Japanese FX intervention: Primed and ready

With USD/JPY trading above 155, markets are now on high alert for BoJ FX intervention. Having secured a joint press release with US and Korean authorities last week to acknowledge serious concern over yen weakness, Tokyo will now feel it has Washington’s blessing to enter FX markets. We look at when and how Japanese authorities could intervene.

Markets are on high alert

Now that USD/JPY has glided through the 155 level, markets are now on high alert for Japanese FX intervention. Recall that 155 had been the level that many in the Japanese banking community had felt would elicit BoJ FX selling operations. That heightened sense of intervention is reflected in the FX options market, where one week USD/JPY traded volatility is now priced at 14.5%, the highest since last December and the one week risk reversal skew - the price for a USD/JPY put over an equivalent USD/JPY call option - has now widened to 3.4% in favour of USD/JPY puts. These are the widest levels since last July.

Japan will feel it has Washington's blessing to intervene in FX markets. Earlier this week, Japanese Finance Minister, Shunichi Suzuki described last week's US-Japan-Korea press release is a 'milestone' agreement - one in which the serious concerns over the yen and won weakness were acknowledged by Washington.

Remember the objective of Japanese FX intervention now would be to make USD/JPY more of a two-way, rather than one-way bet and be marketed as a stabilisation measure. The question now is at what level might the BoJ sell FX and in what kind of amounts?

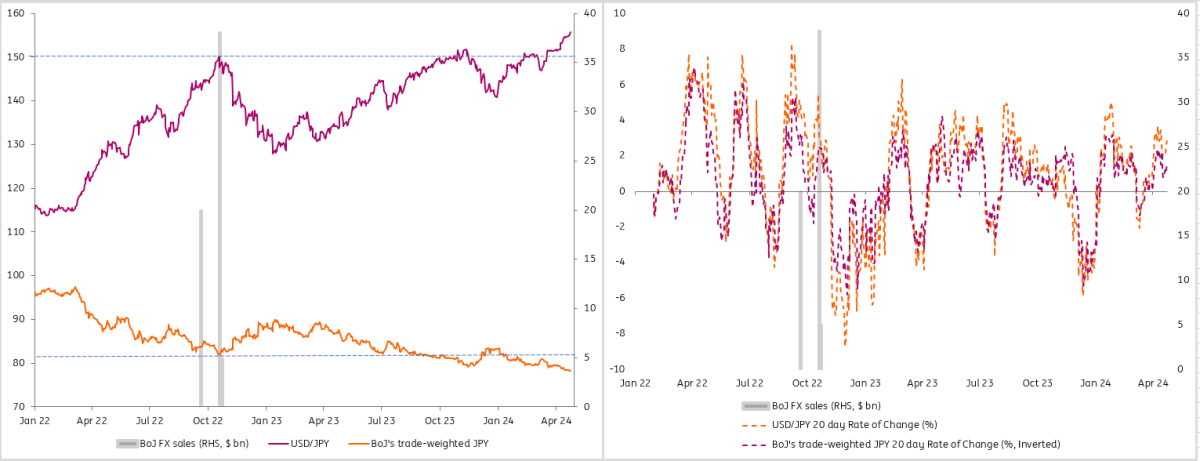

2022 intervention: Absolute levels and rate of change

Source: Refinitiv, ING

The 2022 experience

The BoJ have not intervened much in FX markets over the last decade. Unlike the 1990s and up until around 2003, when intervention was a regular occurrence, episodes of intervention since then have been few and far between. Before the September/October 2022 episode, prior intervention had only been seen in late 2011.

Drilling down into the 2022 FX intervention then, we can see the BoJ entered the market on three separate occasions. Its first foray was September 21st - a Wednesday - when it sold around $20bn. It then followed up around a weekend a month later (Friday 21st, Monday 24th) selling $38bn and $5bn respectively.

The above chart looks at some of the comparables - both in absolute terms and through rates of change. Above we look at both USD/JPY and also the BoJ's trade-weighted nominal yen. In absolute terms, clearly USD/JPY and the TWI have traded through the levels that triggered the 2022 intervention. And looking at rate of change metrics - a measure of disorder or dislocation - today's adjustments of just under 3% over the last 20 days are way under the 5-8% drop in the yen seen back in 2022.

The conclusion to be drawn is that while the market may be on high alert for intervention now (since USD/JPY is above 155) market conditions are not as severe as those seen in 2022. This could suggest USD/JPY needs to be much nearer to 160 before we can expect intervention.

The Yen and the BoJ

In a recent update, ING's economist covering Japan, Min Joo Kang, reminds us that BoJ Governor Kazuo Ueda has made the link between currency weakness and BoJ policy. In other words, if the yen falls too far the BoJ might have to hike rates more. ING's view is that the BoJ hikes 15bp and 25bp in October. However, a surprise March hike from the BoJ did not do the yen much good and it is not clear that an extra 25bp of tightening in JPY swaps curve would make much difference to USD/JPY. For reference, the forward curve still only prices one-month JPY swaps at 0.77% and 0.92% respectively in three and four years' time.

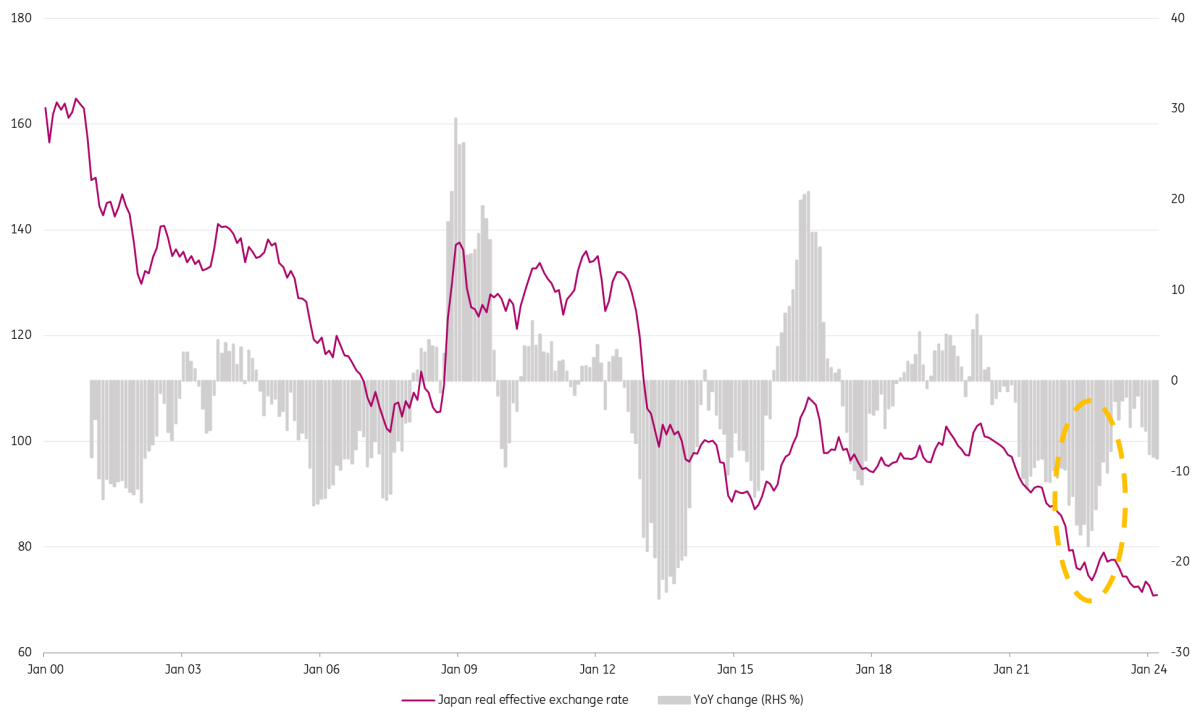

Again comparisons to 2022 may make it a little harder to cite the yen as a key factor in the BoJ's current deliberations. Our chart below shows Japan's real exchange rate and the 20% YoY declines it was suffering around September and October 2022. Currently, those declines are close to a far more modest 8%. And some studies suggest exchange rate pass-through (ERPT) to core CPI is exceptionally weak at just 3% even though ERPT to import prices stands at 65%.

Japan's real exchange rate remains pressured

Source: BIS, ING

Read the original analysis: Japanese FX intervention: Primed and ready

Author

Chris Turner

ING Economic and Financial Analysis

Chris is Head of FX Strategy at ING. Together with his team, he provides short and medium-term FX recommendations for ING’s corporate and institutional client base.