US FOMC July Preview: The advent of yield curve control?

- No change in fed funds rate or pandemic relief programs expected.

- Officials have hinted that may move to target longer term rates.

- ‘Yield curve control’ may entail caps or targets for long term rates.

- Unemployment claims have stalled at 1.3 million, consumer sentiment has reversed.

- The darkening economic picture in the US is one factor behind the dollar’s fall.

The Federal Reserve’s fifth meeting in the pandemic economy is not expected to change the bank’s fed funds interest rate or policy and program approach to the economic debacle brought on by the Covid virus.

After two emergency meeting in March that produced a zero fed funds rate and more than two trillion in securities purchases and loan guarantees, the Federal Reserve Open Market committee, the policy body of the bank, has kept it approach intact since while promising to do all it could to ensure that the US economy recovers from its most rapid collapse in history.

Fed Funds

Yield curve control

One possibility is that the FOMC will add the targeting of long term rates to the largely short-term impact of its traditional fed funds operation.

Called ‘yield curve control’ it would set a cap or target for one or several specific long term rates, and buy or sell Treasuries to move the market yield to the desired return. The Fed’s quantitative easing programs operated in the same fashion, buying government and commercial bonds to force rates lower. Current 30-year mortgage rates that are the lowest in history are one result of the program started by the central bank in March to mitigate the effects of the pandemic.

The primary difference between the yield control concept—there is no acronym yet—and QE is that the YCC? YC2? YC², publicly targets a specific rate much as the Fed’s core inflation target is 2%.

Powell on the economy

In Congressional testimony Chairman Jerome Powell has stressed that while the recovery started sooner than the governors expected, its path was highly uncertain and would “depend in large part on our success in containing the virus.”

Mr. Powell’s warning was prescient. A flare-up Covid infections in several Western and Southern states has reversed some of the reopening measures, delayed others and threatens to send the economy back into a job loss tailspin.

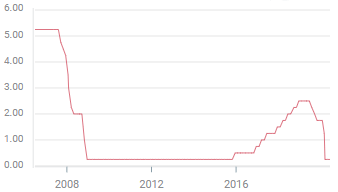

Initial jobless claims and non-farm payrolls

Claims for unemployment benefits have been over 1.3 million for 18 weeks. Despite the 80% decline from 6.867 million in the March 27 week to 1.413 million three months later on June 26, progress since then has been non-existent. The small, 7.5% drop to 1.307 in the July 10 week reversed to 1.416 million the following week. In that month an additional 5.446 million have been fired or furloughed and sought jobless benefits.

Initial jobless claims

The combined March and April job losses of 22.16 million has been one-third recovered by the 7.499 million hires in May and June. But the stalled unemployment claims numbers have stirred speculation that the July non- farm payrolls figure due on Friday August 7 will be flat or even negative.

Consumer confidence

The two months of improvement from the April to June in the Michigan consumer sentiment score have reversed. The July preliminary fell to 73.2 reading from 78.1 in June. The pandemic low as 71.8 in April.

Confidence from the Conference Board is expected to drop to 94.5 this month from 98.1 in June. The plunge from 132.6 in February to April’s 85.7 was the largest decline in the 53 year series.

Conclusion and the dollar

After the Fed’s extraordinary rate, QE and loan programs in March one common question was what could the bank do if, despite these interventions, the economy continued to fall. As Mr. Powell has noted, recovery depends largely on non-economic factors, on the course of the pandemic.

It seems that the answer is yield curve control. Former Chairs Janet Yellen and Ben Bernanke have said the bank may need to cap Treasury yields as a way to help the economy. Current FOMC members Richard Clarida and Lael Brainard also think it should be given consideration and Chairman Powell has said he is open to the idea.

It seems perhaps unlikely that the Fed would take such a major policy step without giving the markets time to adjust to the concept and its ramifications. But the Fed demonstrated in March that it is not afraid of drastic action.

The economy appears to be slowing from the combined effect of new restraints and consumer pullbacks, but the Covid outbreaks that have prompted the retreat also seem to be peaking.

The dollar’s sharp decline in the last two is directly linked to the potential Covid impact on the nascent recovery in the United States and the possibility that the Fed will move again on rates.

In the end the Fed will probably wait to see where the economy heads before instituting yet another ground-breaking policy and use the time to acquaint the markets with its latest prescription.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.