GBP/USD Weekly Forecast: Rate laurels go the the US Federal Reserve

- BOE leaves rates, asset purchases unchanged, warns on inflation.

- Federal Reserve and Chair Powell set the stage for bond taper.

- US Treasury rates move sharply higher after the FOMC meeting.

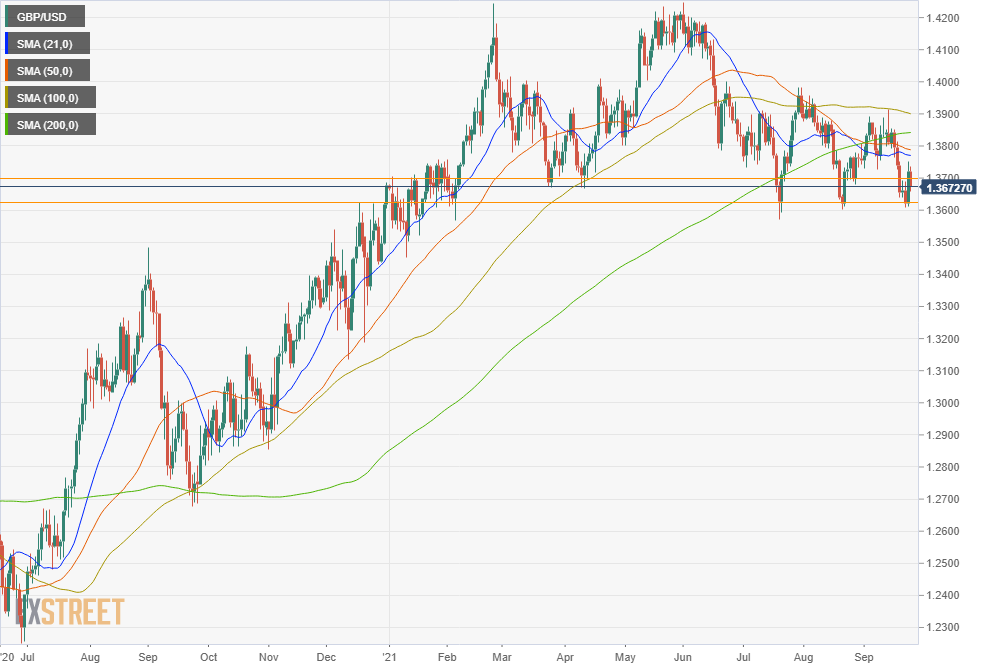

- GBP/USD drops below 1.3700 in Friday trading.

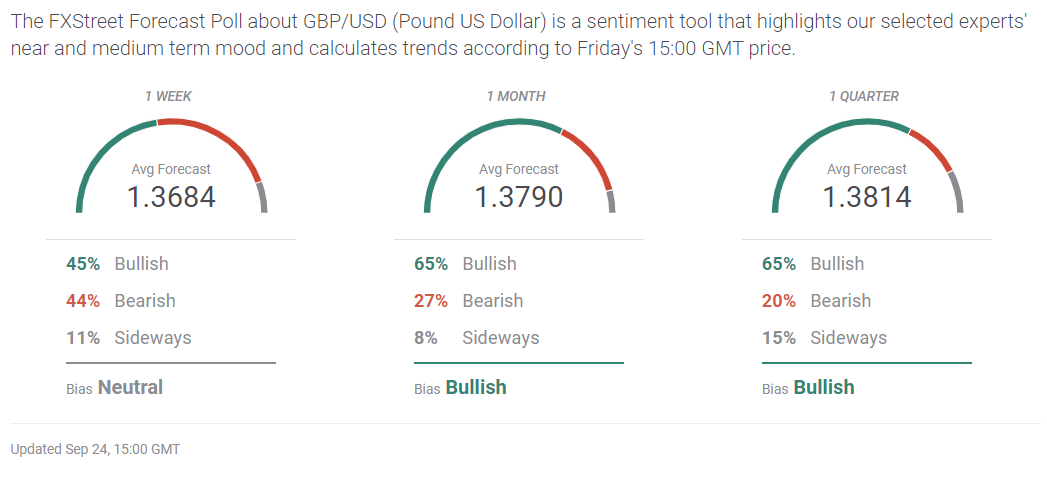

- FXStreet Forecast Poll predicts stronger sterling.

The Bank of England and the Federal Reserve are on the same rate page in the central bank policy book, but the US institution appears to be a few paragraphs ahead.

Two meetings this week indicated that the Bank of England (BOE) and the Fed are moving to curtail and then end their extraordinary bond purchases. These programs have kept sovereign and commercial interest rates near historic lows since last March.

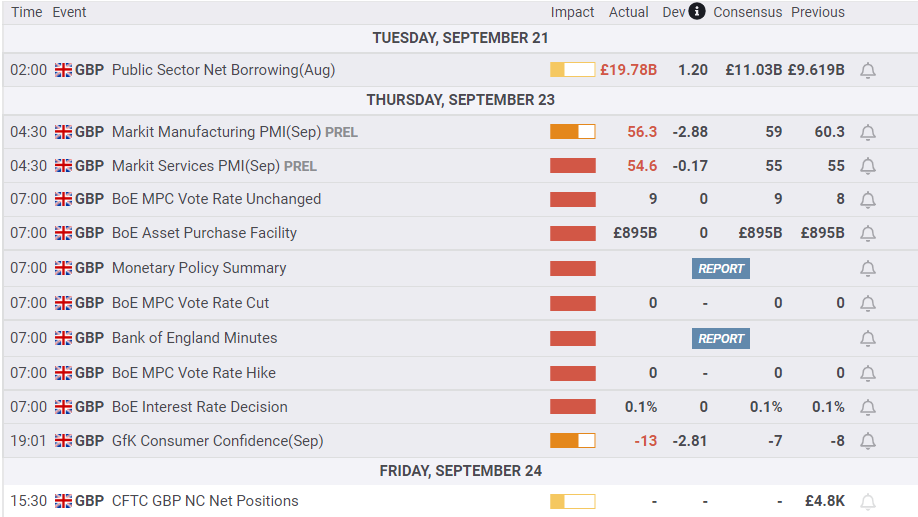

In the UK, the case for reducing the £875 billion asset facility received two additional votes in the Monetary Policy Committee (MPC) meeting on Thursday, after the members voted 8-1 to keep the main rate at 0.1%.

On inflation, the bank warned that prices could rise above 4% this year largely on energy spikes, and lowered its third-quarter GDP forecast to 2.1% from 2.9%. European natural gas prices have skyrocketed as shortages and restrictions have played havoc with the market.

The GBP/USD moved sharply higher to 1.3721 on Thursday following the BOE meeting after falling from 1.3741 on Monday to 1.3622 on Wednesday.

The return on the UK 10-year gilt rose 12 basis points from Wednesday to Thursday at 0.916%, but then barely moved to Friday’s close at 0.918%

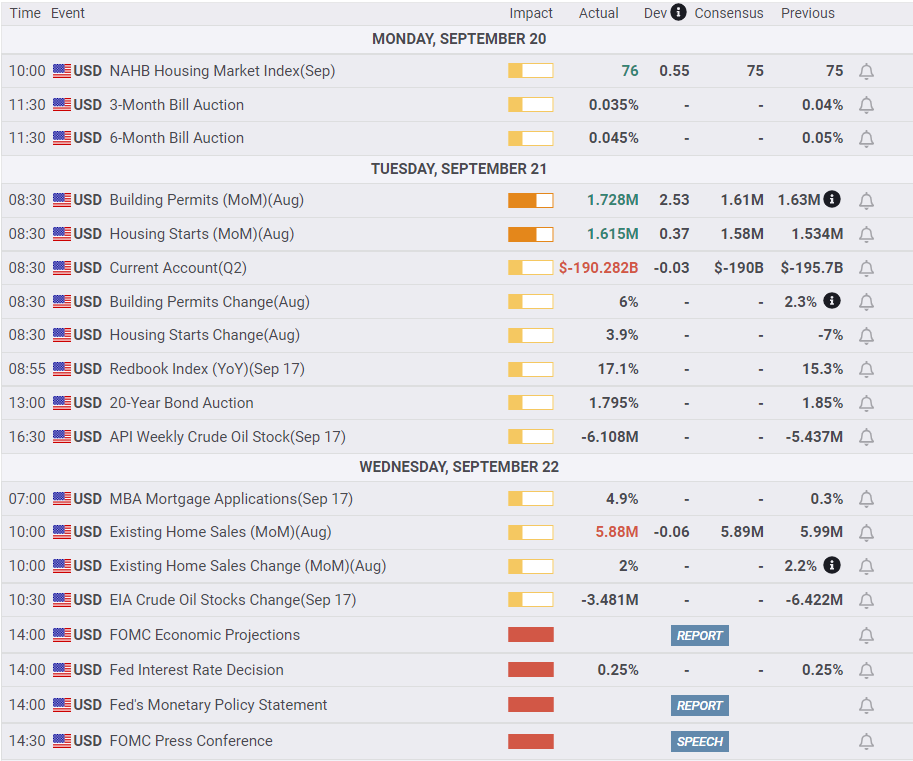

The Federal Reserve meeting on Wednesday gathered only a minor response in the currency and credit markets despite Chair Powell’s observation that most of the members as well as himself, thought the criteria for a bond taper had been met. The bank’s own forecast projected a funds rate hike next year for the first time since the pandemic began 19 months ago. The 10-year Treasury yield added just one point to close at 1.333% on Wednesday.

Thursday and Friday the Treasury market reconsidered. The 10-year yield jumped 12 points to 1.451%, its highest level since July. The 30-year long bond rose 13 basis points to 1.978%. With the 2-year return rising just 3 basis points to 0.272%, the yield curve steepened notably.

The later week reversal in US Treasury yields brought the GBP/USD below 1.3700 and back into the lowest part of its eight month range.

The BOE and the Fed are moving toward ending their pandemic economic support. For the moment the Fed seems to be in the lead, and that will limit the sterling until the Old Lady of Threadneedle Street catches up.

For the UK, the BOE meeting was the only market development of note. Purchasing Managers' Indexes in services and manufacturing for September were slightly weaker than forecast but remained firmly in expansion.

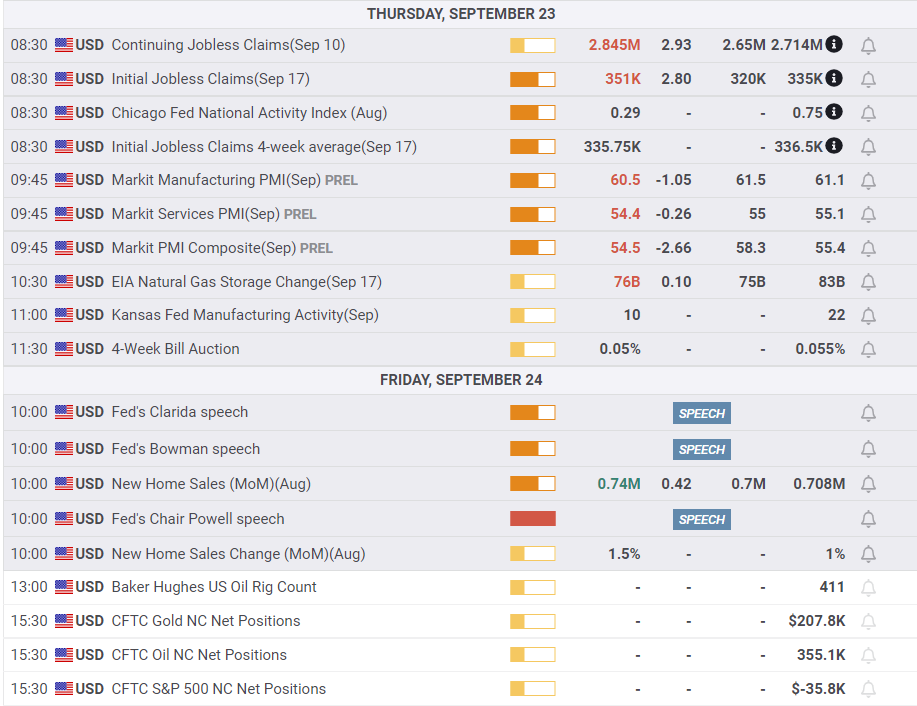

In the US, stocks recovered from Monday’s China-inspired sell-off, returning to last week’s level by Friday. Existing Home Sales, 90% of the US market, performed as expected in August, and Initial Jobless Claims rose for the second week in a row, though neither affected markets.

GBP/USD outlook

The technical weakness shown by the drop through 1.3700 combined with the US Federal Reserve’s taper aggression bodes ill for the GBP/USD. The US 10-year yield added 4 basis points on Friday while the 10-year Gilt return stagnated.

Wednesday’s finish at 1.3622 was the lowest since January 15 and if, perhaps we should say when, it is breached, the absence of any technical support below that level with a reference nearer than the first two weeks of the year is a marked weakness.

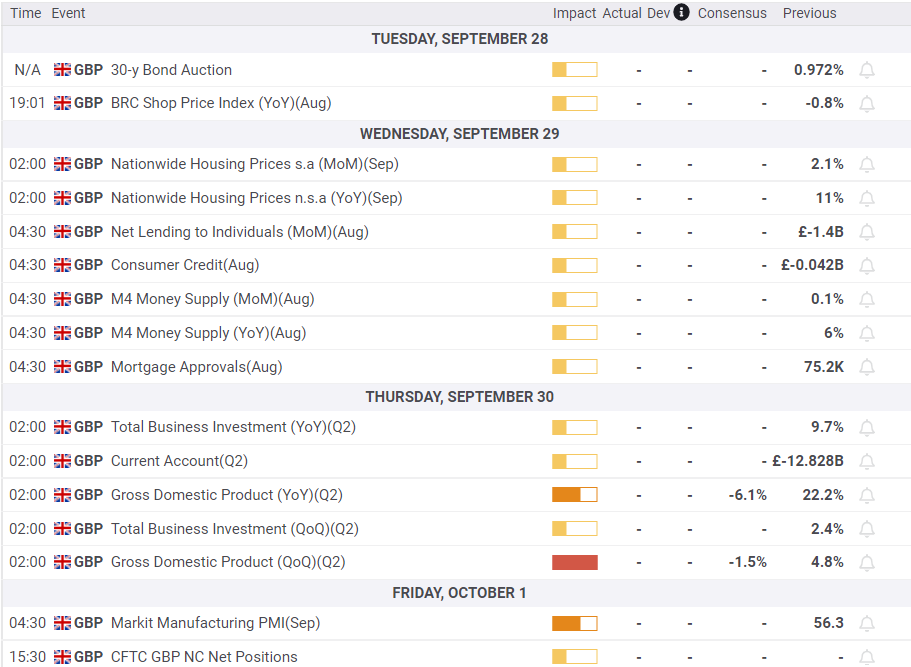

Economic information in the UK begins with home prices for September. Annual prices have gained more than 10% for the last four months, a fact noted by the BOE. Economic growth is expected to turn negative in the second quarter as pandemic restrictions again interfered with the recovery.

US data in the week ahead begins with Durable Goods Orders for August, essentially a restatement of the Retail Sales figures. An important exception is the Nondefense Capital Goods Orders category, a much followed proxy for business investment. The manufacturing Purchasing Managers’ Index will shed insight on whether the factory sector is surmounting labor and material shortages and price inflation.

UK statistics September 20–September 24

US statistics September 20–September 24

FXStreet

UK statistics September 27–October 1

FXStreet

US statistics September 27–October 1

GBP/USD technical outlook

The sterling maintained its technical weakness despite Tuesday's rebound after the BOE meeting. The MACD (Moving Average Convergence Divergence) turned negative on Monday and has kept that outlook. The Relative Strength Index (RSI) has been below 50 since last Friday despite Wednesday's return. It headed lower on Friday. True Range also peaked on Thursday with declining momentum on Friday.

The 21-day moving average (MA) at 1.3771 and the 50-day at 1.3788 were crossed last Friday and have not been approached since. Even Thursday's post-BOE run stopped at 1.3750, well short of intersection. Those MA's form a substantial band of resistance. Only the 200-day MA retains a slight upward cast and at 1.3842 is coincident with resistance at 1.3850.

The prevalence of resistance over support is a good expression of GBP/USD's technical weakness.

Resistance: 1.3700, 1.3740, 1.3870 (21, 50 MA), 1.3842 (200 MA), 1.3900 (100 MA)

Support: 1.3625, 1.3570, 1.3500, 1.3440

FXStreet Forecast Poll

The FXStreet Forecast Poll sees only a minor pullback before the pound takes 1.3800.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.