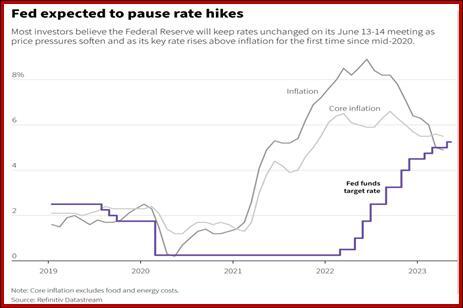

Will the Fed hike materialize?

Outlook: Today we get the usual Thursday jobless claims, which may be interesting in light of the household survey delivering a rise in unemployment last week. The light calendar means we can start thinking about the Fed policy meeting next week and the inflation data due on June 13th (April core having delivered 5.5% vs. the 1957-2023 average of 3.63%, information courtesy of Trading Economics).

In April the core was down 0.1% from the month before but this time, so far the consensus seems to be no change. We need to be a little worried about that because a no-change reading implies the entrenchment of an inflation mentality among consumers, but not a big worry because the Fed doesn’t look at headline. It looks at the PCE version.

The latest shocker was the Bank of Canada ending its pause (from January) to hike by 25 bp yesterday, right after the Reserve Bank of Australia did the same thing. Both central banks had warned the pauses were conditional and they were going to watch the data like a hawk at the time of the pause, and both said this week they were dissatisfied with the data showing the pace of inflation slowdown.

Despite a near universal consensus that the Fed doesn’t take its cue from those other central banks and instead watches its own data, there is some angst that “skipping” a hike in June might come off the table. The usually savvy folks at Deutsche Bank are among those who wonder if the Fed might do the same thing.

But a one-time skip is not the same things as an indefinite, if data-dependent, “conditional” pause. Or is it? The financial markets are populated by people with mad arithmetic skills but who are not great readers or fans of the nuance of language. Their cack-handed invented terms are cringe-making (“dovish hike”).

Accordingly, the probability of a surprise hike by the Fed next week went up to 33.3% from 20.4% the week before, according to the CME FedWatch tool. We appreciate this is betting, not forecasting, but still, it shows the players in this market are not Thinkers.

Forecast: The dollar retains its strong tone even as some other currencies are straining at the bit for a gain (GBP). The hourly charts are so messy it’s tempting to get out and stay out.

Tidbit: Reuters reports volatility is low everywhere. Low vol (the “squeeze” in Bollinger band terms) precedes every breakout but it’s important to note that not every squeeze results in a breakout. “The VIX index (.VIX) clocked another post-pandemic closing low and remains close to that on Thursday. The MOVE (.MOVE) index of bond volatility edged back higher from 3-month lows set the previous session, but overall currency volatility (.DBCVIX) hit its lowest since February 2022.”

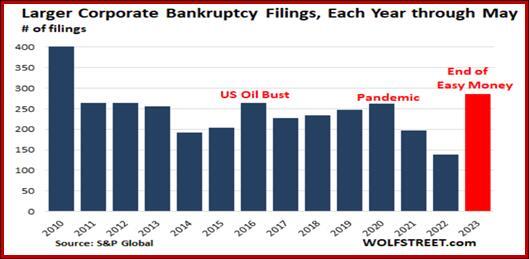

Tidbit: Wolf Street has a story on the rise in bankruptcies, and that’s before commercial real estate hits the fan. Bankruptcies are up by 54 in May alone, for the year-to-date to 286 filings, double the equivalent number last year and the highest since 2010. We like the editorializing: “There is a cleansing aspect to this part of the credit cycle that needs to be allowed to do its job to get rid of the excesses and the deadwood at the expense of investors. This cleansing process that has now just started is long overdue.

“Hilariously, the end of Easy Money is now called credit crunch. Which should be the name of a candy bar (Credit Crunch®) offered to the crybabies on Wall Street when they start clamoring for rate cuts.”

Tidbit 2: Bloomberg reports that Bridgewater’s former CEP Ray Dalio is sticking to his recession story although now he names it something else. “We are at the beginning of a late, big-cycle debt crisis when you are producing too much debt and have a shortage of buyers,” he said at a conference. “He said while interest rates won’t go much higher, the economy will get worse, and that could cause more internal strife if the US continues to have political fragmentation.” We think the Wolf version is more realistic and political fragmentation has nothing to do with debt or economic performance.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat