Trump speech to Congress next Tuesday should move markets

Outlook:

Markets are still responding to the consensus view of "Not March," even though that is not what the Fed said and there are several Feds hinting as hard as they can that March is a real possibility. The "Not March" idea is considered to be behind the slip-sliding note yield and dollar.

As of 8:14 am ET today, the 10-year yield has slipped down further to 2.355%. The WSJ reports that the bond trade had been getting overcrowded and some of the dip can be due to covering or just plain exits. But even so, the bond gang doesn't attribute credibility to the Fed, and that has to be a nagging worry. The CME Fed funds futures give a 22% chance for a hike at the March meeting (under the Bloomberg version), with May at 52% and June at 70%.

The WSJ reports "... the odds for March may rise if upcoming data bolster the chance for the Fed to act. Analysts say the Fed may be hesitant to pull the trigger if the odds remain modest because policy makers don't want to spook markets." One analyst said the bond market "is very skeptical of this Fed, and given their history, it is hard to argue against that thesis." Oh, dear.

Elsewhere, Treas Sec Mnuchin has been making some practice swings. Yesterday he said the tax plan will take a while to get organized and he hopes to have it ready before the August Congressional recess. Then, assuming it's passed right away, we still need a year and more to get effects. This is a reasonable stance, although obviously downplaying the announcement effect. As a seasoned fund manager, Mnuchin must be well-acquainted with the announcement effect. It is a footnote so far that Mnuchin said he has yet to make a judgment on the Chinese currency. It's a little curious that when Trump trumpets big tax changes, markets jump, but a sane comment by Mnuchin gets a yawn.

Before Trump next week, tomorrow we get Buffett's shareholder letter after Berkshire Hathaway releases earnings. This could be fun. One year, Buffett got universal press coverage by saying he paid less in taxes than his secretary.

Next up at bat is Trump, who makes a speech on something/anything/everything to a joint session of Congress next Tuesday. Ahead of time, that morning, Trump will appear on TV to preview some of what he will say. As far as we know, no president has done that before. Maybe it's good thing to move on from dull and pompous conventions, but this show-biz aspect of the Trump presidency is unsettling, especially because Trump is unscripted and likes to shock and dismay. This is one more way for Trump to own the news cycle for a full day.

Then the home team is up. Congress has been struggling with tax reform for decades and it's a particular hobby of House Speaker Ryan. Ryan has firm views on conservative fiscal policy, meaning smaller government that costs less and targets a reduction in the deficit. US debt is now $19.94 trillion, although as a percentage of GDP, contracting a bit (from 3.2% in 2016 to 2.6% this year). Trump doesn't give a hoot about the debt or the size of government. He favors strong government and that does not imply contracting size or cost. The old conservative wing of the party is on the ropes, to mix metaphors, but a battle royal could be forming between the President and the Speaker.

Nevertheless, the Trump speech to Congress next Tuesday is an Event that should move markets, including ours.

The other big political event comes later, in France, but before then, we have polls. Market News reports "On Wednesday, two-year Schatz yields posted a new record low of -0.915%, which was seen as a sign of ongoing safe-haven demand driven by French election uncertainty. Two-year yields closed at -0.906% Thursday." So far today, the yield has fallen further, to -0.96%, another record low.

LePen opponent Macron is gaining in polls after joining with another centrist. "The Ipsos Fiducial poll said Macron would take 22.5% of the first-round vote on April 23, up from 19% in Wednesday's poll. Thursday's poll said National Front leader Marine Le Pen would take 26.5%, unchanged from Wednesday, and former prime minister Francois Fillon would win 20.5%, up from 19%.

"The Ipsos poll projected that Macron would defeat Le Pen in the May 7 second-round vote by a margin of 61% to 39%, a larger margin that the 60%-40% spread in Wednesday's poll."

Don't forget that LePen is not the only political risk. The Netherlands also faces far-right populism. Should we link the less-bad election outlook in France to the improving euro? Maybe. The lowest low as on Wednesday (1.0468), before the centrist alliance. Yesterday the euro rose steadily and this morning, it is breaking red resistance. Market News reports "The euro's inability to close below $1.0500 has players rethinking their bearish bias and wondering if the pair may remain in a $1.0500 to $1.0800 range a while longer." Here's an interesting fact: the euro high so far this year is 1.0812 from Jan 31, itself the highest since Dec 8 when the ECB offered what has been named a "dovish taper." So, in addition to the falling LePen fortunes, we get the ECB sneaking back into the mix. Mr. Draghi probably doesn't want a stronger euro and certainly not one predicated on a taper he is not entertaining, but a stronger euro may be preferable to one that is tanking on political fear.

Fear may be reduced but it's not gone. Analysts, including Brown Brothers' Chandler, focus on the 2-year, the tenor most influenced by current affairs. "Few can keep up with the demand for German pa-per. The German two-year yield fell nine basis points and draws closer [to] minus 1.0%." The FT has a record low minus 0.96% this morning, "a level that many traders believe is caused by a scramble for supposed safety in case the anti-EU Marine Le Pen wins the French presidential election in May." Chandler goers on, "French and Dutch yields are only 4-6 bp. Part of Germany's outperformance, we argue, is part of the scarcity that is derived from the German fiscal position, Eurosystem purchases, and the use of German paper for collateral as well as investment.

"Still, regardless of the reason that German rates are falling, the widening discount it offers vis a vis the US, weighs on the euro. ... The German discount to the US on two-year rates is at 2.13% now. It is widened for the fifth consecutive week."

Well, it's not very weighty. We can see the action is more in the German yield but the US 2-year is actually lower, too. It's just that the German 2-year is lower still. This is not the same thing as the US yield rising organically on growth and inflation expectations, not least because the factor vanishes in a puff of smoke once the elections are over. Then the European yields can normalize higher while the US yields are doing—what?

Bottom line, the falling German 2-year yield "should" weigh on the euro, but that's not what we are seeing of the euro chart. Why? Is it because of lack of confidence in the divergence theory, since one side is not diverging as it should?

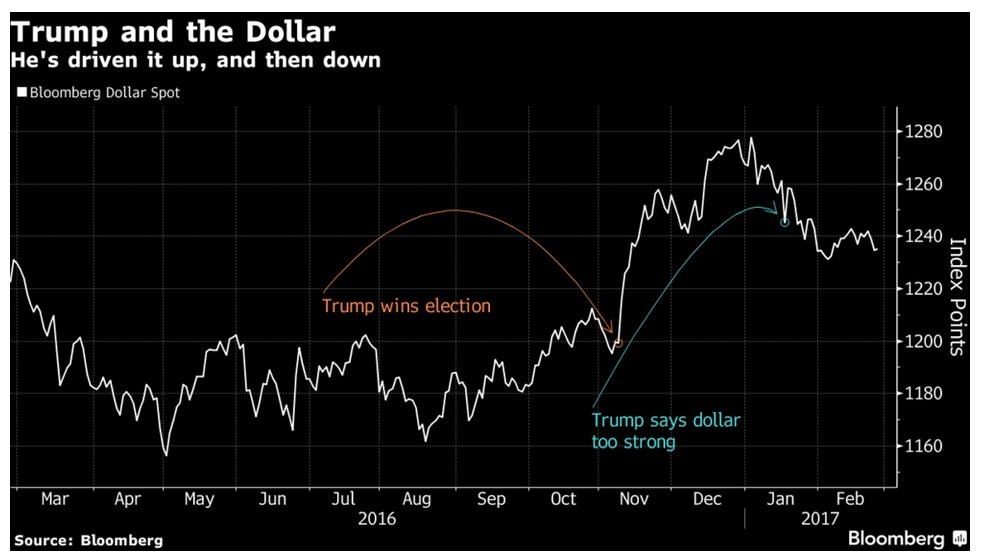

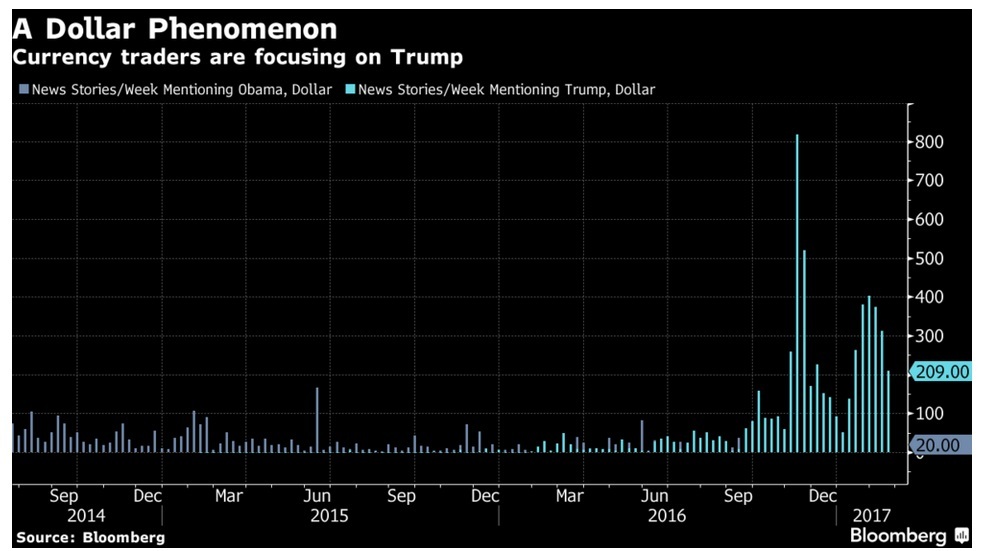

Finally, Bloomberg has a story vindicating our new attentiveness to Trumpian developments in the FX market. "While policy pledges drove the greenback's 3.9 percent gain in November, its best rally in more than two years, pronouncements on the currency, and its peers, from him and his administration have whiplashed traders over the past six weeks."

See the first chart. But even more interesting is the second chart showing that news stories combining "Trump and dollar" are at unprecedented highs. We are not nuts.

Political tidbit: The big move up in the peso yesterday may have a short shelf life. At the same time Tillerson and Kelly were trying to soothe rightfully ruffled feathers, Trump was in Washington telling company execs that the US is sticking it to Mexico. Trump says the deportations are "military" while Tillerson and Kelly said specifically they are not military and just a continuation of the Obama methodology.

Here's another battleline: CNN reports "The President has also ordered Cabinet agencies to inform him of the total direct and indirect aid the US gives Mexico, a move that some see as an attempt to amass some leverage in the debate over the border wall that Trump insists will be built and that Mexico will pay for. Mexican officials have repeatedly said they will do no such thing.

"Under the Merida Initiative, the State Dept has given Mexico $2.6 billion since 2008. That's to strengthen rule of law, counter narco-trafficking, support judicial reform and police professionalization. It doesn't include aid from other State Department programs. Mexico also gets funding from the departments of Defense, Energy, Labor, Health and Human Services, Interior, the Peace Corps, the US Agency for International Development and DHS. Kelly distributed an implementation memo on February 21 asking his staff to calculate how much direct and indirect aid DHS gives Mexico. That process is still underway."

It is Trump's practice to hit the other guy on the other side of the table over the head with a baseball bat and then "negotiate" from a position of strength. It's the same practice used by 3-year olds screeching in a store or restaurant. Parents will give the kid almost anything to shut him up. Trump has insulted Mexico repeatedly and now threatens not only a wall, but to withhold billions in aid. To be sure, we will be interested to hear how much the total adds up to. The American public is already upset about aid to Israel, Pakistan and others. Never mind that many other countries give more on a per capita basis. And never mind that at least some of that dough keeps the brown people on the other side of the border. This "nationalism" is going to be a trainwreck.

Political tidbit 2: in the UK, the UKIP party failed to carry Stoke-on-Trent, which had a 70% vote pro-Brexit last June. Stoke is "The Potteries," where all those glorious teapots were made in the golden age of British manufacturing. Think Minton. It's the next town over from where we went to college, one of the "new" colleges designed to compete with Oxbridge, the University of Keele. Stoke used to be resolutely pro-labor and this time voted for the Labour guy even though he was from another district. In the other place where an election was held (Copeland), Labour took the Tories and UKIP, for what the Guardian reports is "the first time a governing party has taken a seat from another party in a byelection in 35 years."

So what? The UKIP movement, i.e., pro-Brexit, is fading fast now that reality-checking is setting in. Americans never like to admit it, but Britain quite often leads (Thatcher before Reagan). The implication is that the Trump notionally "populist" revolution may not have long to live. After all, we do appreciate expertise and knowledge. Hiring a bunch of amateurs to run the biggest enterprise in the world, the US government, was pretty stupid.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 112.34 | SHORT USD | 02/17/17 | WEAK | 112.86 | 0.46% |

| GBP/USD | 1.2549 | LONG GBP | 01/24/17 | WEAK | 1.2451 | 0.79% |

| EUR/USD | 1.0585 | SHORT EURO | 02/10/17 | WEAK | 1.0643 | 0.54% |

| EUR/JPY | 118.92 | SHORT EURO | 02/03/17 | WEAK | 121.56 | 2.17% |

| EUR/GBP | 0.8435 | SHORT EURO | 02/16/17 | WEAK | 0.8490 | 0.65% |

| USD/CHF | 1.0059 | LONG USD | 02/10/17 | WEAK | 1.0024 | 0.35% |

| USD/CAD | 1.3096 | LONG USD | 02/22/17 | STRONG | 1.3174 | -0.59% |

| NZD/USD | 0.7228 | SHORT NZD | 02/10/17 | STRONG | 0.7185 | -0.60% |

| AUD/USD | 0.7705 | LONG AUD | 01/05/17 | WEAK | 0.7343 | 4.93% |

| AUD/JPY | 86.56 | LONG AUD | 02/09/17 | WEAK | 85.92 | 0.74% |

| USD/MXN | 19.6776 | SHORT USD | 01/31/17 | WEAK | 20.8108 | 5.45% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat