GBP/USD Weekly Forecast: Opening Pandora’s box of No Brexit set to support Sterling as UK parliament is set to reject the Brexit deal

- With the UK parliament scheduled to vote on Brexit deal on Tuesday, January 15, expectations of deal rejection rise.

- The European Union officials increasingly lean toward a delay in Brexit date.

- A No Brexit option emerged as a last minute option on the table.

- Brexit developments are likely to overshadow the UK inflation and retail sales data due during the third week of January.

- FXStreet Forecast Poll turned bullish as No Brexit option supports the optimism.

The GBP/USD was mired by rising Brexit uncertainty that kept the currency pair trapped in a range of 1.2700-1.2820 during the second week of January. The unexpected twist in Brexit rhetorics toward delayed Brexit or even No Brexit at all supported Sterling at the end of the week while increased patience in the US Federal Reserve’s outlook for rates weighed on the US Dollar keeping Sterling at the bay of 1.2700-1.2800 range.

The speculation of delayed Brexit broke out on Friday with the Austrian Prime Minister Sebastian Kurz indicating delay to Brexit date being the only option in case of no Brexit deal progress next week in the UK. Reports saying the European Commission President Juncker is expected to send a letter confirming Irish backstop assurance on Monday in an attempt to help Brexit deal to pass in UK parliament added support to Sterling on Friday to rise to the highest level since December 4 last year of 1.2851.

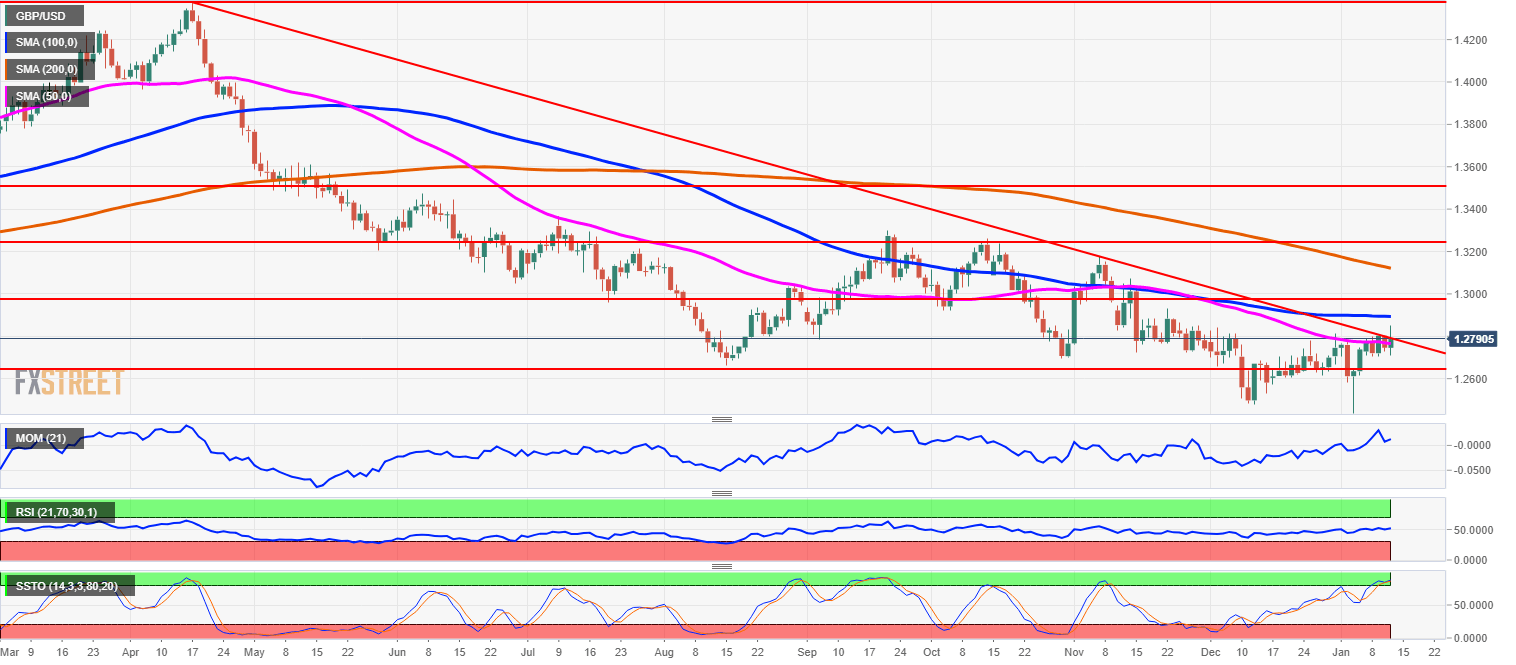

With the break above 1.2800, the GBP/USD technically rose above the long-term downward sloping trendline. Nevertheless, the retreat below the trendline indicates that the FX market is sensibly discounting much more fundamentally important Brexit related drivers in the week ahead to see technical breakouts as an indication of the future currency move.

While the UK economic calendar was very light during the second week of January with the Bank of England Governor Mark Carney’s participation in the online discussion being the main event, the US Federal Reserve’s Decembre meeting minutes and numerous speeches from the Fed officials highlighted last week.

Regarding the US Dollar, there were two main themes affecting the FX market in the second week of January. First, it was the ongoing progress in the US-China trade talks that supported the US Dollar. A second and fundamentally more important theme was related to the reprisal of chances for rate hikes in the US in 2019. The FOMC December meeting minutes disclosed the data dependency of the US central bank with some policymakers indicating the end of the rate hiking cycle. Atlanta Fed President Raphael Bostic said on Wednesday that the monetary policy could move in either direction and that he open to a rate cut if downside risks all come to bear.

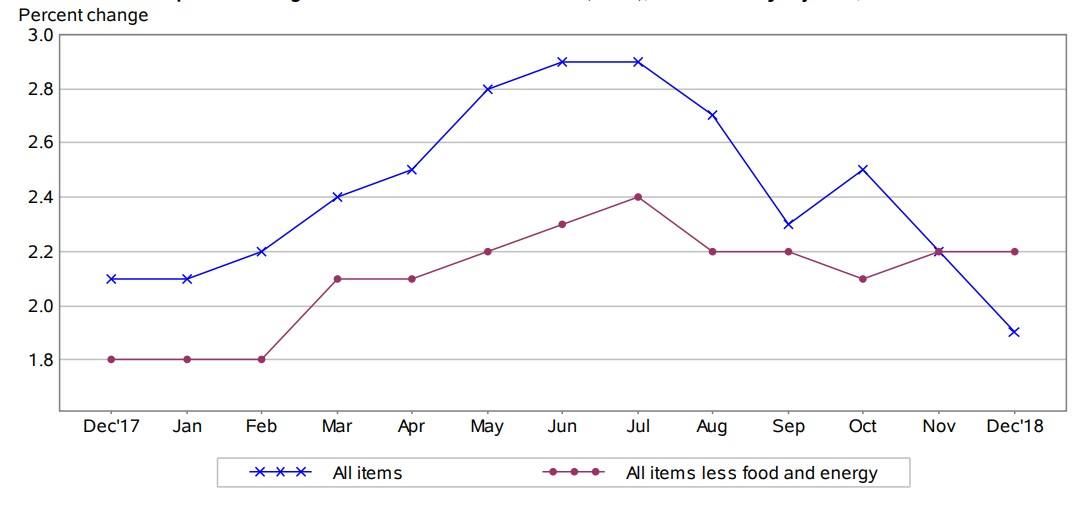

The US inflation was a macroeconomic headline of the week, but as prices remained stable in December with the US headline inflation rising 2.2% over the year and core inflation up 1.9% y/y, the market was little moved.

US headline and core inflation 2017-2018

Source: Bureau of Labor Statistics

The week ahead is expected to see the UK parliament vote on Brexit deal on Tuesday, January 15 and this is the key risk event for the currency. The UK inflation is expected to decelerate to 2.2% y/y in December, while UK retail sales are expected to record another monthly decrease in the same period. The US economic calendar schedules retail sales in the upcoming week. The currency market is thought likely to remain driven by the ongoing trade talks between the US and China and the outlook for the monetary policy path in 2019 in the US while future of Brexit is the most important event in the week ahead of all.

Technical Analysis

GBP/USD daily chart

Technically, the GBP/USD is trading in a downward sloping trend on a daily chart while capped by a trendline and oscillating above a 50-day moving average at 1.2770. The technical oscillators including Momentum and the Slow Stochastics remain elevated after the false breakout above the trendline supported by Brexit delay talks. Slow Stochastics is moving deeply in the Overbought region and correction on GBP/USD lower is set to generate a bearish crossover signal. The Relative Strength index though still remains flat. The GBP/USD is expected to remain increasingly sensitive to Brexit news, with Brexit deal defeat likely to weigh on the currency pair while markets temporarily discount the drift in the US monetary policy outlook on speeches from Fed policymakers. Brexit deal uncertainty is weighing on Sterling ahead of a Brexit deal vote with failure to pass the deal seen creating further chaos and fundamentally pressing on GBP/USD to fall further towards 1.2500-1.2600 level.

Summary of Fed officials speeches last week

The Federal Reserve Chairman Jerome Powell said at the Economic Club in Washington DC on January 10:

- Financial markets expressing concerns about downside risks.

- Inflation is low on under control giving the Fed ability to be patient given inflation data.

- The labor market is very strong by many measures.

- Fed has two rate hikes median in summary of economic projections.

- Does not see any evidence of a slowdown.

- Markets seem to be pricing and pessimism on growth, trade can move policy flexibly and quickly if economic data warrants it.

- Don't see anything showing elevated recession risks.

- Government shutdown typically doesn't last long.

- No inflation risk that would require the Fed to hit the brakes.

- Sees 2019 inflation around 2% strongly anchored inflation expectations.

- A slowing economy in China is a concern for the US.

- We want to return the balance sheet to a more normal level.

- There is no appropriate level of the Fed balance sheet but it will be "substantially smaller" then it is now.

- The unemployment is moving down a bit if Fed outlook met

- Fed is very flexible in adapting policy if the economy moves.

Richmond Federal Reserve President Barkin and a non-voting member of the FOMC said on January 10:

- Expects US growth to continue through at a somewhat slower pace.

- The trend core growth is only in the 1.9% range.

- Hears concern partly driven by trade, politics, market, margin pressure.

- Productivity slowdown is real, due partly to business underinvestment.

- The US is not heading to a sustainable place on a deficit.

- Uncertainty more challenging for the economy.

- Direct impacts from tariffs right now is not significant.

- Fed is very much focused on hitting its inflation target.

- Normalizing rates is not aimed at restraining the economy.

- I do not believe we are at neutral yet, but we are near.

Boston Federal Reserve Bank President Eric Rosengren said at the Boston Economic Club on January 9:

- When short-term rate futures start pricing in rate cuts, it "catches my attention."

- Rosengren is not paying attention to signals from financial markets on rate expectations.

- Prefers to rely on adjustments of short-term rates, not to balance sheet.

- Fed is "mildly accommodative" now, says he is perfectly content to stay there.

- The economic growth of 2%-2.5% over the next year seems "quite reasonable."

- Worries about the extent of leverage he's seeing in the corporate sector.

Chicago Federal Reserve President Charles Evans and a voting FOMC member said in the speech on January 9:

- Sees growing risks but still expects US rates to rise a bit above neutral if they dissipate.

- The first half of 2019 'very important' in deciding the eventual policy path.

- Given tame inflation, the Fed can "wait" and take stock of incoming data.

- US fundamentals are solid but cross-currents "tough to read" in "fluid" environment.

- The policy should be based on cautious data dependence.

- Tighter financial conditions May be healthy "recalibration" after earlier optimism.

- Downside risks include growth abroad, US trade policy, fiscal headwinds.

- Sees inflation near the target in 2019, a bit above in 2020/2021.

- Sees unemployment falling toward 3.5%, a bit higher by end of 2021.

- Monthly US job gains now much more likely to be 60,000-100,000 at this point in US economic expansion.

- US government shutdowns usually have a relatively small effect on the real economy.

- Expects three US rate hikes in 2019 if his forecasts are met.

- The timing for policy tightening "not all that important."

- "Very good time" to wait to see how data play out, watching political developments.

- Financial tightening not yet apparently hurting US consumers.

- Policy setting now at a pretty good place; US outlook good; no clear inflation pressure.

- December jobs report "extremely strong."

St. Louis Federal Reserve President James Bullard and a voting FOMC member said for the Wall Street Journal on January 9:

- We’ve got a good level of the policy rate today.

- There’s no urgent need to go higher.

Atlanta Federal Reserve President Raphael Bostic and a non-voting FOMC member said on January 9:

- The policy could move in either direction; open to a rate cut if downside risks all come to bear.

- Business contacts indicate firms are becoming defensive in planning for a slowdown, holding off on investment plans.

- Likely slowing growth in 2019 is not the result of fundamental weakness in the economy, but return to trends driven by slow growth in the labor force.

- Message from markets is that both main street and Wall Street are concerned about risks to growth.

- Fed needs to be patient and seek "greater clarity" on economic risks as it mulls further rate increases.

Atlanta Federal Reserve President Raphael Bostic and a non-voting FOMC member said on January 7:

- “I am at one move for 2019,” Bostic said commenting on interest rates outlook.

- The US economy looks “pretty solid”.

- Market volatility attributed to uncertainty over trade policy and global economic “clouds”.

- The US government shutdown to have a small aggregate impact on the economy if it stays short.

The economic calendar in the upcoming week

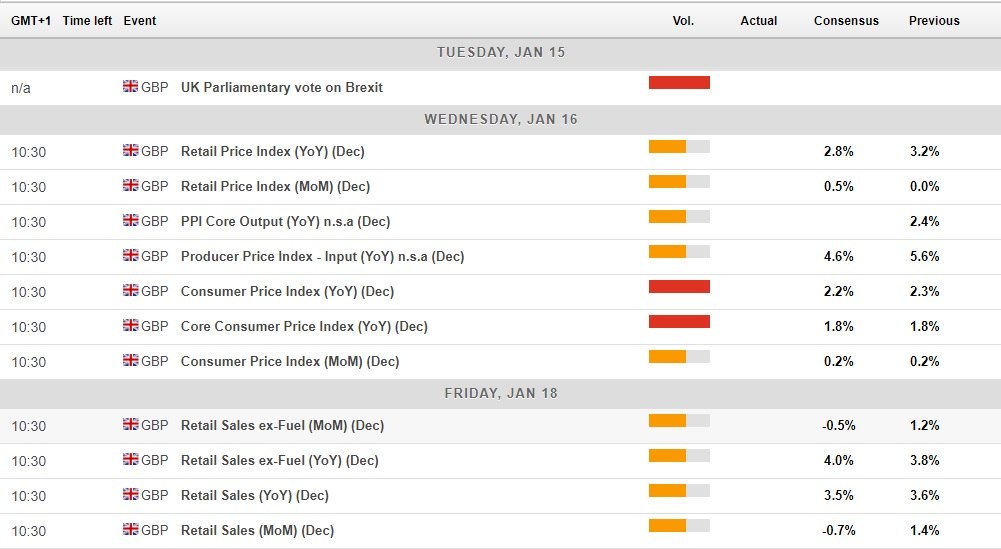

The UK economic calendar features December inflation data and the December retail sales report. The fundamentally most important event is scheduled for Tuesday evening with the UK parliament voting on Brexit deal. While it is unlikely for the UK policymakers to pass the Brexit deal as it is now, the impasse is set to continue because of the UK parliament over voted the UK government and banned it from leaving with no-deal Brexit.

Such a situation is, therefore, increasing the chances of delayed Brexit, that is likely to be short-term supportive for Sterling.

On the data front, the UK inflation is expected to have decelerated to 2.2% in December, down from 2.3% in the previous month while core inflation stripping the consumer basket of food and energy prices is seen dwelling at 1.8% y/y. Reporting for the same month of December, the UK retail sales are seen falling -0.7% m/m, confirming the negative trend from the previous months.

UK economic calendar January 14-18

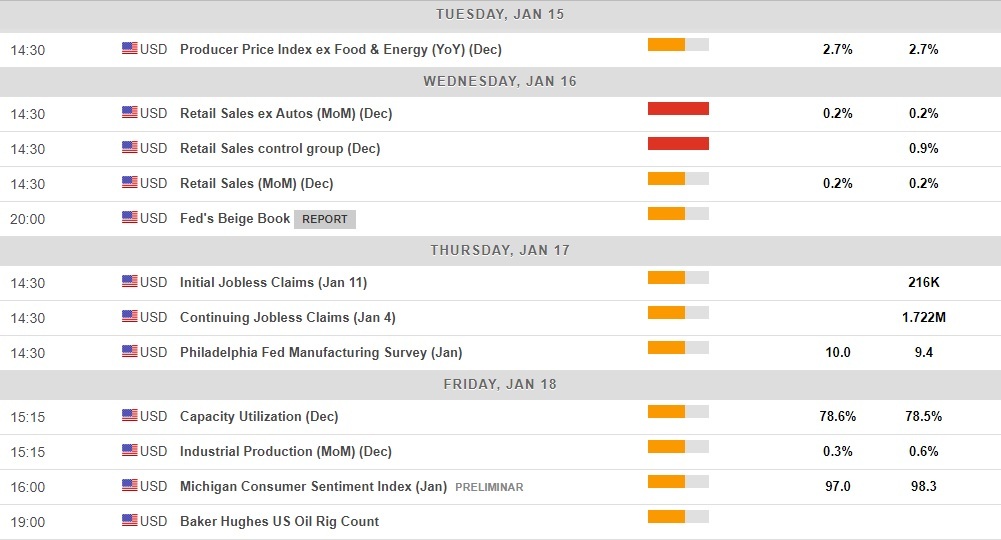

On the other side of the Atlantic, the US economic calendar features December retail sales report with the headline and core sales both expected to rise 0.2% over the month. The set of the US Federal Reserve policymakers speaking will continue with the New York Fed President John Williams scheduled for Friday. Williams is expected to repeat the message of Chairman Powell on patience and data dependent Fed with the market reaction on the dovish side and the US Dollar weakening.

US economic calendar January 14-18

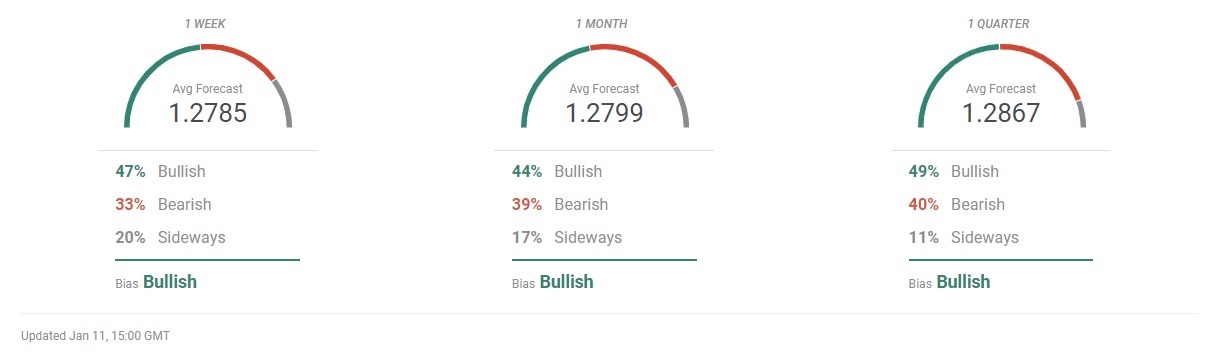

FXStreet Forecast Poll

The FXStreet Forecast Poll turned short-term bullish with the spot rate of 1.2785 expected in the 1-week horizon, up from 1.2552 last week. The majority of forecasters see Sterling rising (47%) compared with 33% of bearish and 20% of sideways projections.

For longer-term forecast, the predictions are more evenly split.

The average forecast for one month ahead sees GBP/USD rising to 1.2799, up from 1.2763 seen last week while bullish-to-bearish forecasts narrowed to 44%-39 compared with 57%-43% last week. The three months' forecast reflects rising Brexit uncertainty with average FX rate at 1.2867, down from 1.2968 last week and 49%-40% bullish-to-bearish split compared with 56%-15% projection last week.

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.