FOMC in the rear-view mirror – NFP eyed

The update from May’s FOMC rate announcement proved more dovish than expected, which naturally weighed on the US dollar (sending the DXY to lows of 105.44) and US yields, as well as, initially at least, underpinning major US equity indices.

The FOMC left the Fed funds target rate unchanged for a sixth consecutive session at 5.25%-5.50%, which was widely expected.

Rate statement

Key points to note from the accompanying rate statement was the sentence change regarding inflation, noting the lack of further progress on inflation, compared to the previous rate statement, which observed that there had been progress on inflation: ‘In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective’.

Another key observation, albeit small, was the replacement of the word ‘moving’ with ‘moved’ to possibly indicate an economy that is stalling: ‘The Committee judges that the risks to achieving its employment and inflation goals have moved toward better balance over the past year’.

The rate statement kept the original passage regarding needing greater confidence that inflation is moving sustainably towards the 2% inflation target. Another observation was the note of the quantitative tightening runoff. As of 1 June, the Fed will begin slowing the pace of QT from US$60 billion to US$25 billion per month.

Press conference

The takeaways from the press conference were that a rate hike is ‘unlikely’ and that Fed Chair Jerome Powell’s base case scenario still includes rate cuts this year. You may recall that some desks were expecting the Fed to adopt more of a neutral vibe, in which a rate cut would be just as likely as a rate hike.

Powell also noted that his ‘personal forecast’ was that inflationary pressures would begin to subside again this year.

Asked whether the Fed has time to cut three times this year, the Fed Chief responded that the Fed continues to seek confidence in disinflation progress, which has yet to be seen in Q1. Powell also communicated that it ‘appears’ it will take the central bank longer than anticipated to reach that level of confidence. He added that when the Fed ‘gets that confidence, then rate cuts will be in scope’.

The crux of the FOMC meeting, then, was that the Fed remains in a good place with current policy, and we are far off talks of a rate hike. However, a rate cut is also still not firmly on the table until progress in disinflation is observed.

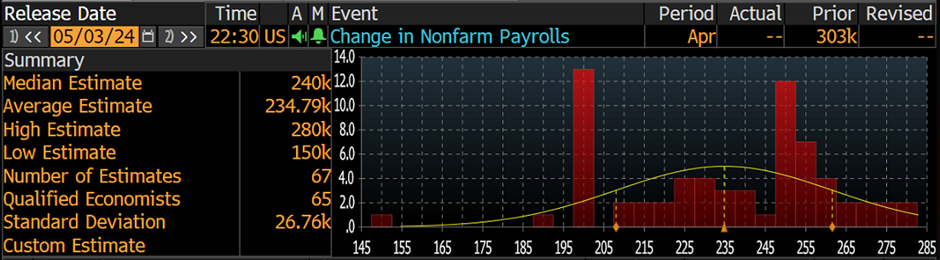

April’s US employment situation report in view

The US Employment Situation Report is set to take the stage at 12:30 pm GMT tomorrow.

According to Bloomberg, the median estimate heading into the non-farm payrolls change is for the US economy to have added 240,000 new jobs in April, down from the beat we saw for March at 303,000. Important to note is that the estimate range for the upcoming release is broad: between 280,000 and 150,000, with an average at 235,000. You may recall that we have seen NFP surpass expectations for five straight months. The question is whether we’ll see history repeat itself tomorrow.

Unemployment for the month of April is expected to remain unchanged at 3.8%; the estimate range for this print falls in between 3.9% and 3.7% (average is 3.81%), as per Bloomberg’s estimates. Finally, average hourly earnings is expected to rise +4.0% on a year-on-year basis in April, down from March’s +4.1% reading (the estimate range is between +4.2% and +4.0%), while month-on-month average hourly earnings are expected to rise +0.3%, matching March’s reading.

Data ahead of the event

Leading up to the event, a beat in ADP non-farm employment numbers was seen, with private establishments adding 192,000 new jobs to the economy in April, beating expectations of 179,000 and from March’s 208,000 reading. Albeit a market-moving risk event, its effectiveness as a precursor for tomorrow’s headline number is pretty much useless.

The latest Job Openings and Labor Turnover Survey (JOLTS) report for March revealed a decline to its lowest level since early 2021 to 8.488m from 8.813m. So, essentially, what we have here is less job openings and fewer quits – the quit rate fell to 2.1% (the lowest rate since summer 2020). This represents a weakening labour market and presents a downside risk for tomorrow’s release.

Further, the ISM manufacturing index fell back into contractionary territory (<50.00), falling to 49.2 (versus expectations of 50.0 and the prior release of 50.3), with the employment index contracting at a slower pace at 48.6, up from 47.4 (marking its 7th consecutive sub-50 release) and the prices paid index increasing to 60.9 from 55.8, which indicates a resurgence in inflationary pressures in the manufacturing sector (increasing at a faster rate of change, which, of course, is not something the Fed will want to see). You may also recall that the Global S&P PMIs for April released last week for the US showed a broad miss across the board for manufacturing and services. We also saw the employment component slide 3.2 points to 48.0.

More recently, the initial jobless filings remain unchanged from the previous release of 208,000 (a slight upward revision in the previous week’s number). Of note, this indicator has remained around 210k since February.

Market reaction

A broad beat in tomorrow’s data will likely bid US yields and the USD higher, potentially prompting more hawkish repricing in rates and weighing on equities and gold. However, a miss in data is likely to have the opposite effect.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,