US Retail Sales October Preview: Inflation is the key, not consumption

- Retail Sales forecast to rise 0.7% in October, as in September.

- Inflation has undermined Consumer Sentiment but not sales.

- Fed does not want to choose between growth and inflation.

- Dollar and Treasury rates will rise regardless of sales result.

Will surging inflation send the American consumer into hiding and end the US recovery?

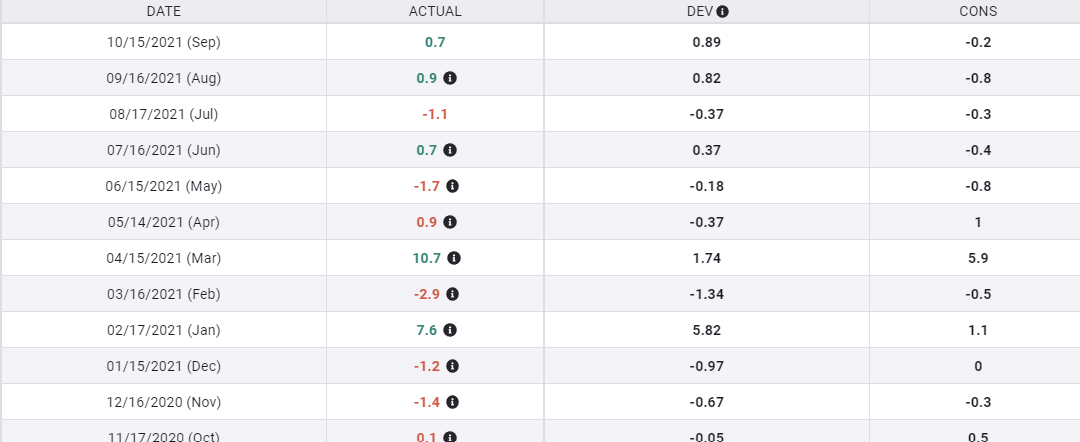

Retail prices rose at a 6.2% annual rate in October. The Consumer Price Index (CPI) has averaged 5.5% for the six months since April, the worst bout of inflation in 30 years.

CPI

For four of those months, August to November, American Consumer Sentiment has been the lowest in a decade.

Retail Sales figures for the two months thus reported, August and September, show that consumers have blithely ignored their own discontents and continued shopping.

October’s Retail Sales on Tuesday, will be the third since consumer attitudes crashed in August. Analysts expect that households will continue their spending ways.

However, because the consequences of a consumer pullback could be catastrophic for the US economy, markets are more than a little nervous that consumers might change their minds.

Retail Sales are forecast to rise 0.7% in October, as in September. Sales ex autos are expected to gain 0.7% after the 0.8% increase prior and the Control Group, which mimics the consumption component of Gross Domestic Product (GDP), is predicted to climb 0.4%, half its September increase.

Retail Sales

FXStreet

Consumer Sentiment, the labor market wages and inflation

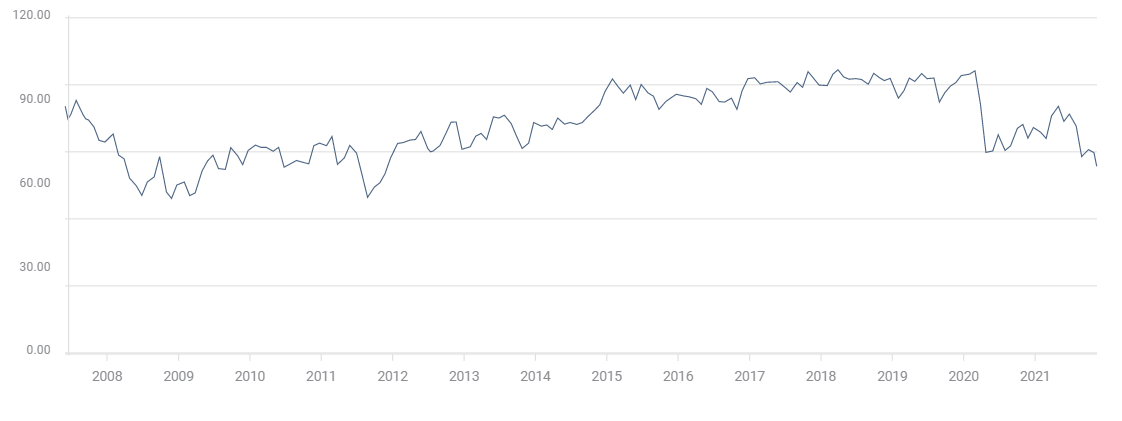

The Michigan Consumer Sentiment Index fell out of bed in August, plunging to 70.3 from 81.2 in July. The drop was wholly unexpected, the consensus forecast had been 80.8. It was the poorest US consumer prognosis since December 2011 and was below the nadir of the pandemic of 71.8 in April 2020.

Michigan Consumer Sentiment

What had happened?

Employment is normally the most important factor in consumer attitudes.

Nonfarm Payrolls have averaged 646,000 for the past six months, the best since the initial lockdown recovery in the spring of 2020. The number of available positions each month in the Job Openings and Labor Turnover Survey (JOLTS) has been nearly one million since March.

A record 4.4 million workers left their jobs in September. These voluntary resignations reflect workers' confidence in finding more lucrative or enjoyable employment.

These statistics suggest that labor shortages have moved the negotiation balance decidedly in the workers’ favor. It seems unlikely that the labor market is the source of consumer discontent.

Inflation is a different story. In the eight months from March, CPI has more than doubled from 2.6% to 6.2%. The annualized rate for the six months from May is 7.2%. In two of those months, June and October the monthly increase was 0.9%, for a 10.8% annualized rate. The reality is even harsher for most families because the inflation rate for many necessities, particularly cars, gasoline, fuel and some foods, has risen even faster than the general inflation rate.

Wages have not kept pace with inflation.

Average hourly earnings rose 4.9% for the year to October. Headline inflation was 6.2%. A household’s purchasing power shrank by the difference of 1.3%. Wage increases have not outpaced inflation since March. To use the reverse measure, consumers lost ground to inflation for seven straight months.

Americans know that plentiful jobs cannot correct for inflation that is moving faster than even the most generous or desperate employer. Inflation, not unemployment, is the cause of consumer unhappiness.

Retail Sales

Retail Sales have been essentially flat over the six months from April, averaging 0.07%. The August and September results at 0.9% and 0.7% were the strongest of the run.

Sales ex-autos were also healthy, averaging 0.5% for the half year and a strong 1.4% in August and September. The Control Group was weaker on the six-month average at 0.3% but at 1.7% for August and September, the most robust of the lot.

Whatever the variation in sales over six months, the collapse of consumer attitudes that began in August had no impact on Retail Sales that month or in September.

Federal Reserve and the consumer

The worst scenario for the Federal Reserve monetary policy is a weakening US economy combined with inflation.

It is already too late for rate policy to have any effect on the next six months of price increases. Prices will be determined by labor and product shortages and the amount of liquidity pumped into the economy by government spending. The reduction or not of the Fed’s bond purchase program does not and cannot address the origin of the current inflation which lies in the economic dislocations of the lockdowns.

The question for the Fed governors is how can they best keep the confidence of Americans? How can the central bank prevent the essential consumer from becoming discouraged?

If the US consumer continues to spend then the US economy stands a very fair chance of weathering the problems of the next year. If however, consumption begins to falter as households attempt to conserve purchasing power, economic growth could quickly reverse. At a 2% GDP rate in the third quarter, it would not take much of a consumer retreat to begin a recession.

Rampant inflation is the threat to family budgets and to the perception of a return to a stable price environment.

The best that the Fed can do is to convince the markets and the consumer that it is determined to deter inflation. This requires that the taper continues, or even advance its schedule and that Treasury and commercial rates be allowed to rise.

Market reaction

Whatever the Retail Sales number for October, the Fed’s taper program will remain on track. Treasury yields and the US dollar will move higher.

If sales are better or equal to the 0.7% forecast, it will allay concerns that the US consumer is pulling back. With healthy consumption the economy will continue to expand and the Fed’s taper program will progress to completion. Treasury and market rates will adjust to the expectation of a higher fed funds profile next year.

The unusual case is if October’s Retail Sales are less than forecast.

Normally a weak sales report, especially in tandem with very low consumer sentiment would prompt a reconsideration or pause in the Fed taper program.

This time it will not and the reason is inflation. If consumers pull back on spending it will not be because the economy is slowing or because jobs are hard to find, but because inflation is eroding purchasing power.

The Fed cannot tame current inflation. The Fed, can and must, reassure consumers and markets that controlling future price increases are its top priority. If it does not inflation expectations will swiftly build in future gains.

The best way for the FOMC to keep future inflation in check and keep the consumers' confidence is to continue the taper and let Treasury rates rise.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.