Narrowly smaller US trade deficit in March

Summary

The U.S. international trade deficit narrowed modestly in March, but consistent with the Q1 GDP data out last week, the deficit was wider for the quarter. Underlying trade flows remain volatile, but stronger domestic growth should support further widening in coming months.

Trade flows flip in March

U.S. trade flows flipped direction in March with both exports and imports pulling back to end the first quarter. Total exports declined $5.3 billion during the month, while imports were down $5.4 billion. The just slightly larger drop in imports led the overall trade balance to narrow modestly to a deficit of $69.4 billion in March from $69.5 billion the month prior (chart).

Trade flows are volatile month-to-month, but the nearby chart shows both exports and imports are holding up. Imports have broadly recovered on trend since the middle of last year, despite remaining about $21 billion below its peak reached two years ago. Exports have been a bit more stable, and while total exports have largely moved sideways in recent years, exports hit a fresh new high in February.

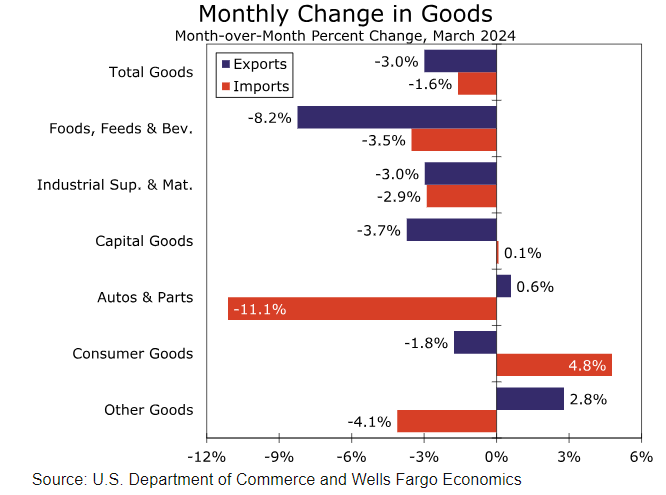

Most of the import weakness in recent years is tied to industrial supplies and consumer goods specifically. The mere stalling in the manufacturing space and pivot from goods spending back to services is consistent with a pullback in domestic demand in these categories. Yet while domestic manufacturing remains constrained by elevated borrowing costs and increased economic uncertainty generally, consumer spending continues to demonstrate resilience. Consumer goods imports have begun to recover as a result and were the fastest growing major category of imports in March (chart). Other areas were notably weak including industrial supplies, which slipped at the fastest pace in nine months, and autos which declined by the most since May 2020.

U.S. export weakness was a bit more evenly spread across major components but the largest drop in any end-use category of goods came from civilian aircraft, which slid $1.2 billion in March. We expect this is more noise than evidence of slower deliveries. This line item is very volatile on a month-to-month basis (aircraft rose $1.4 billion in February) and separately released data from Boeing show steady deliveries throughout the first quarter. Regardless, that weakness caused overall capital goods exports to slip at the fastest pace since February 2021 in March. Elsewhere, industrial supplies and consumer goods exports were down while autos eked out a modest increase.

The March trade data largely confirm what the Q1 GDP report last week suggested; net exports were a sizable drag on first quarter growth. Weaker industrial supplies exports were responsible for most of the weakness in exports for the first quarter as a whole, while solid consumer and capital goods led to a pick-up in imports. Stronger Q1 import growth sets the second quarter up for some tough base comparisons. With domestic strength continuing to show signs of outpacing international conditions, we expect net exports to remain a drag on growth in the near term, but likely less so than the 0.9 percentage points subtracted in the first quarter.

Author

Wells Fargo Research Team

Wells Fargo