The euro looks like a safe haven in a storm

Outlook:

The euro looks like a safe haven in a storm, even though linchpin Germany doesn't have a government yet, in the face of awful dysfunction in the US and UK. We might add Ja-pan, although the upcoming election is not likely to upset any apple carts (Japanese elections tend to be a non-event in financial markets).

In the US, one-man negative sentiment-maker Trump was disclosed as having wanted to increase US nuclear capability tenfold, not knowing that the US had been the leader in reducing global nuclear ca-pability for decades. Hence the Secretary of State's "moron" comment. Yesterday Trump responded to the nuclear ignorance disclosure by threatening to take away a major network broadcast license, anoth-er sign of ignorance (about the First Amendment). Chief of staff Kelly is exhausted trying to keep Trump in check and may not stay in the job much longer. White House staffers leak that Trump is "unstable." Talk of invoking the 25th Amendment is on the rise (a majority of the cabinet can remove the president if he is deemed unfit). Former advisor Bannon is reported to have said there is only a 30% probability Trump finishes his term.

Trump's ignorance also emerged when someone finally pointed out to him that disallowing deduction of state and local taxes would raise the federal tax by almost a third on folks earning $50-150,000/year. Now he is re-thinking that initiative.

In the UK, the Brexit work is one step forward and two steps back. Bloomberg reports October was when the housekeeping was supposed to be done on things like budget payments, allowing trade rela-tions to get started. "Instead, with less than 18 months to until Britain tumbles out of the EU, deal or no deal, the two sides are still battling over what was meant to be the easy part, and the U.K. government is still battling itself on how to approach talks." Case in point: Chancellor Hammond said he will start spending money on no-deal planning in January. Some want him to start now. [European] "Leaders at a summit next week will almost certainly say not enough progress has been made to move on to trade talks, the official said. December is now the next possible date to reach that milestone, leaving the U.K. with less than a year to sketch out a future relationship with its most important trading partner." Mean-while, Germany favors letting UK banks have "transitional access" to the EU. Probably not enough to save Brexit but a good thing.

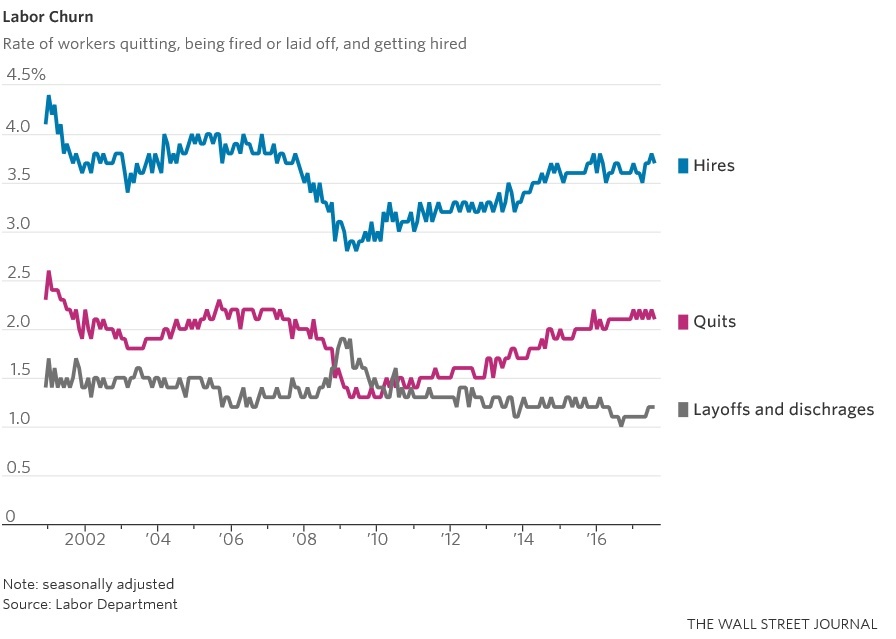

We continue to fret and fume that US growth and inflation are going to fall short of the global averages because there is something deeply, structurally wrong with the US employment environment. Yester-day the JOLTs report (Job Openings and Labor Turnover Survey) shows that workers are not dumping jobs voluntarily to take better ones at an increasing pace, something you would expect given an unem-ployment rate at a 16-year low and the highest level of available jobs at the highest since 2000 when records began. The rate of job leavings actually fell in Aug to 2.1% from 2.2% in July, but is roughly steady over the past two years. See the chart.

The WSJ writes "The quits rate is trending at levels recorded before the recession began, but below 2001 rates. That could suggest that years of steady hiring and labor shortages reported in several indus-tries have not yet made workers feel as if they're likely to find something better if they leave their cur-rent jobs.

The unwillingness to quit could be a factor holding back better wage growth, reflecting workers' rela-tive lack of bargaining power. It might also suggest other factors—such as the unwillingness to move for work, or satisfaction with work-life balance—is keeping workers in their jobs despite ample oppor-tunities elsewhere."

The WSJ is on to something with the new lack of labor market mobility (unwillingness to move for work), a classic advantage of the US labor market and famously something the eurozone lacks, not least because of unions and languages. In the US, unwillingness to move is directly linked to so many houses still being under water. And people's houses are their chief savings vehicle. Selling a house at a loss and not being able to afford a new one elsewhere is a Very Big Deal. It's emotionally upsetting. It brings fury and despair in equal measure.

And therein lies the insight about how and why Trump was able to come even close to being elected. He named people to blame—the Establishment, big banks, the Washington swamp—and promised to fix it. Hidden in his campaign promises was the implicit promise to make your house worth more so you can sell it and not become destitute.

Sentiment is a tricky thing to nail down. The US has one Big Favorable—the Fed rate hike and tapering QE—but it's damaged by doubts about wages and inflation, plus the issue of who takes over from Yellen and whether Trump will try to take away Fed independence. A damaged factor is a weak one.

Then there are the outright negatives, wage growth still failing and the jobs market a mess, reflecting gloom and doom among the citizens. And finally, doom and gloom, not to mention a growing sense of outright fear, about the unfitness of the president.

Now compare to the eurozone, with more robust growth, strong unions that suggest wage growth will continue to match overall economic growth, and an okay political environment, Catalonia nothwith-standing. At least the scariest of the far right is suppressed, for the moment. And the eminently sane Mr. Draghi is going to start talking about tapering sometime. It's not just the outright differential that counts. It's also the rate of change. The US is stalled and the eurozone is just getting started. And the eurozone is likely to deliver a more stable and coherent economic picture, whereas you never really know what to expect from US data, especially now that we have disruptions from hurricanes and fire-storms and ... Trump.

The euro push-back against the correction is a centipede—it has many legs. Having said that, we never know how patient euro bulls will be. A pullback in the euro rally can go quite far, even to the last inter-mediate low at 1.1794, before euro buyers punish the doubters. They will get some ammunition in the form of US data, including PPI today and CPI tomorrow (along with retail sales). The euro rally may appear to be ending and the euro downmove resuming... don't be fooled. See the daily chart. The last low falls just short of the one before (red line). The euro's long-standing rally is dented but not broken.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 112.40 | LONG USD | 09/13/17 | WEAK | 110.05 | 2.14% |

| GBP/USD | 1.3223 | SHORT GBP | 10/03/17 | WEAK | 1.3247 | 0.18% |

| EUR/USD | 1.1854 | SHORT EURO | 09/27/17 | WEAK | 1.1741 | -0.96% |

| EUR/JPY | 133.23 | LONG EURO | 09/13/17 | STRONG | 131.76 | 1.12% |

| EUR/GBP | 0.8964 | SHORT EURO | 09/13/17 | WEAK | 0.9033 | 0.76% |

| USD/CHF | 0.9746 | LONG USD | 09/25/17 | WEAK | 0.9732 | 0.14% |

| USD/CAD | 1.2469 | LONG USD | 09/27/17 | WEAK | 1.2389 | 0.65% |

| NZD/USD | 0.7118 | SHORT NZD | 10/06/17 | STRONG | 0.7088 | -0.42% |

| AUD/USD | 0.7821 | SHORT AUD | 09/25/17 | WEAK | 0.7963 | 1.78% |

| AUD/JPY | 87.91 | SHORT AUD | 10/11/17 | WEAK | 87.35 | -0.64% |

| USD/MXN | 18.7173 | LONG USD | 09/22/17 | STRONG | 17.8066 | 5.11% |

| USD/BRL | 3.1711 | LONG USD | 09/27/17 | WEAK | 3.1670 | 0.13% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat