Nonfarm Payrolls preview: And here comes another soft report

It ´s that time of the month again, when the US releases what once was the biggest market mover. The US monthly employment report, however, has stopped being THE market mover long ago, as a result of the 2008 crisis that led to deflation and record lows rates worldwide. Central banks' decision have been stealing the show ever since, slowly at the beginning, but now being the only possible market trigger that can change a certain trend. In fact, headlines jobs' creation, despite still relevant, has been lately taking a step back in benefit of wages, precisely because these lasts are related to inflation, and central banks these days base their decisions pretty much exclusively on it.

Until last week, the market knew that the US Federal Reserve was on its own in the tightening path, followed by the BOC, as Governor Poloz hinted that the end of lower rates is near. There was some speculation also that rising inflation in the UK, amid Brexit jitters, would force the BOE to act sooner than expected. But things changed 180 degrees at the end of June and during the ECB Forum on central banking, as all of a sudden, most major economies seem ready to follow the Fed's lead. It was not exactly like that, but that's what the market senses after the forum, and sometimes market does not have much logic.

Adding to that, soft inflation in the US during the last few months have generated doubts on Fed's projection for additional hikes. And now, we had a poor ADP survey, and rising unemployment claims at the end of the June. In May, monthly data anticipated a strong payroll, and we got a poor one, as the economy added just 138,000 new jobs, compared to 211,000 in April. What are the odds then of a strong NFP report then for June?

From averaging 240K a month by the end of 2015 and the beginning of 2016, the US job's creation has averaged 121,000 per month over the last three months. Still, and with the economy near full-employment, at least as how the Fed's sees it, is not worrisome. For June, the US economy is expected to have added 179K new jobs in June, whilst the unemployment rate is expected to have remained unchanged at 4.3%. Wages are seen little changed in the month, up to 0.3% from previous 0.2% monthly basis, and 2.6% from previous 2.5% when compared to a year earlier. Over the year, average hourly earnings have risen by 63 cents, far from enough to boost consumption.

Anyway, if the headlines come in-line with expectations, focus will turn to wages, but they would need to surprise big to the upside to back a dollar's rally. If the headlines miss, dollar has no chances.

EUR/USD levels to watch

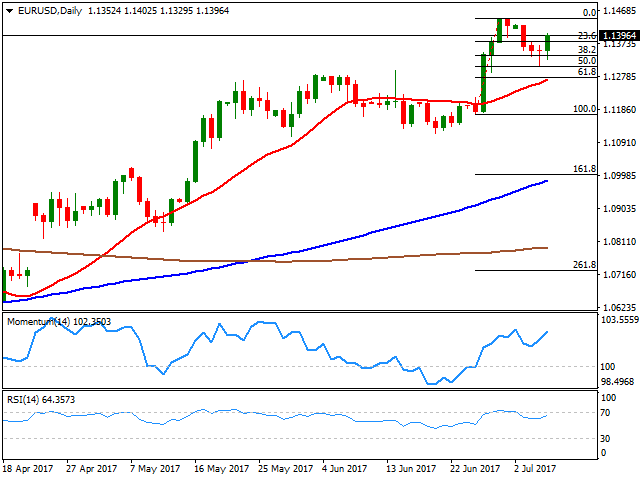

The EUR/USD pair has corrected partially lower this week, but seems now ready to regain the upside, holding near the 1.1400 figure ahead of the report, and not far from its yearly high of 1.1445. In the daily chart, technical indicators have resumed their advances after modestly correcting extreme overbought readings whilst the price is far above bullish moving averages, indicating that the upside is still favored despite this early week's retracement. The pair has an immediate resistance at 1.1420, but a stronger one at 1.1460, as the level capped the upside, since January 2015, with short-lived spikes beyond it being quickly reverted. Nevertheless, and extension beyond it could see the pair advancing up to 1.1494, the high set on November 2015, followed then by the 1.1520/30 region. There's an immediate support at 1.1340, with a more relevant one at 1.1290, June 28th low. Only below this last the greenback will be able to advance further, still in corrective mode, with 1.1250 and 1.1210 as the next supports.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.