US ISM manufacturing PMI December Preview: Waiting for improvement from China trade

- Manufacturing sentiment expected to climb but remain in contraction for the fifth month.

- Business spending was positive in October and November.

- US/China trade deal may help to improve factory outlook.

The Institute for Supply Management (ISM) will issue its purchasing managers’ index (PMI) for the manufacturing sector in December on Friday January 3rd at 15:00 GMT, 10:00 EDT.

Forecast

The purchasing managers’ index is expected to rise to 49.0 in December from 48.1 in November and 48.3 in October. The prices paid index is predicted to rise to 47.5 from 46.7. The new orders index registered 47.2 in November down from 49.1 a month earlier. Employment fell 1.1 points to 46.6 and new export orders dropped to 47.9 in November from 50.4 in October.

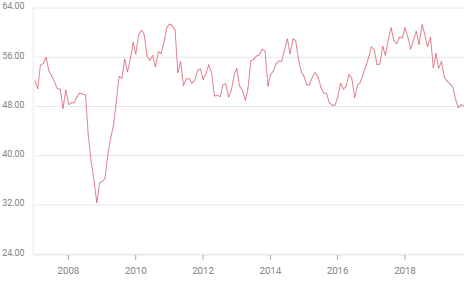

Manufacturing PMI

ISM Manufacturing Report on Business

The ISM survey is sourced to the answers of “a group made up of more than 300 purchasing and supply executives from across the country.” These professionals respond anonymously to a “monthly questionnaire about changes in production, new orders, new export orders, imports, employment, inventories, prices, lead times, and the timeliness of supplier deliveries in their companies comparing the current month to the previous month.”

The responses in the monthly survey are ranked on an index where the division between expansion and contraction is at 50 with the former above and the latter below. *Quotations from the Institute for Supply Management website.

US manufacturing: Unsettling the gloom

Even though the US-China trade agreement has been long anticipated, it is probably too soon to see a substantial improvement in US manufacturing sentiment from the ‘phase one’ trade deal slated to be signed in Washington on January 15th. Though a positive reaction is anticipated as the agreement comes into force the somewhat torturous negotiations over the past two years has instilled a note of caution in the business response.

The purchasing managers’ index in manufacturing slipped steadily lower in 2019. From its 15 year high in August 2018 of 60.8, by last March it was at 55.3 and in August it dropped to 49.1, its first dip into contraction since August 2016. The index dropped to 47.8 the next month the lowest for this survey since July 2009. Recovery to 48.3 in October and another drop to 48.1 in November made four straight recessionary months in manufacturing, equal to the longest stretch since the financial crisis.

Indexes for new orders, export orders and employment have fallen in tandem with the overall sentiment index.

According to the November ISM report, “Global trade remains the most significant cross-industry issue.” Of the 18 manufacturing categories followed by the Institute five reported growth and 13 contraction. All ten component indexes saw falling measures despite the estimate of 2.3% GDP growth in the fourth quarter from the Atlanta Fed.

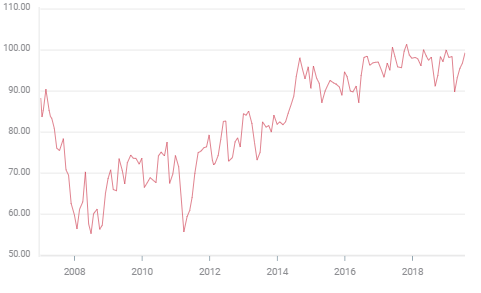

US Consumer Economy

Record employment and strong wage growth has kept the consumer economy humming. Retail sales in the second half of the year reflect the return of consumer sentiment to its best ranges of the past three years.

Michigan Consumer Sentiment

FXStreet

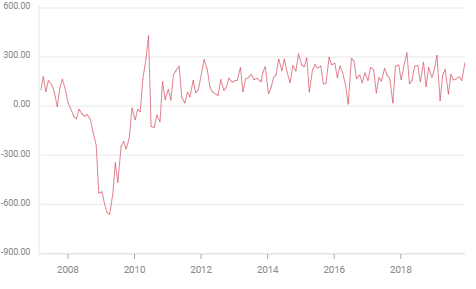

Next Friday’s non-farm payrolls for December are expected to continue the excellent labor market with 172,000 new positions following November’s surprise gain of 266,000. The unemployment rate will remain at a 50 year low of 3.5%.

Non-Farm Payrolls

Conclusion

The US manufacturing sector has been burdened with the China trade war, which, whatever its long-term potential for improved access to the mainland market has exacted a heavy cost in immediate business. The decline in export orders and the threat to global growth from a rampant expansion of tariffs have driven factories into recession and curtailed business investment spending. It has also drastically curtailed US agricultural exports.

Factory performance has limited direct impact on the dollar but the Fed will note carefully if the sector receives a boost from the trade deal. The US-China dispute was cited numerous times by Fed officials as one of the risk factors behind the 0.75% reduction in the fed funds rate from July to October.

Can the limited trade agreement restore the optimism of factory managers, export orders and investment spending to the levels of 2018? Potentially yes, especially if the deal unleashes some of the inhibited growth in the Chinese and American economies, both have demonstrated the capacity to expand faster than their current rates.

December’s PMI figures will reflect past concerns but improvement can be expected before the end of the first quarter.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.