Global Markets Fall As China Unleashes New Tariffs On US

Yesterday, the Trump administration released a comprehensive list of Chinese imports it would put tariffs on. The list included an assortment of products, mostly in the technological and pharmaceutical sector. Today, as a response, China released its list of American products it would place tariffs on. The list was tactical. It targeted the key American exports like soybeans, airplanes, and motor vehicles. As a result, the major global indices fell because investors feared that a trade war was starting.

In general, the sanctions are relatively small on both sides. They total about $100 billion for countries that trade goods worth trillions of dollars every year. Nonetheless, the two countries have more tools that could have significant consequences. For example, China can stop buying US debt, punish American companies in their country, and levy more tariffs on American goods. Still, the two countries will need to talk because tariffs alone won’t address the underlying problems.

A day after the Reserve Bank of Australia left interest rates unchanged, the country released its retail sales data. The data showed that the retail sales accelerated by 0.6% in February. Analysts were expecting that the sales would increase by 0.3%. In January, the retail sales expanded by 0.2% while in December, they fell by 0.5%. At the same time, the number of building approvals declined by 6.2%. Analysts were expecting the approvals to fall by a slimmer margin of 4.8%. This was one of the major concerns from the RBA officials in yesterday’s statement.

Eurostat today released the inflation numbers of the European Union. Core CPI in the region moved up by 1.0% compared to the estimated 1.1% while the YoY CPI remained unchanged at 1.4%. The major sectors that gained were mostly food and tobacco, while energy prices declined. Meanwhile, in the United States, Automatic Data Processing (ADP) released the employment change that passed analysts’ estimates. According to them, 241K jobs were created in March compared to the estimated 208K. This data gives a preview of what to expect on Wednesday, when we receive the official employment data.

On an hourly chart, the EUR/USD pair has wiped the gains made since March 21 when the pair started soaring. The climb saw the pair reach a high of 1.2476, before starting to fall to the current 1.2290. During this decline, the pair has managed to complete a corrective Elliot Wave. Today, the pair is reacting to several data sources such as EU inflation, prospects of a trade war, and the positive ADP job numbers.

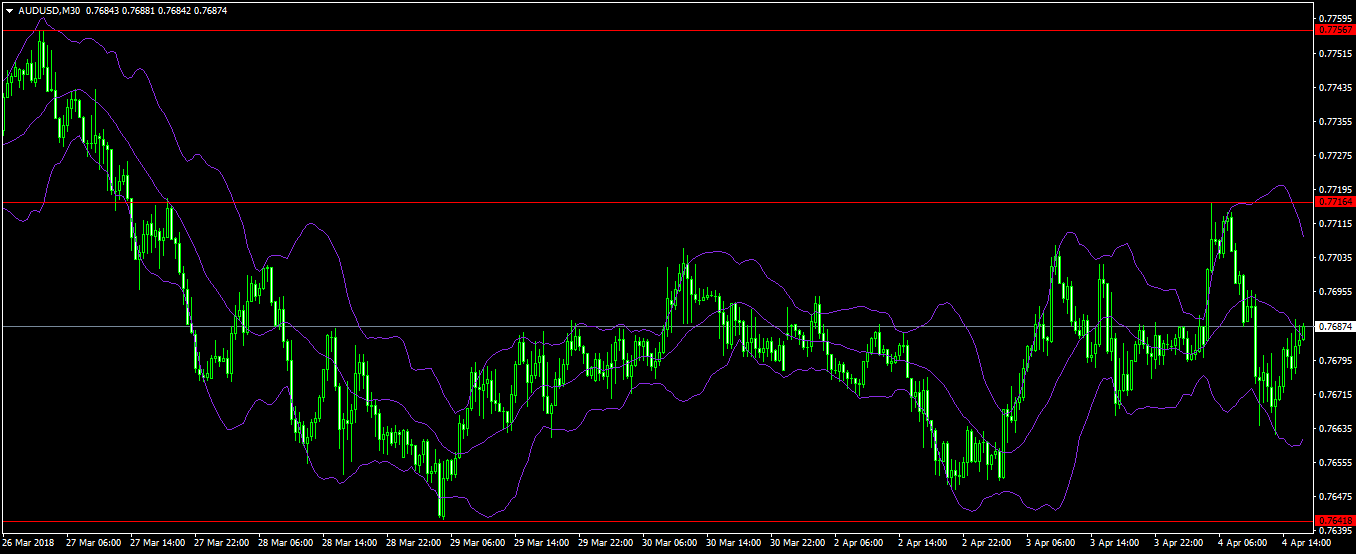

AUD/USD

The pair traded within a narrow range today, a few days after falling to a low of 0.7741. Today, the pair fell from an intraday high of 0.7716 to a low of 0.7660 after data from Australia showed accelerating retail sales. From the United States, ADP data showed that employers were accelerating hiring. Nonetheless, in traders’ mind today was the issue of trade and how a war would impact the different economies.

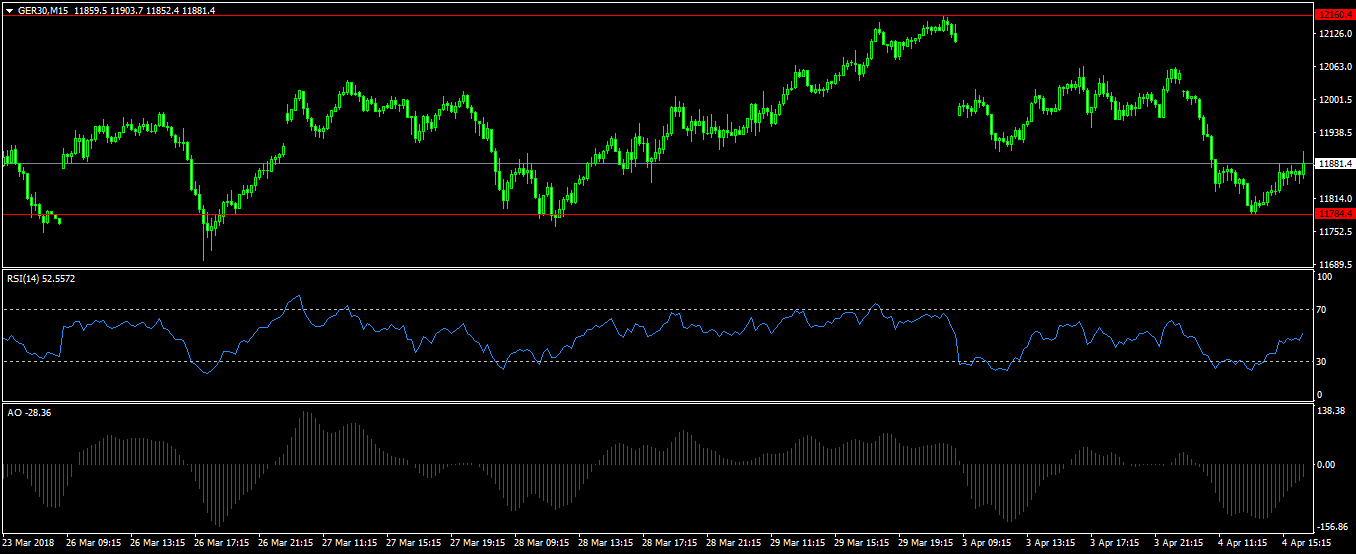

DAX

The DAX is an index of the 30 biggest companies in Germany. Today, the index continued the decline it started yesterday, when it fell from a high of €12,160 to a day’s low of €11,784. Today’s decline was attributed to the ongoing trade issues. Today’s decline was led by companies like Infenion, Lufthansa, and Continental. The only outliers on the gaining side were Adidas, Biersdorf, Merck, Bayer, and Henkel. There is a likelihood that the index will rise after the fears on trade ease.

Author

OctaFx Analyst Team

OctaFX

OctaFX is a market-leading forex broker, providing personalised forex brokerage services to customers in over 100 countries worldwide.