The Fed is getting its way on 'Yes, March'

Outlook:

We are still reeling from the change in sentiment toward the March rate hike. The Fed has a terrible time herding cats, aka the bond market, but managed it this time. Bloomberg reports "Options traders scrambling to price in a March increase exchanged a record volume of Fed futures contracts yesterday." Analysts think Yellen's speech on Friday will be a tipping point. We say the tipping point already arrived when Fed funds futures took the probability well over 50%. Besides, it's always unwise to count on the Fed being clear. Remember Greenspan's "If you understood me, I must have misspoken."

We wished for a comment from Greenspan on the Fed herding sentiment toward March, but all we got in a BBC News interview last evening was his opinion that Trump's America First stance is like Latin American populism—something born of "pain and desperation." His words. And like most populist movements that promise both higher spending and lower taxes, it doesn't have a snowballs's chance in hell of working.

Proof that the Fed is getting its way on "Yes, March" comes from the 2-year yield, which rose to 1.30% intraday yesterday, the highest since 2009. The 2-10 year spread is down to 116 bp, from 136 bp in December, according to the FT. "The move is notable given the fact T-bills have remained subdued due to concerns over the upcoming debt ceiling deadline in March, despite longer-dated yields rising off the back of higher growth and inflation expectations."

It's not all a bed of roses, though. Yes, yesterday's PCE inflation met expectations of near 2%, backstopping the March hike, but the GDP numbers are discouraging. The last Q4 GDP was 1.9% and yesterday's Atlanta Fed Q1 forecast is 1.8%. You can get inflation without much growth—it used to be called stagflation, or worse, secular stagnation--but growth-fueled inflation is the happier version and indicates a more sustainable path of rate hikes.

The Fed prefers core inflation numbers over all others, meaning it declines to forecast prices for food and energy. And yet energy prices are a key driver of more general inflation and we neglect it at our peril. Consider that over the past year, oil prices are up 50%. This is nice for US producers (and exporters). The WSJ notes that the US is a "free rider" on the OPEC output curb, and benefiting from European demand for light sweet crude (while the US Gulf refineries are equipped for heavy and sour). The forecast for oil prices is central to any decent forecast for inflation.

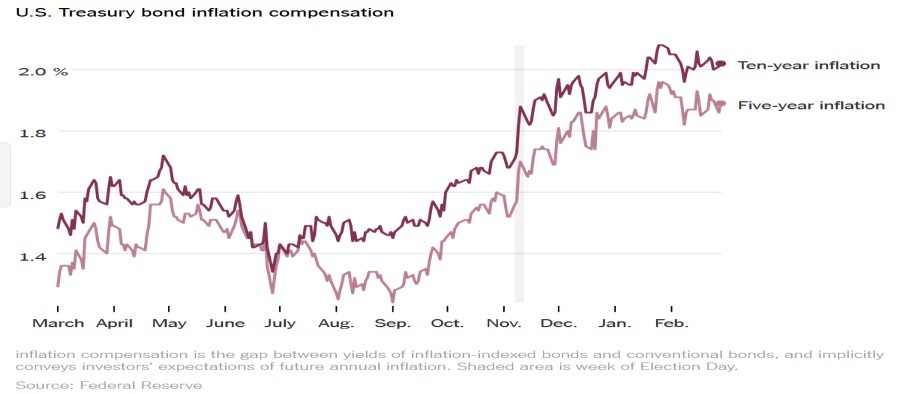

And yet inflation forecasts, as embodied in the TIPs-notional spread, is seeming independent of oil price forecasts or anything else truly "fundamental." See the Fed chart below from the NYT. Inflation forecasts are high and rising because of unproven expectations of unstated policy changes plus a dollop of "normalization." We may complain that QE distorted everything and the Fed's giant balance sheet will continue to distort for years to come, and nobody denies that QE makes a hash of allocations. Nobody can say for sure whether the new rise in inflation expectations is due to normalization, actual and expected oil prices rises, or assumptions about Trump policies.

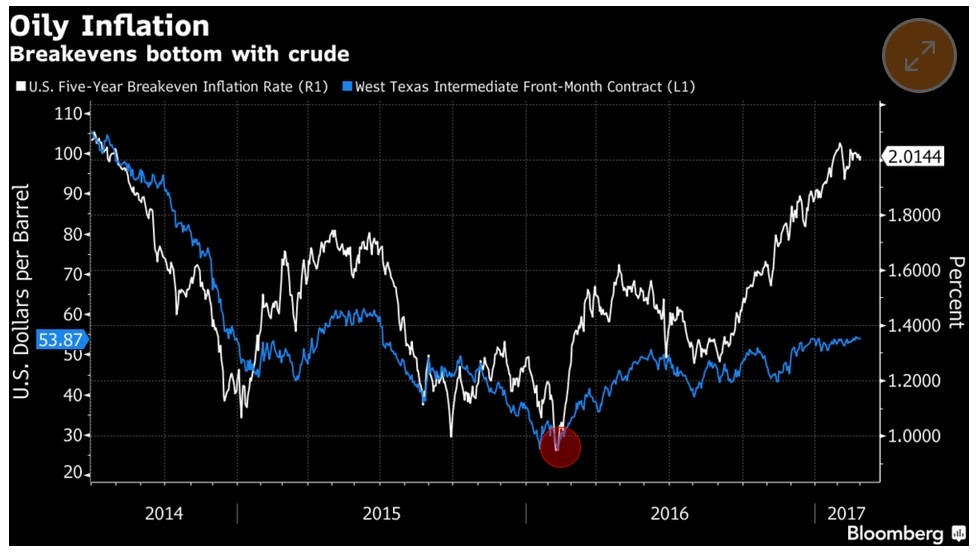

Bloomberg asserts that rising inflation expectations are chiefly an oil story. Trump may try to claim credit for the surging equity markets, but the reflation trade was in place long before the election and based on oil price rises. This is the removal of "the drag on inflation from the price of crude, which a year ago was plumbing depths last seen in 2003." We especially like the chart below:

How to weight these three factors? The oil/breakeven chart is quite convincing. But did the Fed determine to promote "Yes, March" because it sees true, genuine, real inflation ahead from Trump policies? And if so, what does the Fed know that the rest of us do not? After all, there is hardly anything concrete on the table. The one thing we think we know is that Trump policies, unless shaved down by Congress, are going to raise deficits and the national debt without providing the tax revenue offset. So, Feds can speak of robust employment and a good growth trajectory, but markets are right to suspect they have some lines of thought they are not disclosing.

In contrast, we think we know what the ECB is thinking—that headline inflation may hit 2% but the underlying core inflation remains moribund at 0.9% and thus not inspiration for ending QE. But the Germans will continue to agitate. Reuters reports "Keeping inflation-wary Germans patient may be the ECB's biggest challenge as the politically sensitive and emotionally charged issue is bound to feature in the election campaign ahead of elections in September.

"With German inflation at 2.2 percent, real rates are in negative territory, eating into the savings of thrifty households and adding to already abundant criticism of super easy monetary policies.... With overall savings of 5 trillion euros ($5.28 trillion) and interest rates at zero, an inflation of 2 percent means German savers are basically losing 100 billion euros per year, Bavarian Finance Minister Markus Soeder said on Wednesday. Policymakers earlier suggested that any discussion about the bank's next step would likely start in June with a decision coming only after the summer."

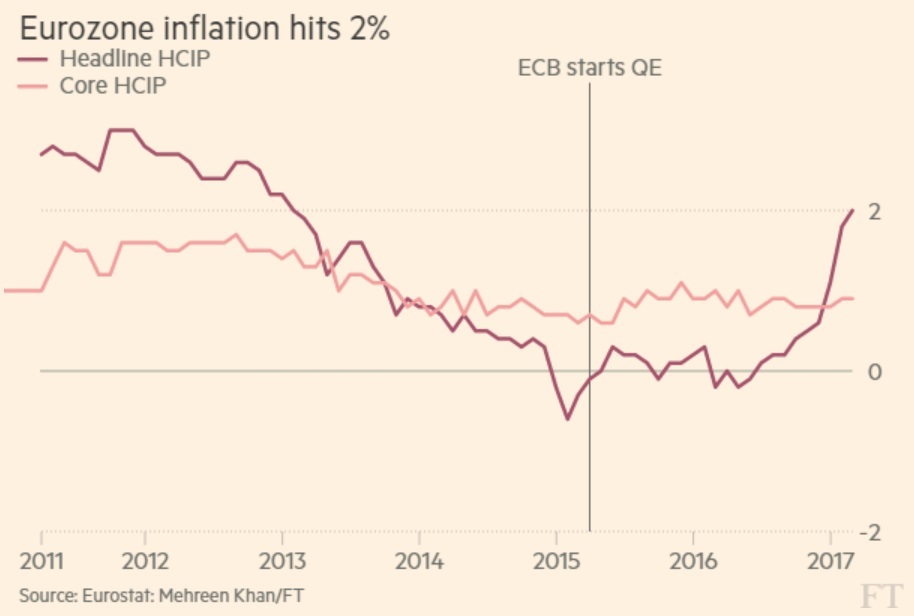

Technically, the ECB target is "below 2%" so the 2% number today means the ECB is under pressure to act from lots of corners, and not just the German one. The FT calls it a headache for Draghi, but he's a strong guy and can let inflation run above target for some time to compensate for years of deflation. Besides, inflation rates are wildly uneven among members. Spain has 3.1% but Ireland has 1% and France, 1.4%. We like the FT chart placing QE at the dividing line between deflation and inflation. We'd really like to see some other data on this chart, like oil prices. The ECB next meets on March 9.

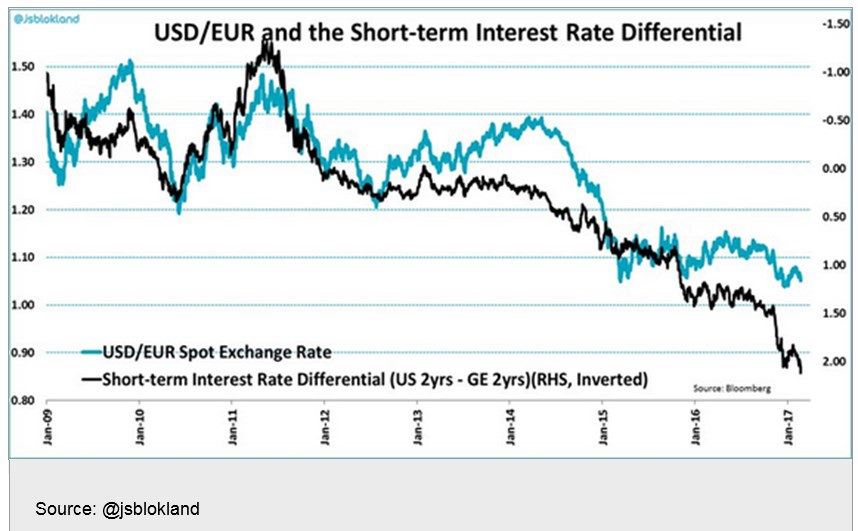

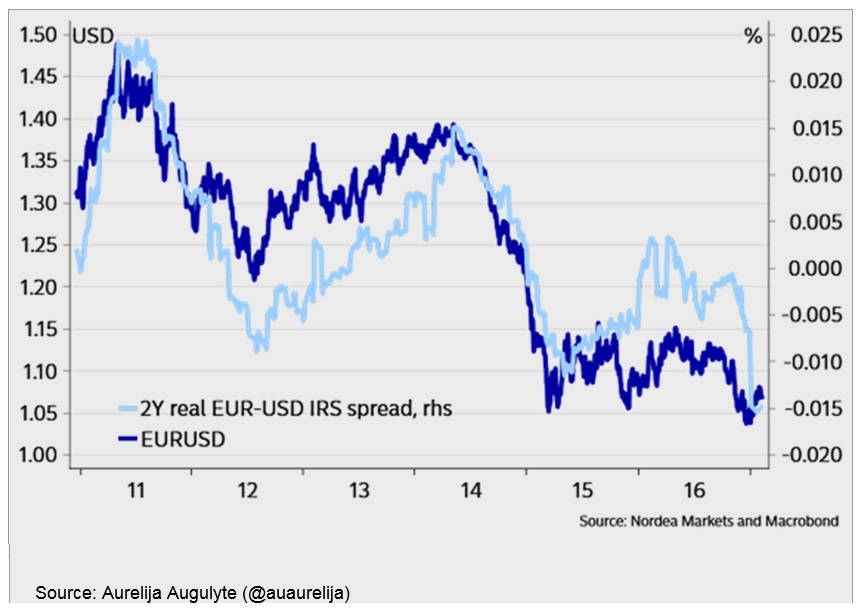

But as always, it's not only the rate response that counts, it's the differential against others. The Daily Shot has two charts, the first showing the 2-year spread vs. the euro and the second showing the "real" rates, which looks less compelling. That's not the message we get. On the first chart, raw notional yield diff, the dollar was overly strong given the spread from mid-2012 to Jan 2015. This is probably risk aversion plus unjustified expectations of a more activist Fed.

Then, in the real version, the euro is overly weak given the spread during most of 2015 and this is the ECB's embrace of QE. In other words, sentiment and institutional expectations skewed the relation-ship. But the correlation is still darn good, if a little rougher than theory might have it.

The other yield spread that should have traders betting the ranch is the US-Japan. Today FinMin Aso reminded everyone, in case they missed it, that wider US-Japan interest rate differential would cause dollar/yen to rise further. This idea has been on the table for a long time but doesn't always rule. Now it probably will drive the dollar/yen to 120 or more, and remember, the best intermarket correlation of them all is the weak yen/strong Nikkei stock index.

Bottom line, the dollar rally forecast has a good tailwind. Oil prices are jumpy but likely to rise to the $60 level at some point this year. The Fed is hiking in March while the ECB will stay with QE into the fall. And Trump policies, when we finally get any, are probably inflationary.

Politics: After one of two days without an uproar, now we have the Trump candidate for Attor-ney General, Sessions, having failed to disclose meetings with Russians. This is the same old Wa-tergate thing—it's not the event itself, it's the cover-up. The slimy Dem leader Pelosi is calling for Sessions' withdrawal. The NYT is in a feeding frenzy over the former Obama administration intelligence officials having distributed information about the Trump campaign and Russians very widely in case the Trumpies tried to hide it once in office. The NYT thinks this is patriotic, but we worry about spooks having deep agendas. So far this stuff is not affecting the FX market but it's vaguely dollar-negative.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 114.21 | LONG USD | 03/02/17 | NEW*WEAK | 114.21 | 0.00% |

| GBP/USD | 1.2278 | SHORT GBP | 03/02/17 | NEW*STRONG | 1.2278 | 0.00% |

| EUR/USD | 1.0529 | SHORT EURO | 02/10/17 | WEAK | 1.0643 | 1.07% |

| EUR/JPY | 120.25 | SHORT EURO | 02/03/17 | WEAK | 121.56 | 1.08% |

| EUR/GBP | 0.8575 | LONG EURO | 03/02/17 | NEW*WEAK | 0.8575 | 0.00% |

| USD/CHF | 1.0106 | LONG USD | 02/10/17 | STRONG | 1.0024 | 0.82% |

| USD/CAD | 1.3366 | LONG USD | 02/22/17 | STRONG | 1.3174 | 1.46% |

| NZD/USD | 0.7106 | SHORT NZD | 02/10/17 | STRONG | 0.7185 | 1.10% |

| AUD/USD | 0.7618 | LONG AUD | 01/05/17 | WEAK | 0.7343 | 3.75% |

| AUD/JPY | 87.01 | LONG AUD | 02/09/17 | WEAK | 85.92 | 1.27% |

| USD/MXN | 19.9017 | SHORT USD | 01/31/17 | WEAK | 20.8108 | 4.37% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat