US Dollar Forecast: Attention will be on Powell’s testimonies and US CPI

- US Dollar Index (DXY) sharply reversed its recent weekly uptrend.

- A dovish Powell in Sintra fanned the flames for a September rate cut.

- Powell’s semi-annual testimony and US CPI come to the fore.

A needed correction ahead of extra gains

All that goes up must eventually come down. Consequently, the Greenback felt the effects of gravity in the FX market this past week, experiencing strong selling pressure after reaching multi-week highs above the 106.00 barrier as measured by the USD Index (DXY). This index compares the performance of the US Dollar (USD) against a basket of six major currencies (Euro, Japanese Yen, Swiss Franc, Canadian Dollar, British Pound, and Swedish Krona). In this context, the index ended the week with losses for the first time after four consecutive weeks of gains.

The Fed and central banks maintain divergent policies

The pronounced retracement in the index these past few days came mostly in response to investors’ repricing of a potential interest rate cut by the Federal Reserve (Fed) sooner than previously anticipated.

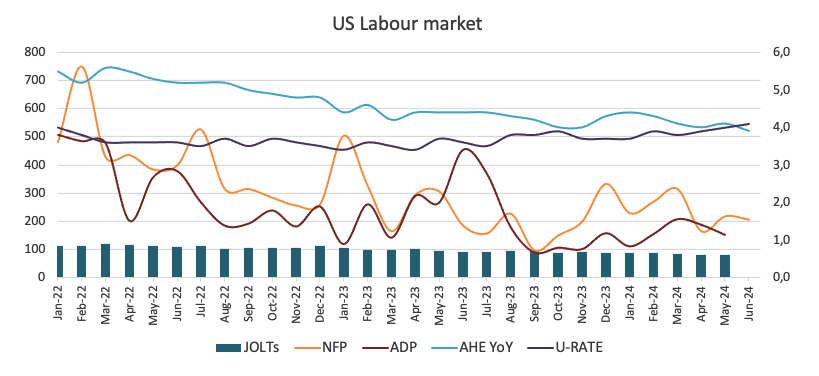

The above was mainly underpinned by disenchanting results from US fundamentals throughout the week, with the focus ostensibly on the labour market and, secondly, on the services sector. The exception was, once again, another solid print from US Nonfarm Payrolls, where the economy added more jobs than initially estimated in June (+206K), although the Unemployment Rate ticked higher for the third month in a row, now hitting 4.1%.

Among the G10 central banks, the European Central Bank (ECB) reduced its rates by 25 bps early in June, although it maintained the uncertainty around probable extra rate cuts in the latter part of the year. Moreover, the Swiss National Bank (SNB) surprised markets with an additional 25 bps cut on June 20, while the Bank of England (BoE) issued a dovish hold on the same day. Similarly, the Bank of Japan (BoJ) conveyed a dovish message on June 14. In stark contrast, the Reserve Bank of Australia (RBA) is seen kicking off its easing cycle in H2 2025.

The debate over one or two rate cuts by the Fed remains well in place

Despite rising market chatter regarding the possibility of an anticipated kickstart of the Fed’s easing cycle, which should give some credit to the markets’ view of two 25 bps rate cuts this year, this is not the view shared by the Committee, as it has advocated for just one interest rate reduction at its latest meeting on June 12. That scenario should most likely materialize at the December 18 event.

The re-emergence of disinflationary pressure, indicated by the US Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE), along with a recent slowdown in key areas such as the labour market and the services sector, seems to have led market participants to anticipate two interest rate cuts by the Fed this year, most likely in September and December.

According to the FedWatch Tool by CME Group, there is approximately a 75% chance of rate cuts at the September 18 meeting and nearly a 96% likelihood of lower rates by the end of the year.

Also contributing to the weekly decline in the US Dollar emerged the lack of surprise from Fed officials, whose comments broadly matched what markets had already digested, namely, that the Fed needs more time to evaluate that inflation is convincingly moving towards the 2% goal.

It didn’t help either the dovish tone by Fed’s Chair Jerome Powell in his participation at the ECB Forum in Sintra (Portugal), where he expected inflation to edge down next year, potentially reaching the mid-to low-2s by mid-2025 and possibly reaching 2% by late next year. Powell also expressed his belief that the domestic economy is nearing a point where there is a tradeoff for monetary policy between the Fed's goals of full employment and price stability. Additionally, he indicated that the bank still needs more data before cutting interest rates to ensure that recent weaker inflation readings accurately reflect underlying price pressures.

Earlier in the week, Federal Reserve Bank of New York President John Williams (permanent voter) stated that he continues to believe price pressures are moderating back to the levels targeted by the central bank.

Collaborating with his colleagues, Chicago Federal Reserve Bank President Austan Goolsbee (2024 voter) remarked that he sees some "warning signs" of weakening in the economy. He added that the Fed’s goal is to reduce inflation without stressing the labour market.

US yields accompanied the US Dollar’s retracement

The Greenback has started the month on the defensive, as it has US yields across the spectrum, all against the backdrop of reignited (unjustified?) speculation that the Fed might start reducing its interest rates sooner than expected by the Committee.

Markets’ view of rate cuts is challenged by the Fed's hawkish narrative

Persistent, albeit reiterative, hawkish Fedspeak favours extra patience, and further evidence of inflation’s path towards the Fed’s target maintains its collision course with the market’s belief of two interest rate cuts in the latter part of the year.

Meanwhile, the constructive bias in the Dollar appears reinforced by consensus among Fed officials; hence, the likelihood of an extra advance in the currency remains well on the table in the long term. And if we bear in mind that market axiom that says you cannot beat central banks...

Moving forward, there are almost non-existent chances of a change of tone at the upcoming Chief Powell’s semi-annual testimony next week, which should leave the Greenback vulnerable and exposed to potential deeper pullbacks.

Upcoming key events

Next week features Powell’s semi-annual testimonies on Tuesday and Wednesday, while the release of inflation figures for June tracked by the Consumer Price Index (CPI) should also be at the forefront of investors’ attention on Thursday.

Techs on the US Dollar Index

The DXY is expected to maintain its bullish outlook while it trades above the 200-day SMA.

However, if the index rises above the June high of 106.13 (June 26), it might face the 2024 top of 106.51 (April 16). Once it clears this zone, DXY is likely to visit the November peak of 107.11 (November 1) before reaching the 2023 high of 107.34 (October 3).

On the other hand, the crucial 200-day SMA at 104.49 might provide some early contention before the June low of 103.99 (June 4). A deeper drop might bring the weekly low of 103.88 (April 9) back into focus, ahead of the March low of 102.35 (March 8) and the December bottom of 100.61 (December 28), all before the psychological conflict zone of 100.00.

Economic Indicator

Fed's Chair Powell testifies

Federal Reserve Chair Jerome Powell testifies before Congress, providing a broad overview of the economy and monetary policy. Powell's prepared remarks are published ahead of the appearance on Capitol Hill.

Read more.Last release: Thu Mar 07, 2024 15:00

Frequency: Irregular

Actual: -

Consensus: -

Previous: -

Source: Federal Reserve

US Dollar PRICE Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Canadian Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.14% | -0.36% | -0.32% | 0.17% | -0.24% | -0.34% | -0.24% | |

| EUR | 0.14% | -0.23% | -0.19% | 0.32% | -0.10% | -0.19% | -0.12% | |

| GBP | 0.36% | 0.23% | 0.04% | 0.55% | 0.14% | 0.04% | 0.10% | |

| JPY | 0.32% | 0.19% | -0.04% | 0.49% | 0.09% | -0.02% | 0.07% | |

| CAD | -0.17% | -0.32% | -0.55% | -0.49% | -0.43% | -0.51% | -0.45% | |

| AUD | 0.24% | 0.10% | -0.14% | -0.09% | 0.43% | -0.10% | -0.02% | |

| NZD | 0.34% | 0.19% | -0.04% | 0.02% | 0.51% | 0.10% | 0.06% | |

| CHF | 0.24% | 0.12% | -0.10% | -0.07% | 0.45% | 0.02% | -0.06% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.