GBP/USD Weekly Forecast: Can UK hope continue defeating global gloom? Fed, US GDP, virus all eyed

- GBP/USD has advanced amid vaccine hopes but suffered amid external tensions.

- Coronavirus developments, Brexit, the Fed decision, and US GDP are all eyed.

- Late July's daily chart is showing bulls are in control.

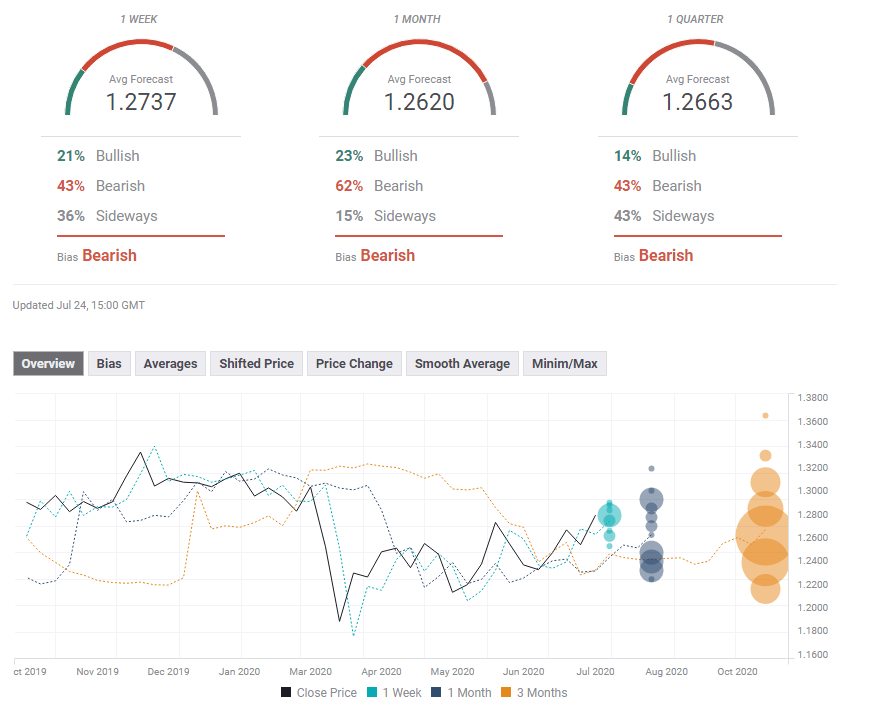

- The FX Poll is showing that investors are bearish on all timeframes.

British vaccine researches and an American-style shopping spree in the UK have boosted the pound, defying worsening international relations and US coronavirus figures. These themes will likely continue dominating with significant additions from the Fed and US growth figures.

This week in GBP/USD: Vaccine hopes vs. international tensions

British science is surging forward. The University of Oxford and AstraZeneca reported substantial progress in developing a coronavirus vaccine. The Phase 1/2 trial proved safe and able to develop what scientists call "double protection."

While the results of Phase 3 are awaited, Synairgen, a smaller pharma firm, said its medication is efficient in keeping COVID-19 patients from deteriorating. Both announcements and other efforts have boosted sentiment and supported the pound.

Even before there is solid medicinal mitigation to the malaise, UK shoppers have returned to the streets, taking advantage of the reopening – and also spending some of the funds granted by the government – to catch up. Retail sales leaped by 13.9% in June and are close to 2019 levels.

Markit's preliminary Purchasing Managers' Indexes for July also showed ongoing recovery.

Sterling also received support from across the Channel, as EU leaders finally agreed on a €750 billion recovery fund. The decision boosted global stocks and also provides hope for greater European demand for British products.

On the other hand, Brexit negotiations have not gone anywhere fast. Micheal Barnier and David Frost, negotiators for the EU and the UK respectively, both confirmed a lack of progress in talks. Reports that Britain would abandon the negotiation table proved premature, and the denial helped sterling find its feet.

While stability characterizes relations with Brussels, London and Beijing are growing further apart. Prime Minister Boris Johnson's decision to cancel the extradition treaty with Hong Kong – in response to China's tightening of its grip over the city-state – has angered the world's second-largest economy and may impact investment.

Sino-American relations intensified as well. The US closed China's consulate in Houston, alleging it of illegal activity in the Texan city. US Secretary of State also delivered a stinging speech against China's authoritarian regime and criticized its president Xi Jinping. China responded by shutting down the US consulate in Chengdu.

Pompeo did stress that the trade deal between the two superpowers remains intact, providing some comfort to investors. On the other hand, America's top diplomat and his British counterparts failed to advance trade talks during Pompeo's visit to London.

The US continues struggling with COVID-19, as infections topped four million and deaths surpassed 144,000. The disease's economic impact is becoming more evident in economic figures, with jobless claims rising for the first time after 15 weeks of decline.

Coronavirus has also shifted the political approach. President Donald Trump made an abrupt U-turn, admitting the situation will get worse before it gets better and called fellow Americans to wear face masks. He is responding to his unfavorable polling figures, showing that his support is highly correlated to his mishandling of the virus.

UK events: Brexit deadlock, coronavirus, and China

Brexit talks were stuck, are stuck, and will likely remain so for another week. Nevertheless, low expectations do not mean lack of attention by markets, which will likely shrug off any reports about disagreements but may respond to a surprising breakthrough or if one side abandons the talks – a low probability event.

UK coronavirus headlines have fortunately been on the backburner as numbers continue falling. That would allow further gradual removal of restrictions, supporting the pound. A worrying increase in cases – as seen in some countries on the continent – would send sterling lower.

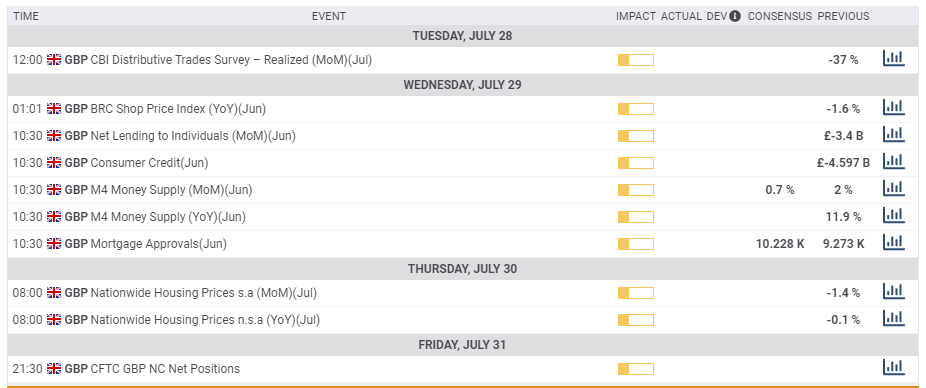

The economic calendar is light in the upcoming week. Consumer credit figures for June and house prices for July may gain some attention.

Here is the list of UK events from the FXStreet calendar:

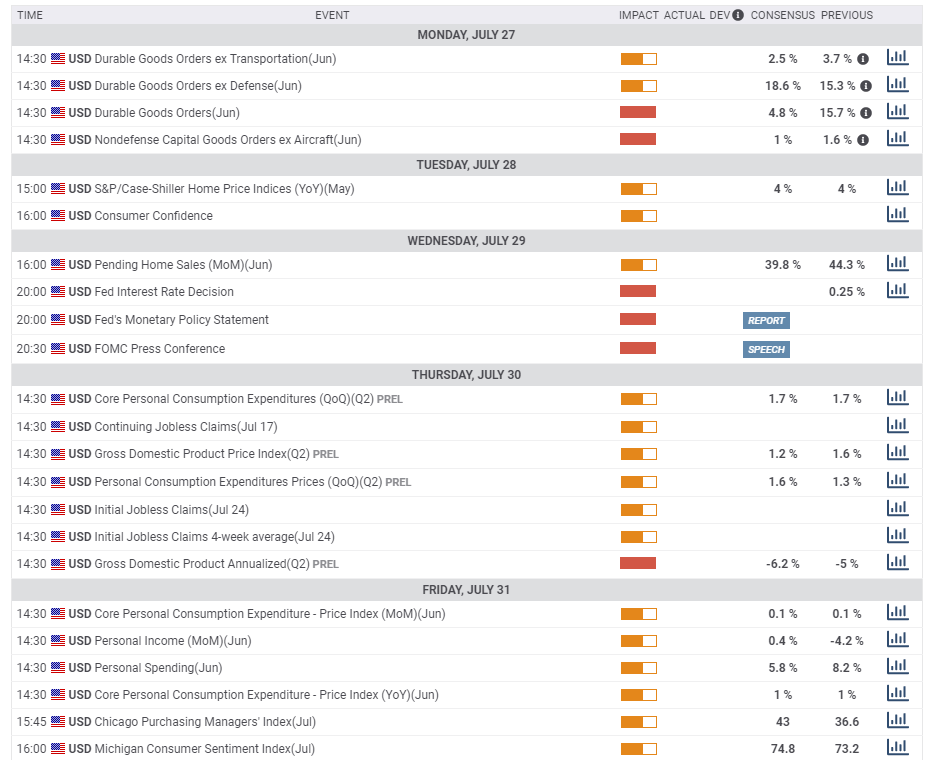

US events: Fed, GDP, and coronavirus compete for attention

Democrats and Republicans may make some noise but they are likely to strike a deal on extending federal unemployment benefits, support to small businesses and other emergency steps. Nobody wants to be seen as hitting the economy while it is down – and especially in an election year.

Investors will probably focus on coronavirus statistics, new restrictions in the states that are suffering, and easing in the rare places they are receding in. Several forward'looking figures have already shown the economic impact of this second wave, and both soft and hard data will provide an updated view of the economy now.

The busy calendar kicks off with Durable Goods Orders for June – the month which saw the turn from fast reopening to consumers hunkering down once again. Economists expect all figures to extend their recovery.

The more up-to-date Consumer Confidence gauge by the Conference Board will likely fall, following the parallel measure from the University of Michigan.

The highlight of the week is the Federal Reserve's decision on Wednesday. The world's most powerful central bank will likely refrain from action once again after immense action beforehand. The Fed continues buying bonds and is committed to keeping low rates for longer.

Jerome Powell, Chairman of the Federal Reserve, will likely urge elected officials to act and may be asked about the next steps and about the stock market rally – of which the Fed is the main underwriter.

See Fed Preview: Warming up to controlling the yield curve, nudging lawmakers, keeping markets happy

The Fed competes for attention with the first release of Gross Domestic Product for the second quarter which is set to confirm a recession – the first since 2009. The economic calendar is pointing to a drop of 6.2 annualized but estimates vary widely. The economy squeezed by 5% in the first quarter.

Apart from the headline figure, investors will pore into the details, with Personal Consumption and government contribution standing out. Weekly jobless claims are due out at the same time as GDP and could continue showing a concerning increase. Continuing claims are for the week of July 17, when Non-Farm Payrolls surveys are conducted.

The week and the month-end on Friday, raising the chances for a highly volatile session as money managers adjust their portfolios. Several economic figures could also rock markets./ Personal Spending likely extended its recovery in June while the final UoM Consumer Sentiment is set for a minor upgrade.

The presidential elections are still far off and it would probably take outlandish polls to move markets in a week packed with data. Politics will likely grab attention later on.

Here the upcoming top US events this week:

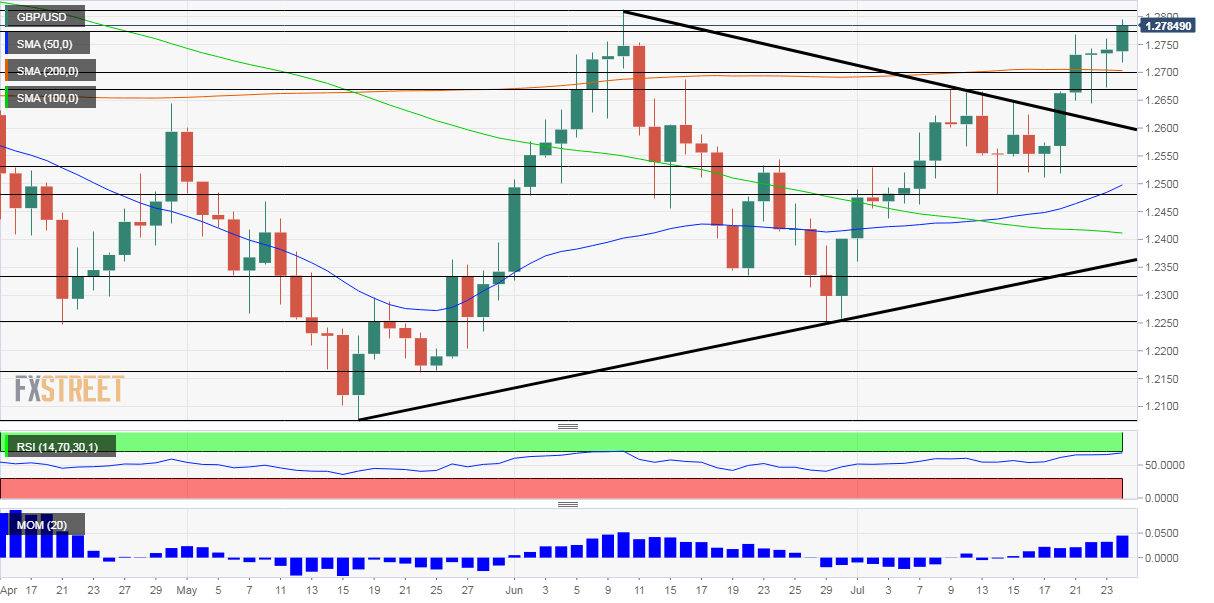

GBP/USD Technical Analysis

Pound/dollar has broken above the 200-day Simple Moving Averager and the downtrend resistance line that had capped it since early June. The bullish bias is compounded by upside momentum. So far, GBP/USD is still not overbought, as the Relative Strength Index is still below 70.

Resistance is at 1.2770, touched twice in late July, and emerging as a double-top. It is followed by 1.2815, June's peak. Further above, 1.2845 and 1.2980 are eyed ahead of the round 1.30 level.

Support waits at 1.27, where the 200-day SMA hits the price, followed by 1.2665, a swing high from early July. It is followed by 1.2534, a high point in early July. It is followed by 1.2470, a swing low earlier in the month.

GBP/USD Sentiment

While the UK economy has surprised with its recovery, headwinds coming from deteriorating international relations and emerging overbought conditions may limit further gains.

The FXStreet Forecast Poll is showing that experts are doubting the rally and see a downward correction. However, the average targets have been upgraded in the past week.

Related Reads

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.