US Initial Jobless Claims Preview: Better is still a long way to go

- Claims predicted to drop to 1.3 million from 1.542 million.

- Continuing claims to fall to 19.8 million from 20.929 million.

- Total claims filed approaching 45 million in three months.

- May retail sales show burst of deferred consumer spending.

- Markets and the dollar remain priced for a rapid recovery.

The slow decline in initial jobless claims in the US is expected to continue but even the lowest number in three months would be almost six times the pre-pandemic average from February.

Labor Market statistics

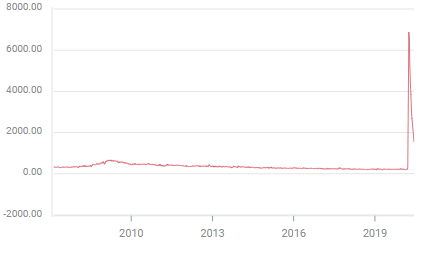

First time unemployment claims are predicted to drop to 1.3 million in the June 12 week from 1.542 million in the first week of the month. Claims will have declined for 11 straight weeks since reaching 6.867 million in the week of March 27, the second of the layoffs forced by the business closures from the coronavirus pandemic.

Initial jobless claims

Though claims will be down 87% from that March peak, the more relevant comparison is between the four week moving averages, 2.002 million in the week of June 5 and 232.5 thousand in the March 13 week, an increase factor of 8.6 or 860%.

Continuing claims are forecast to tumble to 19.8 million in the June 5 week from 20.929 million. It would be the first total below 20 million in six weeks and a 20% drop from the high of 24.912 million on May 8.

Non-farm payrolls figures from May that had 2.5 million hires instead of the expected 8 million layoffs strongly suggests that the bottom for the labor market was with April’s loss of 20.687 million positions.

The June payrolls results will be reported on Thursday July 2 rather than Friday due to the US Independence Day holiday on July 4.

PMI and retail sales

Purchasing managers’ indexes in May from the Institute for Supply Management have also rebounded from their April lows. Manufacturing PMI came in at 43.1 up from 41.5. The new orders index rose to 31.8 from 27.1 and the employment index edged to 32.1 from 27.5.

Services was marginally stronger with overall index rising to 45.4 in May from 41.8 and new orders jumping to 41.9 from 32.9. Employment rose to 31.8 from 30 in April.

Payrolls are normally the last to recover when business conditions improve as firms want to be certain the economy is on the upswing before committing to increasing labor costs.

Retail sales were much better in May than anticipated, reversing their record April losses with their largest increase in history. Overall sales jumped 17.7% after falling 14.7% and the control group GDP component rose 11% following the April 12.4% plunge.

Retail sales

Conclusion and markets

Last month’s retail sales figures may help to speed hiring as cash flow improves to small business, but many of the service sector workers fired in the early days of the business closures are unlikely to return soon as consumer traffic is still a fraction of what it was last year.

The initial claims and non-farm payrolls numbers show that the employment situation is better than it was but it is a long way from normal. People are still losing their jobs as businesses fold under the pressure of the restrictions and the uncertain timeline for complete opening. Hiring has a long road ahead to employ all who have lost their jobs.

Equity markets and the dollar have largely priced a rapid recovery with currencies completing their exit from the risk-aversion trade last week. The variable for both markets is the state of the pandemic and its potential to bring back business closure in some or all of the US. That possible development would mean wholesale market revision.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.