In a blow to modern romance, Parisian authorities took steps to remove the “locks of love” that adorned the railings of the Pont des Arts. Couples had been affixing the locks to the railings of the bridge and throwing the keys into the River Seine to demonstrate their commitment to one another. While each lock was a small symbol, the accumulation eventually placed an unacceptable weight on the bridge’s structure.

A number of American couples presently find themselves trying to unlock themselves from their homes. They are unable to move because of excessive mortgage debt, stagnant home values and tight credit conditions. The shackles they face are limiting U.S. housing and labor market performance.

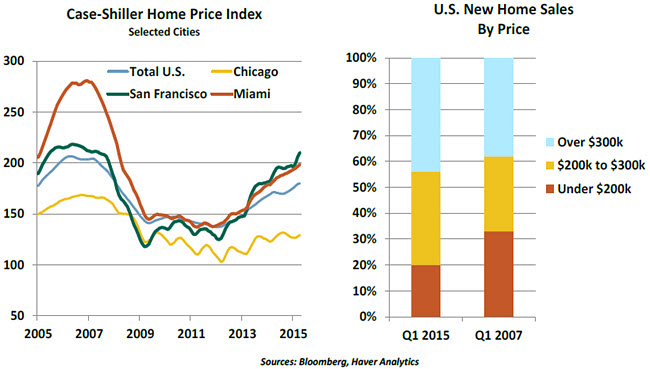

Many sectors of the American economy have recovered nicely and powered past peaks reached before the Global Financial Crisis. But housing is not one of them. As we discussed earlier this year, residential sales and construction are proceeding very modestly. The combination of stricter regulation, aversion to leverage, high levels of student debt and demographic trends has made the going tough.

Progress has been very uneven across markets and price points. Home values in Northern California have surpassed their former high, while Florida property values remain well below their pre-crisis levels. Houses at higher price points have been selling somewhat more successfully than starter homes.

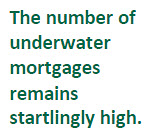

Part of the reason for this latter phenomenon is that the owners of those starter properties are represented disproportionately in the community of families who are underwater on their mortgages (the loan amount exceeds the property value). While the fraction of properties that are in this position is half of what it was three years ago, Zillow estimates that nearly one in six American families still have negative equity in their homes. Almost a million U.S. homeowners still owe double what their property is worth.  In total, one-third of American homeowners have less than 20% equity in their homes. This limits their ability to purchase in new markets where property values might be rising and makes qualifying for a mortgage more challenging.

In total, one-third of American homeowners have less than 20% equity in their homes. This limits their ability to purchase in new markets where property values might be rising and makes qualifying for a mortgage more challenging.

All of this leads residents to avoid listing their homes, which has created a dearth of inventory for first-time homebuyers to consider. The availability of affordable homes has declined further over the past several years as investors purchased units and turned them into rental property. Those rents, especially for detached single-family homes, have been escalating, which puts many of them out of reach for families who are locked in by their mortgages.

Another potential consequence of this situation is reduced labor mobility. Simply put, homeowners who are underwater may hesitate to accept new positions because their finances make it difficult to get out from under their current mortgages. Studies done early in the recovery did not see this as a constraint, but a more-recent analysis from the Census Bureau found some evidence that “house lock” was impairing the labor market’s recovery.

Resolving a debt crisis usually involves concessions from both borrowers and lenders. We discussed this concept a few weeks ago as it applies of the Greek debt crisis, and the same holds true for the American housing market. U.S. homeowners certainly should have known better than to take on more debt than they could handle. But mortgage lenders were aggressively pushing credit at the peak of the last business cycle, employing underwriting tactics and compensation schemes that ultimately proved very damaging.

Programs to assist homeowners in distress proliferated in the years after the crisis. The Making Home Affordable (MHA) effort, which included the Home Affordable Refinancing Program (HARP) and the Home Affordable Modification Program (HAMP), was chartered in 2009. To date, they have arranged 2.5 million permanent mortgage modifications, but Zillow estimates that there are nearly 8 million homeowners who remain underwater. Permanent modifications have been increasing by only 75,000 per quarter recently. Further, the MHA programs focus heavily on changing the terms of existing mortgages, lowering interest rates and extending maturities. A substantial body of work, however, suggests that principal reductions will be needed to allow the market to return to a healthy equilibrium. (This is another parallel with Greece.) In many cases, this will require the cooperation of Freddie Mac and Fannie Mae, who have been reluctant to provide it.

The legal settlements reached by mortgage underwriters with the Justice Department require the establishment of pools earmarked for debt relief. But the process of disbursing these funds has been slow. Principal write-downs can trigger a tax liability, which potential beneficiaries may not be able to afford.

To some, forbearance is a four-letter word. It raises issues of moral hazard in aiding those who are delinquent on their loans while others continue to make their payments on time. And someone (banks or Government Sponsored Agencies) would have to accept some losses.

That perspective is certainly important. But there remains a substantial community of Americans who are shackled by their mortgages. We should continue seeking keys that might provide new openings for them.

Celebrating (?) DFA

The Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA) celebrated its fifth birthday last Tuesday. The occasion prompted reflections that were celebratory (from Dodd and Frank) and excoriating (from House Financial Services Committee Chairman Jeb Hensarling).

It is not yet possible to offer a complete critique of the Act. This is due, in part, to the fact that the Act is not yet complete. According to the law firm of Davis Polk, a little less than two thirds of the rulemaking called for under DFA has been completed. For those elements that have become law, their full effects (both intended and unintended) will take time to assess.

The Act’s supporters point to the substantial increase since 2009 in the amount of bank capital, which serves as a buffer against failure. This week, the Federal Reserve announced that substantial capital surcharges will be required of the country’s largest institutions. With all the recent merger activity in other industries, there hasn’t even been speculation about banking consolidation, partly because regulators are very unlikely to grant the requisite approval for combinations of any scale. “Too Big to Fail” may not have been eradicated, but DFA provides powerful incentives for firms to control their size.

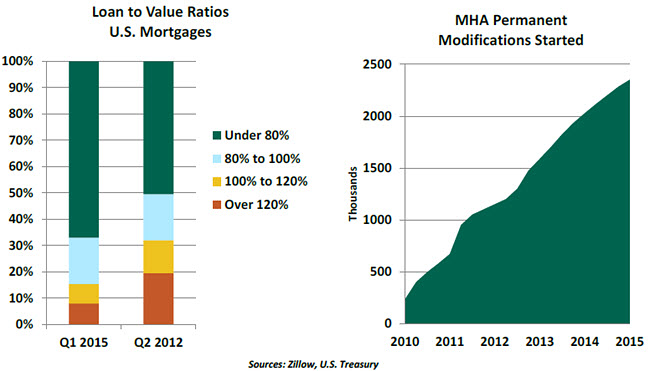

Detractors suggest that post-crisis regulation has crimped credit intermediation and constrained economic growth. On the surface, the data do not seem to support that contention: commercial loans are at a historic high and growing rapidly. Real estate lending has advanced much more modestly, but this represents a return to underwriting sobriety after the mortgage bacchanal of 10 years ago.

Market participants have also expressed concern about the impact of DFA on liquidity in markets. Several aspects of the Act aimed squarely at broker/dealers: the special stress test they must pass annually and Volcker Rule restrictions on proprietary trading, to name two. A series of exaggerated market moves in recent years was blamed on the thinning number and size of trading desks willing to take an opportunistic position in front of a trend.

But one measure of market liquidity finds current conditions slightly better than their long-run average (see chart above). And a recent report on the Treasury market correction of October 15, 2014, places the blame squarely on other features of market infrastructure, including the advance of electronic trading algorithms.

The costs of complying with DFA have been significant. Staffs devoted to tracking the new regulations have expanded substantially. This has hindered bank profitability and discouraged the chartering of new institutions. DFA adherents would certainly note that these costs must be weighed against potential gains in consumer protection and industry safety.

Industrial accidents of significant scale typically incite a wave of re-regulation. And that re-regulation can be taken too far. But it may take a long time for costs and benefits to be fully appreciated and for the political climate to allow for some moderation. We may be debating the Dodd-Frank Act for many anniversaries to come.

Canada Cools

As the U.S. economy leads the Fed to contemplate a rate lift-off, Canada is headed in the opposite direction. The nation’s housing boom has left consumers highly leveraged and cannot be sustained. The energy industry, which accounts for roughly 10% of gross domestic product (GDP) and a quarter of goods exports, has been hit hard.

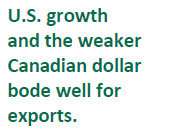

As the petroleum sector slowed, others were supposed to take over. A weaker Canadian dollar would boost non-oil exports to the United States, especially manufactured goods, according to Bank of Canada (BoC) Governor Stephen Poloz. Instead, GDP fell an annualized 0.6% in the first quarter of 2015 and is expected to have contracted again in the second quarter. The disappointment led the BoC to cut rates for the second time this year on July 15 and lower its GDP growth forecast to 1.1% for 2015.

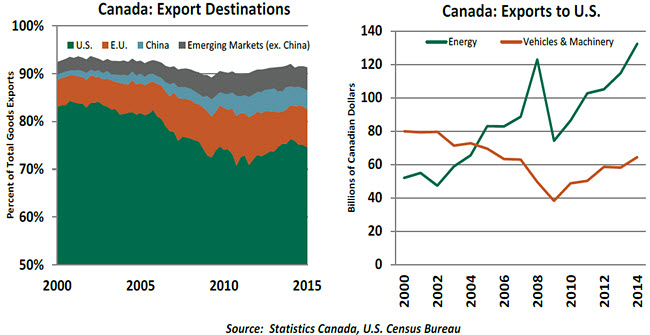

The hiccup is cause for a deeper look into Canada’s trade relationship with the United States, by far the nation’s largest trading partner. Over the past 50 years the U.S. share of Canadian exports averaged 75%, peaking at 84% in 2000. Vehicles and manufactures formed the most- important part of trade during the past century. In the ‘90s, vehicle and machinery manufacturers represented 24% of U.S.-destined exports, while energy was just 11%.

However, the past decade or so brought an important shift in the trade relationship. First, rising oil prices and new technology made extracting from Canada’s prairie oil sands both possible and profitable. At the same time, manufacturers were hit hard as production moved overseas, to China and Mexico. In 2005, energy replaced vehicle and machinery manufacturers as the economy’s key export sector and accounted for 33% of exports by 2014, compared to 16% for vehicles and machinery.

However, the past decade or so brought an important shift in the trade relationship. First, rising oil prices and new technology made extracting from Canada’s prairie oil sands both possible and profitable. At the same time, manufacturers were hit hard as production moved overseas, to China and Mexico. In 2005, energy replaced vehicle and machinery manufacturers as the economy’s key export sector and accounted for 33% of exports by 2014, compared to 16% for vehicles and machinery.

Canada’s exports also shifted away from its neighbor to the south, due to the U. S. recession and the rise of emerging markets. By 2010, the U.S. share of exports fell from its 2000 peak of 84% to 71%. China and other emerging markets stepped in to purchase metal and agricultural commodities from the resource-rich economy.

Considering both domestic and global frailties, a U.S. export-led recovery remains Canada’s best hope. U.S. economic momentum and a weaker Canadian dollar bode well. But as recent weakness has shown, Canada cannot wait much longer.

Recommended Content

Editors’ Picks

EUR/USD clings to gains above 1.0750 after US data

EUR/USD manages to hold in positive territory above 1.0750 despite retreating from the fresh multi-week high it set above 1.0800 earlier in the day. The US Dollar struggles to find demand following the weaker-than-expected NFP data.

GBP/USD declines below 1.2550 following NFP-inspired upsurge

GBP/USD struggles to preserve its bullish momentum and trades below 1.2550 in the American session. Earlier in the day, the disappointing April jobs report from the US triggered a USD selloff and allowed the pair to reach multi-week highs above 1.2600.

Gold struggles to hold above $2,300 despite falling US yields

Gold stays on the back foot below $2,300 in the American session on Friday. The benchmark 10-year US Treasury bond yield stays in negative territory below 4.6% after weak US data but the improving risk mood doesn't allow XAU/USD to gain traction.

Bitcoin Weekly Forecast: Should you buy BTC here? Premium

Bitcoin (BTC) price shows signs of a potential reversal but lacks confirmation, which has divided the investor community into two – those who are buying the dips and those who are expecting a further correction.

Week ahead – BoE and RBA decisions headline a calm week

Bank of England meets on Thursday, unlikely to signal rate cuts. Reserve Bank of Australia could maintain a higher-for-longer stance. Elsewhere, Bank of Japan releases summary of opinions.