Fed Preview: Balance sheet to the fore

-

Interest rate policy to remain unchanged, Fed Funds at 2.5%

-

Focus will be on the disposition of the Fed's balance sheet

-

Economic and government concerns will absorb the FOMC and Chairman Powell’s press conference

FOMC

The Federal Open Market Committee, the policy making body of the US central bank is expected to keep its base rate at 2.5% at the conclusion of Wednesday’s two day meeting. The bank has projected two 25 basis point increase in 2019 but given little indication when those might take place. The December 2018 economic and rate projections posit a GDP expansion of 2.3% for the year and a Fed Funds rate of 2.9% on December 31.

US economy: growth on track

The US retains its growth propensity. Economic expansion in the first three quarters of 2018 measured 3.67%, and the full year rate will likely be over 3% for the first time since 2004. Fourth quarter annualized GDP is forecast by the Atlanta Fed GDPNow model to be 2.7%, which would place the year at 3.125%.

Job creation remains strong. Non-Farm payrolls averaged 206,000 new positions a month for the year. The best performance since 2015. Unemployment fell from 4.1% in the first quarter to 3.7% in September, October and November the lowest in 49 years, before returning to 3.9% as 400,000 people rejoined the work force in December. Wages moved to their highest annual gains since the recession reaching 3.2% at year end, a rate that will move higher as labor shortages pressure employers. Manufacturing work, long considered a dying sector by economists and politicians, had its best year in two decades.

FOMC Economic and Rate Projections: Doubt creeps in

The robust US economy did not prevent the Fed from ending the year with evident concerns. The bank publishes its economic and rate projections four times a year, the last for 2018 in December. In those materials the outlook for economic growth and the Fed Funds rate were reduced for the first time in over two years. The estimate for 2019 GDP slipped to 2.3% from 2.5% and the base rate projection for December became 2.9% instead of 3.1%, implying two 0.25% increases from the current 2.5% instead of three.

The Fed’s logic, muted in the FOMC statement but more directly expressed in speeches by Chairman Powell and several other voting members of the FOMC revolved around the effect of global economic and political risks on the US economy.

The US-China trade dispute, then and now on hiatus and under negotiation until March 31st is the most important. Agreement on trade that removes tariffs and opens both countries to higher levels of mutually approved trade has the potential to power the global economy and mitigate concerns emanating from Europe. Conversely an escalating dispute would do more than justify the IMF’s caution on the growing risks to global growth.

FOMC Statement

As always the FOMC statement will be parsed for changes in wording and inflection. The December text stated, “The labor market has continued to strengthen and that economic activity has been rising at a strong rate. Job gains have been strong, on average, in recent months, and the unemployment rate has remained low. Household spending has continued to grow strongly, while growth of business fixed investment has moderated from its rapid pace earlier in the year.” The committee also judged “that risks to the economic outlook are roughly balanced.” With the bulk of Fed economic concerns external to the US and the economy remaining strong alteration here would be significant.

The committee has four new voting members this year, Charles Evans of Chicago, Eric Rosengren of Boston, Esther George of Kansas City and James Bullard of St. Louis. With no policy changes on tap and the bank far from considering a change a dissent would notable.

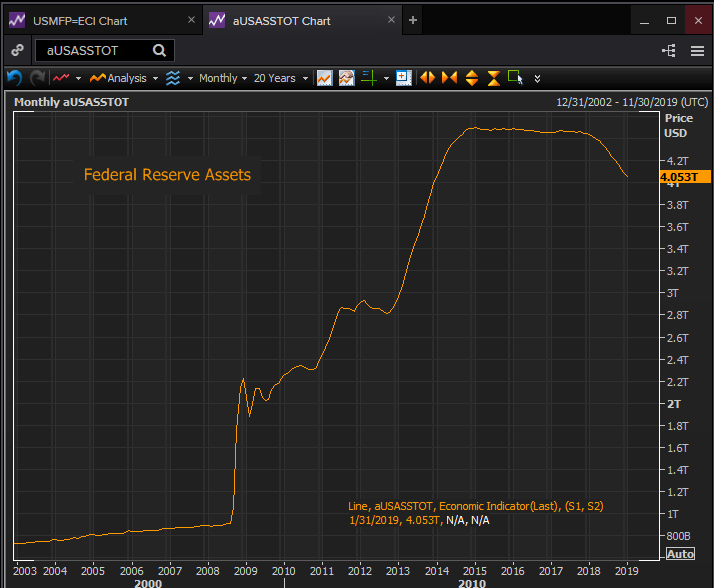

Federal Reserve Assets: Is a bond diet good for the economy?

The Fed has been reducing its huge stock of financial assets acquired in the years after the financial crisis for a little more than a year.

The Fed stopped buying new bonds in 2014 with the end of quantitative easing but for the next four years it maintained its supply by rolling over expiring securities. The bank reinvested the proceeds of the maturing asset in a new security. By doing so it negated any effect the sale might have on market interest rates.

Chart: Reuters

Bond prices trade inversely to rates. When the Fed sells a tranche of securities it can force bonds prices lower, depending on the size of the sale. This can, again depending on the size of the sale raise market rates. If the sale is not balanced by an equal purchase, rates have the potential to stay at the level left by the sale.

As important as the actual sale is the knowledge that the Fed is a long term seller of securities. With a balance sheet that expanded over 400%, from under $1 trillion in 2008 to $4.5 trillion in 2014 the long term effects of this reduction could stretch to more than half a decade.

The Fed was a net seller of about $500 billion of bonds and securities in 2018. If the goal was a $1 trillion balance sheet that would take six years at half a trillion dollars a year. Starting in 2018 it would end in 2023. The assumption for that schedule would be that there is no recession in the intervening years that would force the FOMC to reduce rates, cease sales or reinstitute purchases.

The logic for reducing the bond portfolio in an economy that is not exhibiting any signs of overheating or inflation is that same as that for raising the Fed Funds rate. It is storing up potential rate cuts and bond purchase for the next recession.

The bond autopilot

In his press conference after the December FOMC meeting Chairman Powell referred to the balance sheet reduction being on “autopilot”. That comment did not fully jibe with the Fed’s new found caution as expressed in the economic and rate projections and the speeches of several governors subsequently.

Mr. Powell has since counseled patience on rates and the bond reduction. The Wall Street Journal reported that the Fed is considering halting its portfolio sales.

Market implications and the dollar

The FOMC statement is unlikely to specify any changes in the bond program.

If there is an alteration in the Fed’s plans or the pace of bond sales it will be in Chairman Powell’s statement or in the question and answer of the press conference. Stated or implied, a halt or reduction in bond sales will impair the dollar and boost equities, partially because it will be a surprise, though perhaps not a huge one. Continuation of the present bond program will provide the dollar with modest support.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.