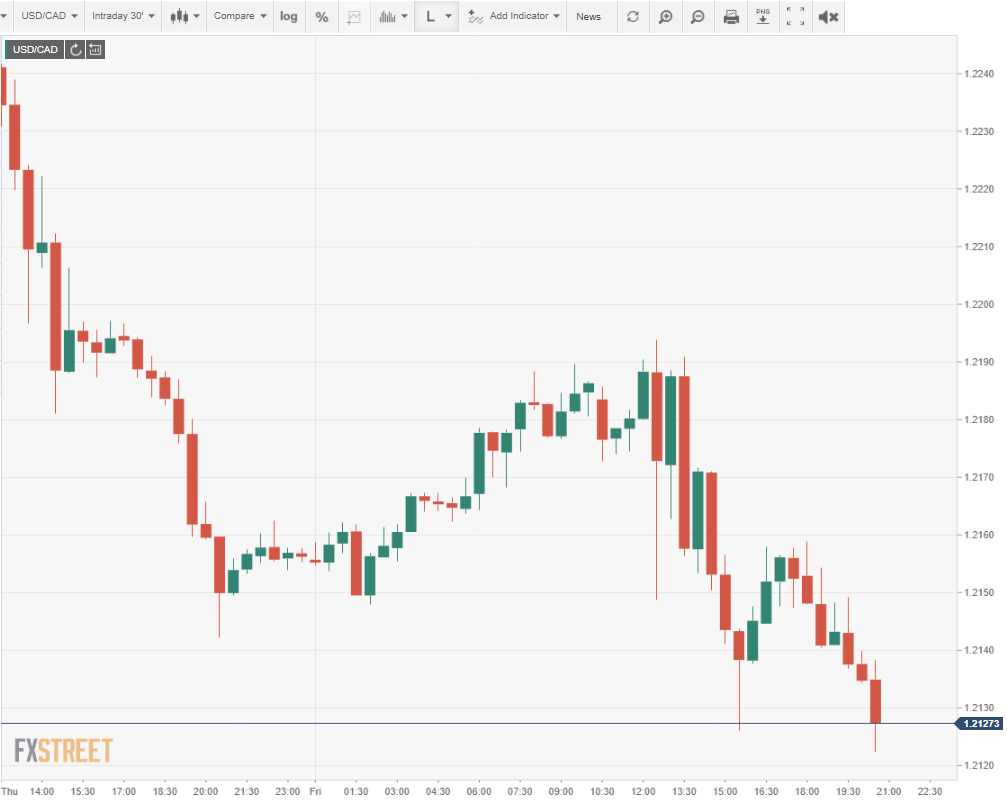

The USD/CAD fell at the Nonfarm Payrolls (NFP) release, dropping about 150 points in two hours, recovering slightly then moving steadily lower into the close.

Treasury yields at first mirrored the sell-off in the dollar. The 10-year yield fell from 1.56% to 1.47% but by the close had added two basis points to 1.579%.

Equities rose on Friday with the Dow adding 0.66%, 229.23 to 34,777.76, the S&P 500 0.74%, 30.98 points to 4,232.60 and the Nasdaq rising 119.39 points, 0.88% to 13,752.24. Despite an initial disturbed reaction from the Dow futures, the weak payroll report makes Federal Reserve intervention and lower rates a continuing certainty.

The NFP figures fit the Federal Reserve’s caution perfectly. As Chairman Jerome Powell said after the FOMC meeting two weeks ago, “We have had one good jobs report, that is not enough.”

NFP puzzle

The puzzle of US April job numbers may take several months to work out.

US economic growth was 6.4% in the first quarter. The Atlanta Fed GDPNow estimate for the second quarter is running at 11%.

Many industries report shortages of workers, particularly in skilled manufacturing roles and in the restaurant and hospitality business.

How can there be 8 million or more unemployed and shortages of machinists, waiters and waitresses? Were payrolls weak because employers could not find workers to hire?

The unexpected rise in Continuing Jobless Claims in the latest week may offer a clue. Unemployment benefits have been extended and supplemented several times in the pandemic, the last adding $300 a week for many workers.

For many lower-wage workers unemployment benefits pay as much or more than their wages. Individuals, quite logically, may prefer to collect payments as long as they can before returning to jobs that offer no economic advantage.

It is also possible that the surprising April NFP numbers could be a statistical oddity, generated by Bureau of Labor Statistics (BLS) seasonal adjustments.

The unadjusted figure shows 1.089 million jobs gained in April.

Seasonal statistical adjustments are based on historical models. If an adjustment to seasonal norms produced the swing, it could return in May, or over several months, or not at all. It depends on the assumptions in the BLS statistical model that produced the reduction.

In defense of the statisticians and their models, there was nothing normal about the past year.

Good-to-excellent US data earlier in the week from the Institute for Supply Management (ISM) and Automatic Data Processing (ADP) turned out to be a poor guide for April’s Employment Situation Report.

Purchasing Managers Indexes in manufacturing and services declined slightly in April from March’s pandemic high.

The dip in manufacturing sentiment was related to frustrations in supply and hiring, not to a diminution of business. New Orders in both sectors remain exceptionally strong and what is more important have been so for six months and longer.

The Services Employment Index rose to its best score since September 2018 and the manufacturing measure, though lower, remained firmly in expansion.

There is no indication in other statistics that the US recovery is faltering, only that employers are having great difficulty finding help.

USD/CAD outlook

The exceptionally rapid fall of the USD/CAD over the past two weeks makes a profit-taking rebound a logical event but one beset with two practical problems.

Fundamental factors have not changed. Treasury yields in the US are stalled. If the NFP weakness did not force rates lower, it is hard to see any economic information inspiring traders to take them much higher, at least until the payroll conundrum is answered next month.

From a technical point of view, there is no approaching support that is a logical point of departure for a rebound.

Beneath the Friday finish at 1.2127 are two closes from September 2017, 1.2115 on the seventh and 1.2111 on the eleventh and two low trades, 1.2062 on the eighth and 1.2083 on the twelfth. None of these brief visits are sufficient to form a base for a technical rebound.

Beyond that, the prior trip to these levels was almost two years earlier in May 2015.

The combination of commodity pricing, US economic ambivalence after the payroll report, and technical weakness should keep the USD/CAD moving lower.

Canada statistics May 3–May 7

The very weak but expected Employment Change report did the loonie no damage.

US statistics May 3–May 7

Canada statistics May 10–May 14

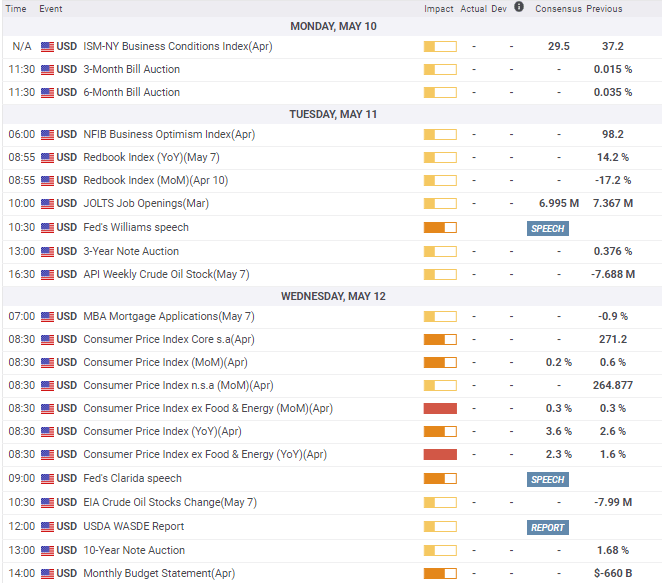

Bank of Canada Governor Tiff Macklem's speech on Thursday will be of the most interest this week. The sales figures from March are out of date.

US statistics May 10–May 14

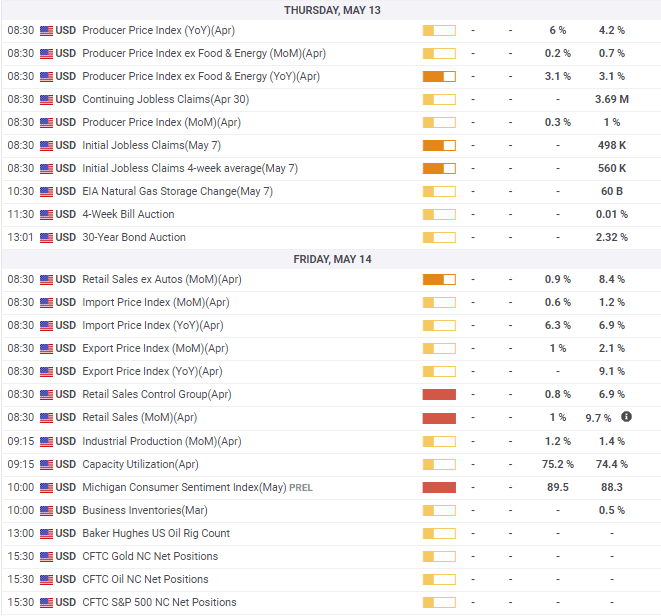

Wednesday's CPI and Thursday's PPI will report on April inflation, with NFP out of the way, attention will be on prices. Retail Sales for April are expected to return to earth, any unexpected strength will take the sting from the NFP report and support the dollar.

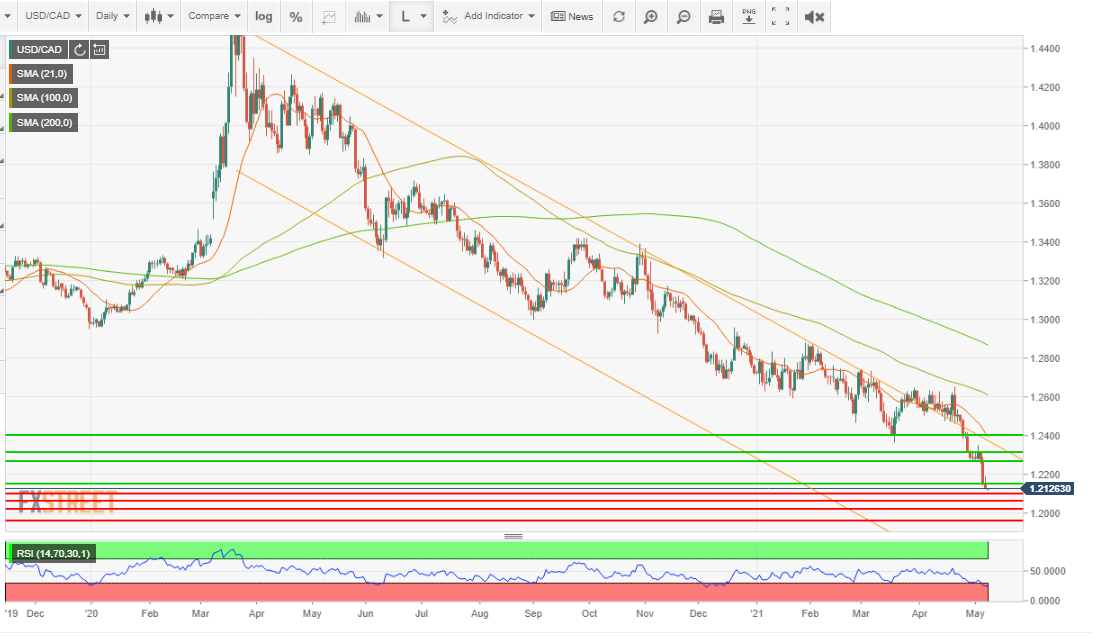

USD/CAD technical outlook

The technical situation for the USD/CAD is defined by weak and old support opposing strident lower momentum fueled by fundamental commodity and economic recovery trends.

The first support lines at 1.2100 and 1.2060 reference a brief period in mid-September 2017 and are consequently insubstantial. The next series beginning at 1.2020 are two-years earlier from May 2015, but they represent a more extensive set of trading ranges over about five weeks.

The Relative Strength Index (RSI) is oversold at 24.54 but unlikely to prompt a bounce on its own. The 21-day moving average (MA) at 1.2412 is part of resistance at 1.2400. The 100-day MA at 1.2617 and the 200-day MA at 1.2874 are unimportant at the current level.

The bias in the USD/CAD is lower awaiting a catalyst for profit taking.

Resistance: 1.2150, 1.2265, 1.2315, 1.2400

Support: 1.2100, 1.2060, 1.2020, 1.1960, 1.1860

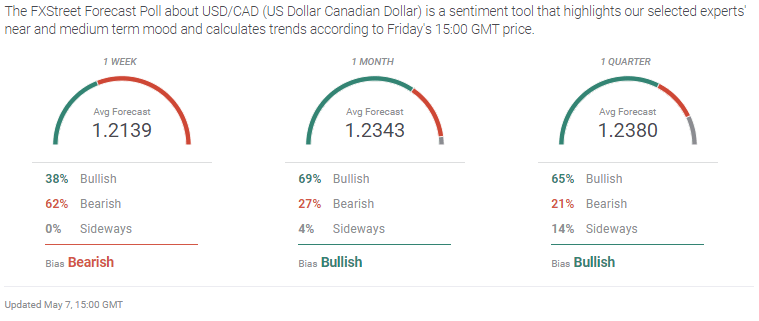

USDCAD Forecast Poll

The FXStreet Forecast Poll takes the logical view that, over the next quarter, the market will recoup some of the large amount of profits available in the USD/CAD's year-long fall.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.