What the US midterm elections mean for the dollar and stocks [Video]

![What the US midterm elections mean for the dollar and stocks [Video]](https://editorial.fxstreet.com/images/Macroeconomics/Events/US Elections/Donald-Trump-campaign.jpg)

On November 8, American citizens will head to the polls to elect their new Congress. Opinion polls and prediction markets argue the Republicans will take back at least one chamber, setting the stage for two years of political deadlock. Such an outcome could spark a relief rally in equity markets, and perhaps some profit-taking in the mighty dollar.

Power shift

With less than three weeks to go, investors are grappling with how this election could impact US government policy and financial markets. The Democrats currently hold a slim majority in the House of Representatives while the Senate is split 50-50, with Vice President’s Harris’s tiebreaker vote giving the Democrats control. Most prognostications suggest it would be a miracle if they keep control of both chambers.

Opinion polls clearly favor the Republicans to win back the House. According to simulation models by FiveThirtyEight, the probability of this scenario is around 70%, while betting odds in most prediction websites are even higher at 85%. The Senate is a much closer call, with both opinion surveys and bookmakers viewing it almost as a coin toss.

There is a long list of contentious issues at the heart of this election including abortions rights, climate policy, and threats to democracy. Nonetheless, the economy could still steal the spotlight amid the worst cost of living crisis in decades and rising concerns that a recession is on the horizon.

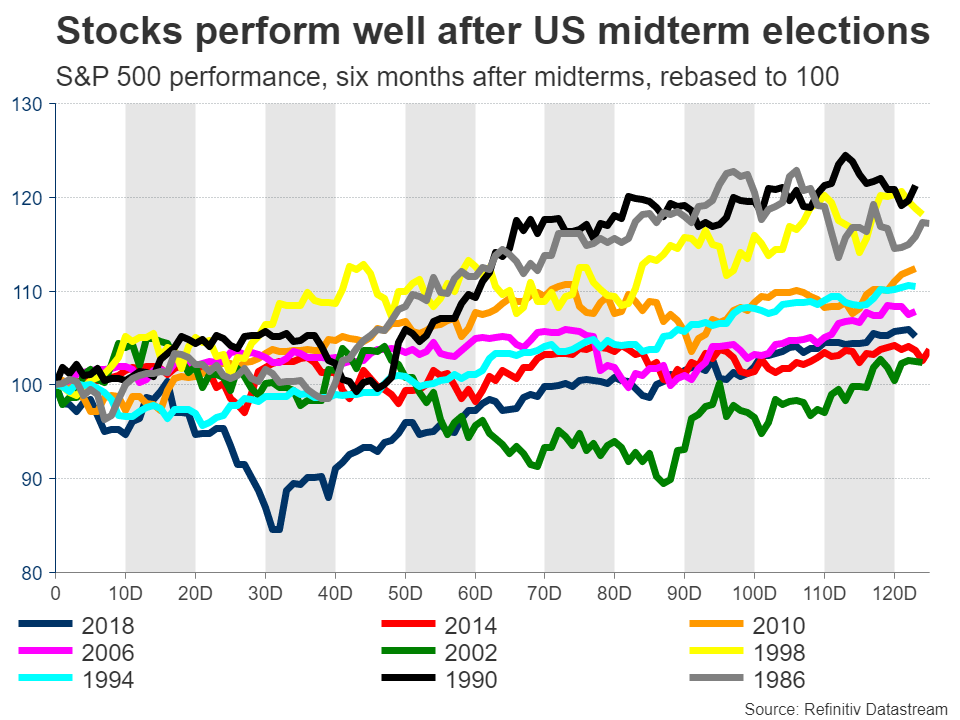

Stocks like a divided Congress

Historically speaking, stock markets tend to perform poorly in the months heading into midterm elections, but then stage sharp rallies after the event has passed. The logic behind this pattern is that investors often hedge or cut their market exposure because of the political uncertainty, and then unwind those hedges once they have clarity of the outcome.

Over the last seven decades, stock markets have always been higher six months after a midterm election. Of course that doesn’t mean much in a year as rocky as this one. Markets will be driven mostly by how inflation evolves, how high the Fed raises interest rates, and whether a recession actually hits. Still, it’s useful to look at the historical precedent.

A divided Congress may prove beneficial for equity markets because it would strip President Biden’s power, limiting the scope for enacting anti-business legislation such as raising corporate taxes or tightening regulations. Even if the Republicans gain control of one chamber, they would almost certainly veto such laws, eliminating one risk facing investors.

The risk is that a split Congress is already the market’s baseline scenario. Hence, if the Democrats manage to pull off the upset victory and keep both chambers, that could spark a substantial selloff, although the likelihood seems quite low.

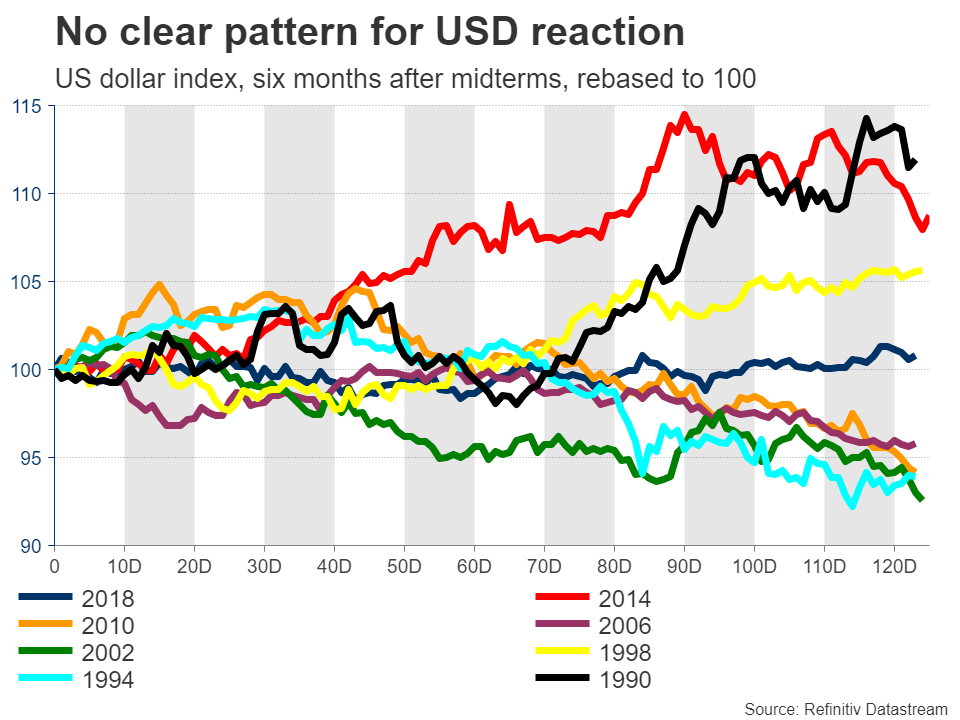

What about the dollar?

Turning to the US dollar, there is no clear historic pattern after midterms. The market reaction will boil down to how the election affects the trajectory of Fed policy. In this respect, a split Congress would probably limit the federal government’s ability to roll out new spending.

If the Republicans seize control, they will use their new powers to push back against recent decisions by the Biden administration such as forgiving student debt, and block any future initiatives that involve heavy spending.

With fiscal spending being slashed in an environment of slowing economic activity, the next couple of years might be characterized by slower growth and softer inflation, which argues for the federal funds rate to peak at a lower level.

Market pricing currently suggests the peak will be just under 5%. This might be dialed down a notch if the Democrats lose Congress, igniting a pullback in the mighty US dollar.

Big picture

All told, this election is unlikely to be a game-changer for markets. It might be the trigger for a short-squeeze in stocks and a round of profit-taking in the dollar, but ultimately those are likely to be relief moves, not trend reversals.

Stock markets are still far too ‘expensive’. Valuations haven’t fully adjusted to the rapid spike in real rates yet, and with the economic data pulse slowing, particularly in Europe and China, the risk of an earnings recession is becoming increasingly realistic.

As for the dollar, the dynamics that fueled this spectacular rally are still very much in play. Inflation is scorching-hot and the US labor market remains in good shape, giving the Fed cover to keep raising rates aggressively. Meanwhile, every other major currency is battling its own demons, so there is hardly any competition.

There’s a Fed meeting almost one week ahead of the midterms, which could prove to be equally important for the dollar as investors try to decipher when the central bank might hit the pause button.

Author

Marios graduated from the University of Reading in 2015 with a BSc in Economics and Econometrics. Prior to joining XM as an Investment Analyst in December 2017, he was providing financial analysis, reporting and consulting service