USD/JPY Forecast: Is the correction over? The Fed and the NFP decide

- USD/JPY slightly retreated from the highs as the market mood was mixed.

- A jam-packed week features the Fed and the Non-Farm Payrolls.

- The technical picture remains bullish for the pair. Experts have not moved their targets since last week.

This was the week: Robust US data, Softer BOJ

US data was upbeat. It began with New Home Sales coming out at 692K annualized for March. It then continued with robust investment data. Durable Goods Orders jumped by 2.7%, more than triple the expectations. Orders excluding defense and air rose by 1.3%, far above 0.1% projected. The figures supported the US dollar and raised expectations for the preliminary GDP data for Q1.

GDP indeed came out better than expected at 3.2%, but this was mostly priced in. The attention moved to the low level of inflation the data was based on. The low deflator means that nominal GDP was not that impressive. In addition, consumption failed to impress.

The components and the tepid market reaction that followed somewhat weighed did not help the pair.

See US GDP Quick Analysis: 4 reasons for the USD drop and why it can surge

The Bank of Japan left its policy unchanged as expected but sounded quite dovish. Governor Haruhiko Kuroda and his colleagues lowered growth forecasts, pledged to keep the interest rates at current, negative levels into 2020, and pushed back on their projections for reaching the elusive 2% core inflation goal.

The dovish stance of the Tokyo-based institution limited pullbacks in USD/JPY.

The US and China announced further high-level talks between US Treasury Secretary Steven Mnuchin, Trade Representative Robert Lighthizer, and Chinese Vice Premier Liu He. However, there were no reports of any breakthroughs, just a positive tone.

Fed decision - Not too dovish Fed

The central event of the week is the Fed decision. The world's most powerful central bank completed its dovish shift by entirely removing the hawkish bias and signaling no rate hikes in 2019. Moreover, they announced that the balance sheet reduction program would end in September. The neutral mode weighed on the US Dollar for a short time, before markets remembered that the US is beating the rest of the world.

At the May meeting, the Fed does not publish new forecasts nor the dot-plot, but investors will closely watch the tone on the economy, inflation, and any hint about the next move in interest rates. The labor market remains the strong point of the economy, while inflation is lagging. The recent growth data will be of interest.

Regarding interest rates, markets still see the next move by the Fed as a rate cut, and they may be in for a disappointment. While the central bank shifted to neutral, it remained optimistic about the economy, and this view has now been vindicated. If Powell leaves a rate hike on the table, whether this year or the next, the greenback has room to rise and stocks could fall.

The statement will likely remain mostly unchanged, but reporters and traders will scrutinize every word coming out of Fed Chair Jerome Powell's mouth.

Other US events: NFP in the limelight

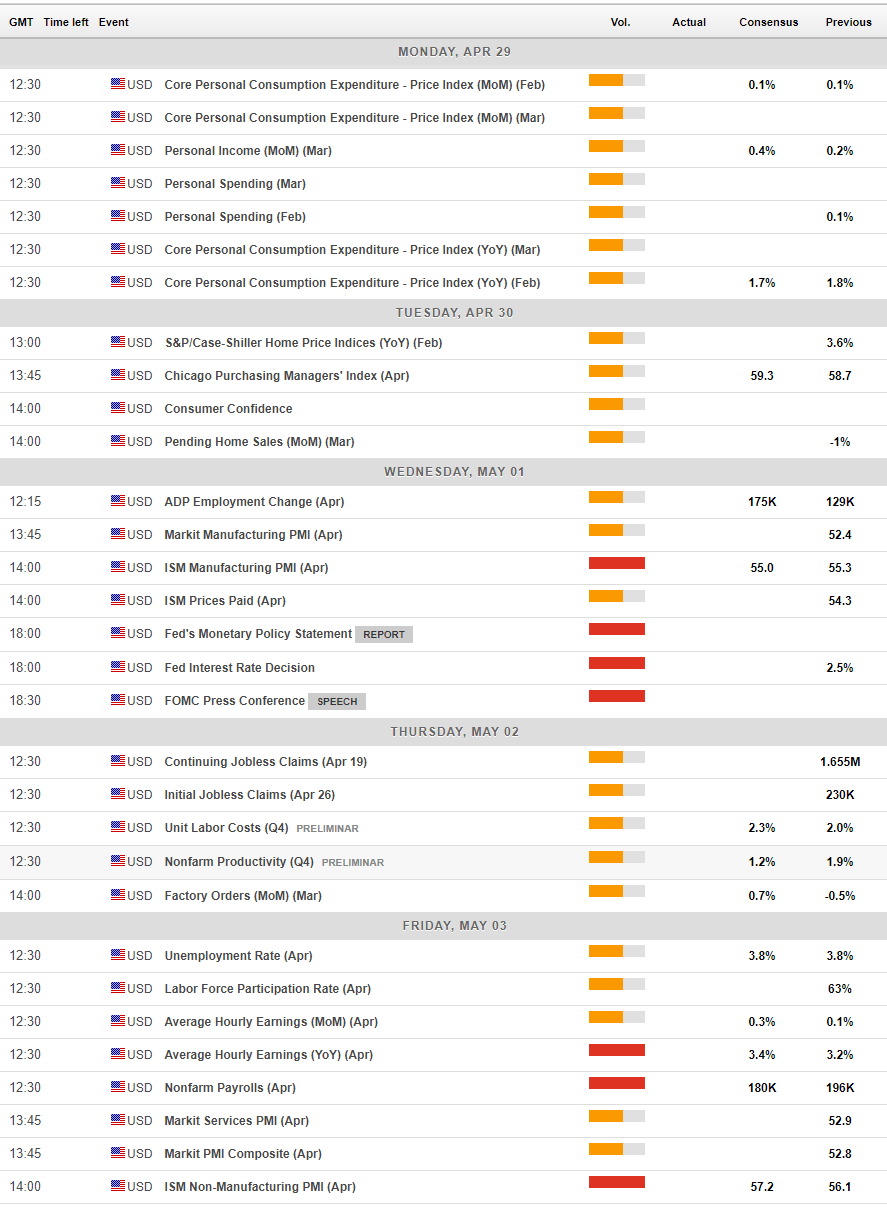

The turn of the month is jam-packed on the calendar. The week kicks off with the Federal Reserve's preferred measure of inflation: the Core PCE Price Index. After the parallel Core CPI dropped to 2% in March, this measure will likely follow suit by edging down from 1.8% to 1.7%. Personal Spending and Personal Income are released at the same time.

Tuesday features two housing figures. The S&P Case Shiller HPI which shows slower growth in prices, and Pending Home Sales. The Conference Board's Consumer Confidence is also on the cards and will likely show OK levels of confidence.

Things genuinely warm up on Wednesday. The ADP Non-Farm Payrolls report for the private sector is not always well-correlated to the official BLS report, but it certainly moves markets. A bounce back to 175K is projected after 129K in February (before revisions).

The second NFP hint is the ISM Manufacturing PMI. The forward-looking survey stood at 55.3 points in March, above the 50-point threshold that separates expansion from contraction, but not at the peak levels seen beforehand. The Prices Paid component is also of interest for the Fed, that uses it as a gauge of inflation.

The US releases Factory orders, productivity data, and jobless claims on Thursday. Everything is of interest, but the focus will likely remain on the Fed fallout.

On Friday, the focus shifts to the US Non-Farm Payrolls. March saw a return to normal with job growth rising by 196K and wage growth decelerating to 3.2% YoY with an increase of only 0.1% MoM. Another satisfactory increase in jobs is projected: 180K. Wages carry expectations for an advance of 0.3% MoM and 3.4% in April, repeating the data for February. The Unemployment Rate is on course to remain at the low level of 3.8%. All in all, economists forecast another positive outcome.

Slightly overshadowed by the NFP, the last word of the week belongs to the ISM Non-Manufacturing PMI. The survey for services stood at 56.1 points in March, slightly above the manufacturing sector number. It is now predicted to rise, reflecting hopes for faster growth.

Here are the top US events as they appear on the forex calendar:

Japan: Watch trade talks and the general mood

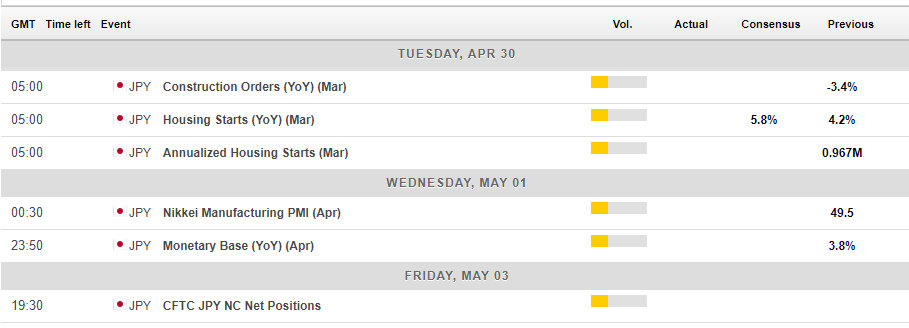

The Japanese calendar is quite empty, with Construction Orders, Housing Starts, and the Manufacturing PMI all being of interest, but will unlikely rock the boat.

The yen will, therefore, focus on the general sentiment in bonds and stocks, driven in no small part by trade talks. The meetings between China's He and America's Lighthizer and Mnuchin will be closely watched. Markets want to see a final deal or at least an announcement on a summit between Presidents Donald Trump and Xi Jinping.

Here are the events lined up in Japan:

USD/JPY Technical Analysis - Bullish

Dollar/yen settled above the 200-day Simple Moving Average and feels comfortable there. Also, the 50-day SMA is getting closer to crossing above the 200-day one, the golden cross pattern. Momentum remains positive, and the Relative Strength Index is stable.

USD/JPY is trading in a narrowing wedge, with uptrend support being steeper than downtrend resistance. The pair is trading in the middle of the range at the time of writing.

Despite the recent slide, the technical picture is positive.

Some resistance awaits at 112.15 that capped the pair in both March and April. The next line to watch is the recent high of 112.40 that was the highest level seen this year. The next levels are 113.60 and 114.20 that date back to late in 2018.

111.35 was the recent low and provides immediate support. It also converges with the 50-day SMA. The next line to watch is 110.85 that was the low point in mid-April. Further down, 109.75 was a swing low in late March. Lower, 108.50 is next down the line,

-636918679445058970.png)

USD/JPY Sentiment

Optimism by the Fed may be positive for the greenback against most currencies but could trigger a downfall in stocks that could, in turn, trigger safe-haven flows towards the Japanese yen. A downbeat Fed could weigh on the dollar against most currencies but also weigh on the yen if stocks rise. All in all, USD/JPY has more room to march forward than fall, but the moves could be limited due to the role of the yen.

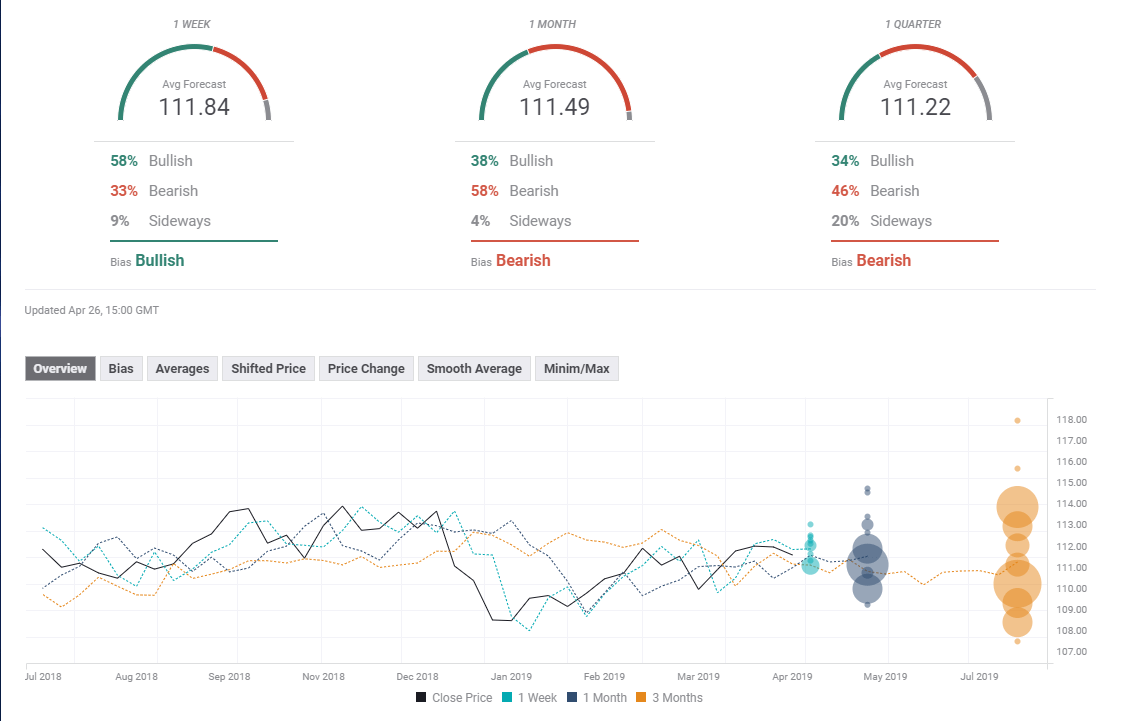

The FXStreet Poll shows a bullish bias in the short term and bearish ones afterward. While the targets are descending, all are between 111.00 and 112.00. In addition, the targets have not changed much. It seems that experts are cautious.

Related Forecasts

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.