US Michigan Consumer Sentiment Preview: Concerns about the future are driving the decline in sentiment

- Consensus estimate predicts a small drop in October consumer sentiment.

- Consumer confidence has not recovered from its late summer plunge.

- Labor market and wages remain strong but their influence on sentiment may be waning.

The University of Michigan will issue its preliminary Survey of Consumers for October on Friday October 11th at 14:00 GMT, 10:00 EDT.

The survey consists of three indexes--the Index of Consumer Sentiment, the Index of Current Economic Conditions and the Index of Consumer Expectations. Each result is revised once. The survey began in 1978.

Forecast

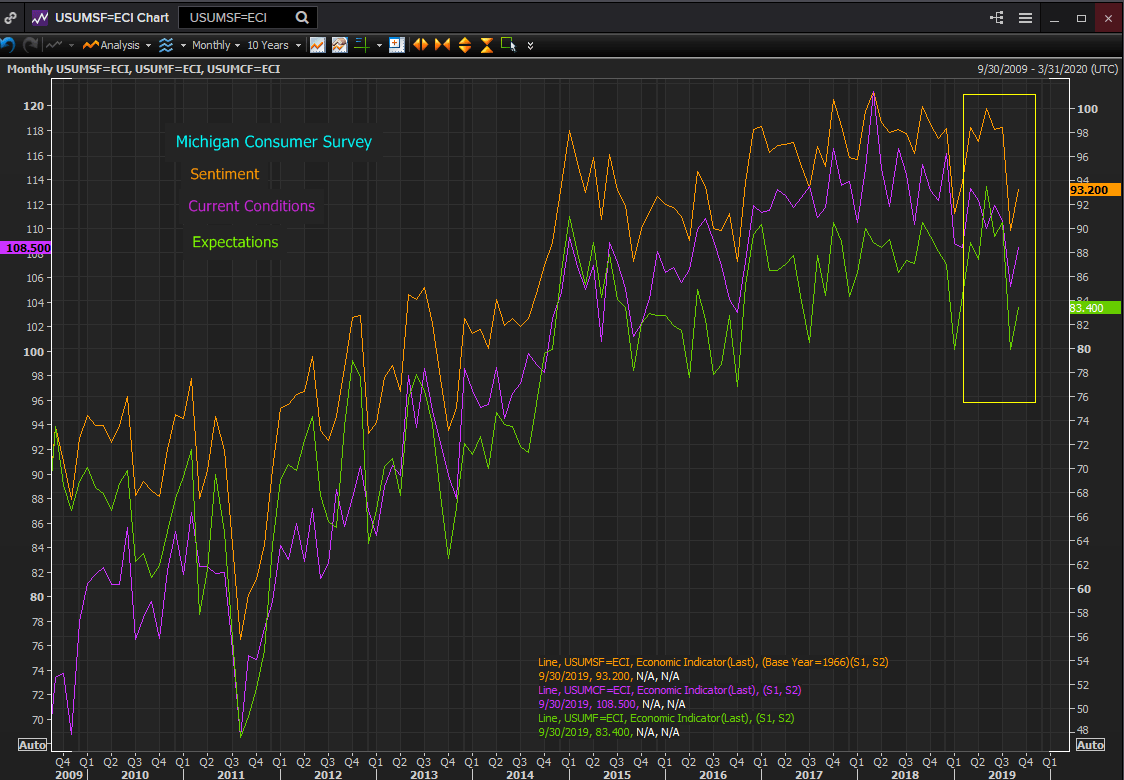

The Consumer Sentiment Index is expected to drop to 92.0 in October from 93.2 in September. The Current Conditions Index is projected to slip to 107.5 in October from 108.5 the prior month. The Expectations Index is forecast to edge lower to 81.7 from 83.4.

Michigan and the Conference Board consumer surveys

The late summer decline in the major US consumer confidence measures occurred despite one of the strongest job and wage markets in decades, traditionally among the most important factors in consumer satisfaction.

The 8.6 point drop in the Michigan Sentiment index from July to August was the biggest in six years.

The following month the Conference Board confidence score dipped to 125.1 from 134.2.

Reuters

Both indexes have returned to the lower limits of their ranges for the last two years. The Michigan index is back to the level of November 2016 before the prolonged rise that began with the presidential election.

Michigan current condition and expectations indexes

The Michigan survey questions consumers about their sentiments in two time frames. Respondents are asked about their satisfaction with their current economic condition and about their expectations for where they will be in six months. The split between the two sets of responses is instructive.

This year the index of current satisfaction has fallen 4.8 points, from 113.3 in March to 108.5 in September. The index for expectations has fallen more than twice as much at 10.1 points. While one survey is not conclusive the difference does provide insight into the concerns of American households.

Reuters

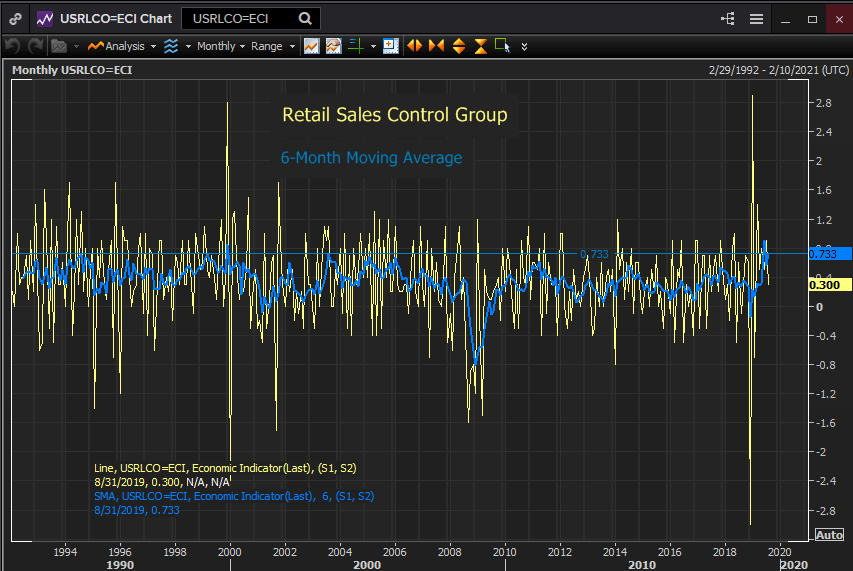

Retails sales

Consumers’ spending decisions come down on the current side of the above current conditions/expectations ledger. The retail sales control group category, which inform the GDP calculation, averaged a monthly increase of 0.733% from March through August. That was the highest average in 16 years. Consumption is being driven by the positive realities of jobs and wages whatever external factors are creating anxieties for American households.

Reuters

Conclusion

Consumer sentiment remains positive though at the low end of the elevated range of the last two years. The recent decline in sentiment is not normally associated with a labor market at full employment and with historically low jobless rates.

External factors from politics in Washington to the trade dispute with China and even the European Brexit wrangle and the length of the economic expansion likely play a part in the plunge in attitudes. Consumer sentiment took a similar dive in January when the partial government shutdown was making headlines for several weeks but recovered when the closure ended.

Consumers are optimistic but their concerns are realistic and rising. Attitudes will be determined by developments in the China trade argument and by the political drama being played out in the nation’s capital.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.