Week Ahead on Wall Street: Poor sentiment leads to new lows, but is October set up for a bear market rally?

- Wild swings in sterling create a risk of contagion.

- Apple suffers a massive meltdown, and Tesla misses deliveries.

- Credit Suisse in turmoil as bank moves to reassure investors.

It was an incredible week in financial markets, which is something we seem to be saying every week lately. This one truly was,however, due to the sudden risk of a mini-Lehman event in the UK spreading havoc across global markets. The big news was in the UK where sterling reacted negatively to the UK borrowing a bucket load of money to basically cut taxes for the top 10%. By eliminating bankers' bonus restrictions and also eliminating the top rate of tax, the new UK Prime Minister and Chancellor set out on a very shaky path.

Sterling markets reacted with fury over plans to increase borrowing, sending sterling and UK gilts into free fall. The Bank of England then intervened in gilt markets to try and stem the damage. Later we learned the reason was a near meltdown in the pension industy, which would have led to a mini-Lehman moment. This sent risk assets into a tailspin and put the dollar once again on the charge. Sterling fell to a record low versus the dollar before correcting on the Bank of England intervention. This Bank of England intervention was basically a pivot and so risk assets took off higher on the news. Investors have been hoping for a Fed pivot to put a floor under risk assets all year.

Soon it became clear that this may be a case of being careful with what you wish for. The Fed is only likely to pivot if we are entering another financial crisis. However, we do notice some stress in the messaging from Fed officials. They have been pretty uniform in their hawkish assessment of late, but on Friday we heard from Lael Brainard who mentioned financial stability worries. This was a noted divergence from the latest Fed missives and indicative of a potential pivot.

The macro environment remains challenging, and we have already gotten close to a major (or perhaps formerly major) economy in the UK reaching a breaking point. That increases the risk of a system breakdown, and Bank of America is out with a timely warning on the US Treasury market. Sober reading!

"Treasury Market Breakdown Is At Risk": Fed Markets Guru Has A Scary Warning For Powell https://t.co/fLwuoiW5Yv

— zerohedge (@zerohedge) October 3, 2022

The latest Leading Economic Indicator continues to decline, and that is not good news for equities as the below tweet outlines. Forward returns for equities are likely to be low. This adds to pressure from rising yields as there is now an alternative to equities from 4% to 5% yields on investment grade or sovereign debt.

This chart isn't positive for equities. H/T @Credit_Junk (check out his Substack!) https://t.co/qrjDFIZD3D pic.twitter.com/vjFd1UbtC2

— FX Macro Guy (@fxmacroguy) September 30, 2022

Bear in mind (excuse the pun) that we are far from bear market valuations just yet. It takes time to get there though, so do not get too impatient.

According to Bloomberg, if today were the bear market bottom it would be the highest P/E for the SPX of any bear market low since at least 1957. Average bear market low P/E = 12.6x, current P/E = 17.9x. pic.twitter.com/usn4N7ZR2n

— BWK Capital (@BwkCapital) September 26, 2022

Apple and Tesla stock woes

Things were of course not helped by the big daddy of them all – Apple (AAPL). The stock was down nearly 10% as Bloomberg first reported that Apple was asking suppliers not to increase production levels, and then Bank of America weighed in with a rare downgrade. A reminder here we have a $100 12-month price tag on Apple (AAPL). Read more here: Apple Stock Deep Dive: AAPL price target at $100 on falling 2023 revenues.

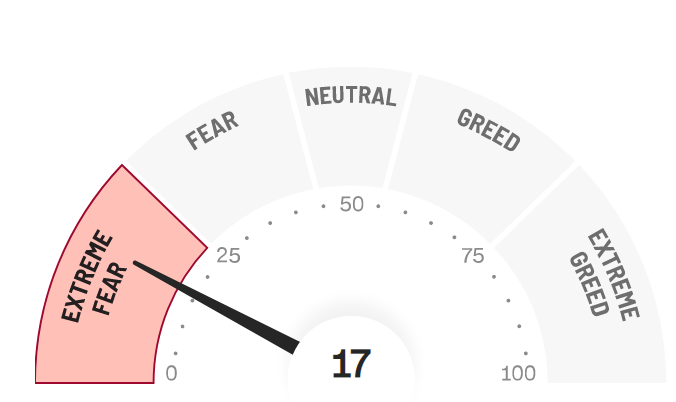

Now the second big daddy (well close),Tesla (TSLA), missed delivery estimates on Sunday, and the stock is already down 4% premarket. This will make any rally harder to take hold. There are some signs that a brief pause in selling pressure may be imminent though. Sentiment is terrible, and this is often a contra indicator. It worked well for the June rally. We have any number of metrics, but the most common, the CNN Fear and Greed index, is at a noted low.

Source: CNN.com

Seasonality is also in favour of a bounce with October being one of the strongest months historically. With earnings season soon to kick off, we are likely to see some derisking ahead of the event. We should also point out how much bad news is in the price. Apple is now marked down, Tesla to follow, we have had massive sell-offs in Nike (NKE) and FedEx (FDX). Tech remains pressured. This seems perfectly set up for a bear market rally in my view. We just need to get over this obsession with Credit Suisse!

Week ahead

Already OPEC is not helping with talk of a big supply cut sending oil prices up 4%. Risk assets do not like higher oil prices, so here we go again. The dollar too is testing the BOJ overnight as it heads back to 145. This move has been slower, so my feeling is the BOJ will not be in as much of a rush to sell dollars this time around. They will be there somewhere, but this melt-up has been much slower.

Already we have yet another UK pivot as the government ditches plans to cut the top rate of income tax. This is a victory for bond market vigilantes already then. The Soros playbook still lives on!

On Friday we will get the US employment report. This is one of the key events along with CPI. A strong showing is bad for risk assets in my view as it cements the recent hawkish tones from the Fed. It will also be a point of reference for the Fed as it has mentioned the employment market on several occasions. The Fed will feel comfortable hiking if the employment market remains strong.

Earnings week ahead

Not a huge week as we are near the main Q3 earnings season now.

#earnings for the week https://t.co/lObOE0dOhZ $TLRY $MTRX $AYI $LEVI $STZ $MKC $RPM $BYRN $HELE $SGH $LW $ACCD $CAG $NG $LNDC $SAR $RGP $RELL $ANGO pic.twitter.com/zAiNW0QPtW

— Earnings Whispers (@eWhispers) October 1, 2022

SPY forecast

Again here we see signs of a bottom. The SPY is approaching the 200-week moving average. This really needs to hold or it is: "Look out below!". We finally broke $362 with a low close on Friday, likely quarter-end markdown putting in a low bar for the quarter ahead. Still there is the possibility of a wash to $352, and that would make me more comfortable in prescribing another bear market rally. Also the Relative Strength Index (RSI) is close to oversold, so in my view the risk-reward is beginning to set up for a bear market rally, the timing is the tricky part. It always is!

SPY chart, daily

Economic data

All eyes are on Friday's employment report.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.