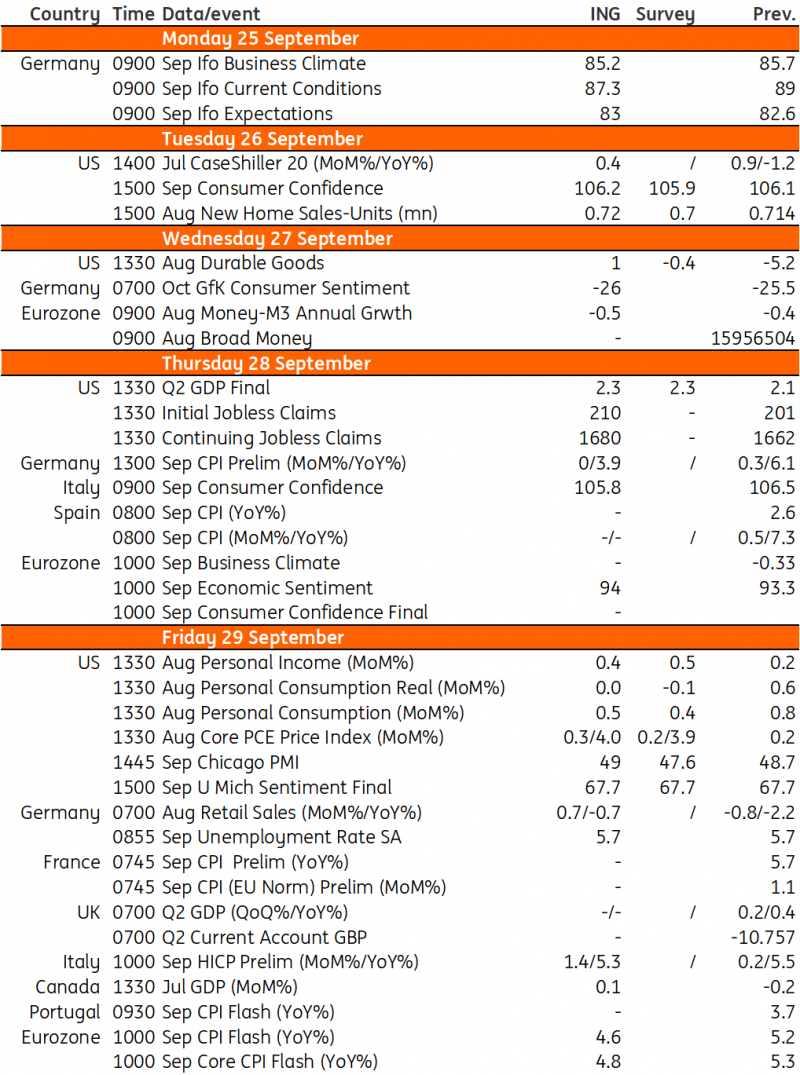

Key events in developed markets next week

Next week, all eyes will be on Federal Reserve officials as they explain what they need to see in order to hike rates again this year. It's also a big week in the eurozone with the release of both headline and core inflation.

US: August personal income and spending report release

The Fed’s higher-for-longer interest rate message, combined with upgraded growth forecasts and lowered unemployment projections, has gained more market traction with the 10Y Treasury yield up at 4.5% – the highest since 2007 – and the dollar continuing to strengthen.

The coming week will see several Fed officials hitting the airwaves to explain their thinking and what they need to see in order to justify hiking rates again this year and what they see as the most likely scenario for next year. At the moment, the market is split on whether there will be a final hike and it will be down to the data and general newsflow to determine what will happen at the November and December FOMC meetings. Jobs, consumer spending and inflation will be the key figures to watch while strike action in the auto sector and the prospect of a government shutdown will also factor into the thinking of officials.

The key release to watch will be Friday’s August personal income and spending report. After a strong July, we expect to see weaker spending coming through, especially in real terms, with higher gasoline prices responsible for much of the increase in nominal spending on goods, based on what we saw in the retail sales report. With regard to services, the Federal Reserve Beige Book indicated that “consumer spending on tourism was stronger than expected, surging during what most contacts considered the last stage of pent-up demand for leisure travel from the pandemic era”. This should help to mitigate some of the weakness in goods, hence our slightly above-consensus forecasts.

We are also aware that the Fed’s favoured measure of inflation, the core PCE deflator, could come in a little higher than the market is forecasting. We look for a 0.3% month-on-month increase in prices, similar to the CPI report, whereas the consensus is for a more benign 0.2%MoM print.

We will also get durable goods orders, new home sales and consumer confidence readings. Again we expect to see slightly higher numbers than the market is pricing, with a lack of available existing homes supporting new home transactions while better numbers from Boeing should help lift orders. The Conference Board measure of consumer confidence is more influenced by labour market responses, which should be good given low unemployment and a strong sense of job security. The University of Michigan measure, which is more reflective of concerns about the cost of living, is consequently likely to be a lot weaker.

Eurozone: Expect a drop in both headline and core inflation

Next week will be all about eurozone inflation. After this week's PMI, which confirmed that the eurozone remains in a weak economic environment, the focus will shift towards inflation progress. Expect a drop both in headline and core on the back of base effects, but the higher oil price will have a limiting effect on energy inflation.

Key events in developed markets next week

Source: Refinitiv, ING

Read the original analysis: Key events in developed markets next week

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.