The full impact of rate hikes has not come through yet

Outlook

Yesterday Richmond Fed Barkin spoke out of both sides of his mouth. Inflation should moderate and the labor market is now helping “But he cautioned that there still is risk that continued housing and services inflation will keep price gains elevated. Sellers are still trying to raise prices, he warned, and they will do so until customers push back strongly. ‘The risk is that, as we get less help from the goods sector, continued shelter and services inflation will leave the overall index higher than our target,’ Barkin said.”

Nothing new or even interesting here except for one thing—he acknowledges Lag. The full impact of rate hikes has not come through yet. When that happens, we will get inflation closer to the target.

In retrospect, it’s puzzling that more Feds, including Mr. Powell, do not emphasize Lag as a critical factor. It might not make any difference to the high-frequency traders, but it’s the dose of realism we solely need to tamp down high emotions (“high inflation! Probably means hikes!”)

New York Fed Williams underlined the message with this: "Eventually we'll have rate cuts" but for now monetary policy is in a "very good place." In other words, it’s bringing down the inflationary factors. Later today we get the former dove, Minneapolis Fed Kashkari.

We like Mr. Powell for his Boy Scout earnestness, but gee, he could have put it like this. And the bond market was pleased. The 2-year yield that had been a hair over 5% is now down to 4.835%. See the little dots showing where this stands on the 52-week basis.

Not a tidbit but a bit off on the side are the oil and gold prices, plus the equity indices. Oil and gold are imagined to be inversely correlated with the dollar—dollar down, gold up. This (and oil) is an unreliable relationship and not to be swallowed whole. The same thing holds for the dollar and the S&P. This time some analysts are confused by less than stellar earnings failing to drive equities down, which shows a lack of understanding of sentiment, of which earnings is but a small part.

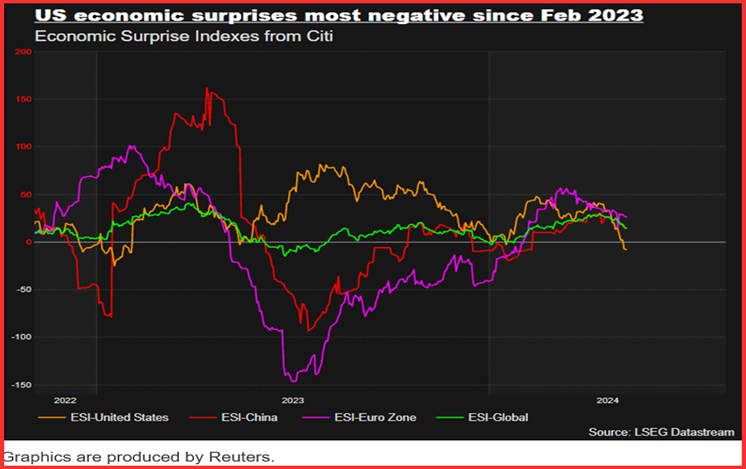

We don’t like to forecast the stock market but something else has come to the top of the commentary pile—the Citi surprise index. Everyone is showing it today. Below is the Reuters version. We guess the drop in surprises/shocks in relation to expectations is thoroughly equity index-positive. And yes, we can have the dollar and the S&P up at the same time.

Forecast: The Tuesday pullback is quite feeble so far and is visible mostly in the USD/CHF and maybe the USD/JPY, although yesterday’s holiday and intervention story make it hard to tell. The max move in the euro would be to about 1.0675, hand-drawn support. We never know when a corrective pullback will end, so beware. It could be small and short-lived or it could be big and long-lasting.

Intervention Saga: Nobody knows for sure whether the BoJ intervened last week.

Reuters reports “Japan's top currency diplomat Masato Kanda once again on Tuesday said Japan may have to take action against any disorderly, speculative-driven foreign exchange moves.”

TreasSec Yellen added no clarity by saying "I'm not going to comment on whether they did or didn't intervene. I think that's a rumor." She also said the yen "did move quite a bit in a relatively short period of time" and “we would expect these interventions to be rare and consultation to take place." The inference is that no consultation did take place, hence “it’s a rumor.”

Was Yellen being subtle and diplomatic? Some think she was sending the message that “they should have told us” and “next time, please let us know” but intervention should be very, very rare. In other words, if you are going to do it again, consult with us—as though the US has the authority to approve or disapprove. This seems arrogant and insulting, although it’s in keeping with various formal agreements. We may never find out, or find out months or years down the road.

The question is whether yen traders interpret any of this as giving permission to push the dollar/yen up even further, back toward 160. If volatility is falling, and volatility is the justification for intervention, the MoF/BoJ are in a pickle.

Ordinary chart-reading would have any bounce in dollar/yen ends somewhere around 156. But this is hardly an ordinary environment.

It’s a little funny that former TreasSec Summers said that interventions are ineffective at shifting exchange rates. This is, historically, questionable. If he was thinking of the big currency deals of the 1970’s and 1980’s, he is both right and wrong. As former Fed chief Volcker wrote in his book Changing Fortunes, the first big intervention was the Plaza Accord, which worked so well it had to be reversed by the Louvre Accord. We have had interventions, mostly by the BoJ but also by others (Bank of England, China) and some worked, while others did not.

Some analysts expect yen volatility to wind down and remove the official justification for intervention. As a side note, if there is a goal, we guess that the classic 50% retracement might be it. That falls, conveniently, at about 150. Now we have to consider whether market sentiment will adapt to what the MoF/BoJ seem to want, nourished at least a little by the prospect of the rate differential narrowing from the US side. We would not bet against it.

Reasons for the Fed to Cut Rates:

Avoid embarrassment from getting inflation wrong twice.

Normalize the yield curve.

Head off any recessionary tendencies.

Help housing via mortgage rates.

Help banks rollover commercial property loans.

Help the stock market.

(Help the current White House) .

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat