In 2010, the United Kingdom emerged from a general election with a hung parliament, the first in 36 years. The negotiations that followed led to a coalition between the Conservative and Liberal Democrat parties which, despite initial doubts, endured a full term.

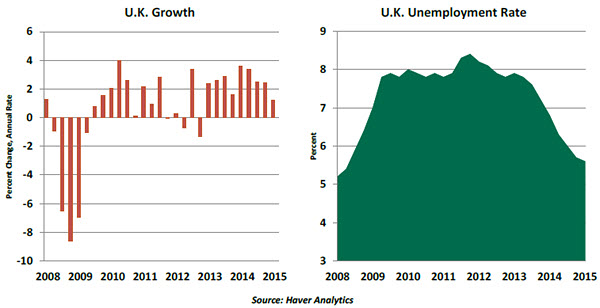

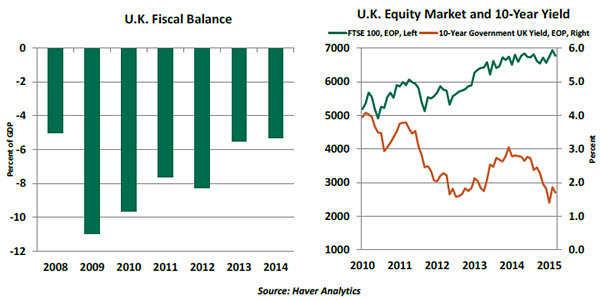

As voters prepare for the balloting next week, the outcome is more uncertain than five years ago. Attention has concentrated on predicting different combinations of parliamentary seat victories and who would work with whom. The focus has drifted from the economy and policy, which we explore here. As his party is keen to remind us, under Prime Minister David Cameron's tenure, the level of public borrowing in Britain has fallen to 5.0% of gross domestic product (GDP) today from an unsustainable high of 10.2% of GDP in 2009-10. During that interval, the economy performed well. GDP growth for 2014 was recently revised upward to 2.8%, unemployment is down at 5.6%, the fiscal deficit has been halved and confidence among consumers is the highest it’s been for over a decade.

The U.K.'s fiscal position is an important issue and one that features heavily in the plans of the three major parties. The Conservatives have been clear that they have a "long-term economic plan" and have pledged to continue public spending cuts to achieve their goals. They want to balance the current budget by 2017-18 (i.e., government revenue covering all expenditures except investments, adjusted for the economic cycle) and have an outright surplus by the following year. They argue that this will leave the United Kingdom in a better position to withstand future global shocks.

In their manifesto, they lay out a deficit reduction plan involving a further £30 billion in fiscal consolidation over the next two years, with £12 billion coming from the welfare budget, £5 billion from tackling tax avoidance and £13 billion from departmental savings, although those departments have not been named.

Labour, on the other hand, have been vaguer with their fiscal plans. They will cut the budget deficit every year but have only promised a surplus on the current budget "as soon as possible," implying a less-austere approach to managing the economy. Contrary to the Tories, Ed Miliband's party is likely to raise taxes, increasing the top rate to 50% from 45%, introducing a "Mansion Tax" on properties worth more than £2 million and reversing cuts in corporation tax.

The Liberal Democrats share the goal of arriving at a balanced current budget by 2017-18 and want to have debt falling as a proportion of national income every year from 2017-18.

The impact of these policies is debatable. Higher public spending and reduced cuts outlined by Labour and the Liberal Democrats could potentially increase growth. A recent study by Oxford Economics suggests that the Liberal Democrats' plans, if fully implemented and under certain assumptions, would result in the highest level of growth, followed by Labour and then the Conservatives. But their results suggest the differences would be modest.

The impact of these policies is debatable. Higher public spending and reduced cuts outlined by Labour and the Liberal Democrats could potentially increase growth. A recent study by Oxford Economics suggests that the Liberal Democrats' plans, if fully implemented and under certain assumptions, would result in the highest level of growth, followed by Labour and then the Conservatives. But their results suggest the differences would be modest.

Higher levels of economic activity under Labour, coupled with plans to increase the minimum wage, could lead to a long-awaited boost in earnings and spark inflation, meaning policy rate tightening could be quicker than it would be under David Cameron. However, Labour's plans imply a slower pace of deficit reduction and higher debt; according to estimates from the Institute of Fiscal Studies (IFS), debt would be £90 billion higher by 2019-20 under a Labour government compared to a Conservative government. That is a sizeable amount and increases the potential for higher interest payments and higher future taxes to fund them.

Market and business reaction has thus far been varied. The FTSE 100 breached the 7,000 mark for the first time in March and is up just over 7.0% year-to-date. Government borrowing costs remain low, with 10-year gilts yielding around 1.7%. Both point to markets shrugging off uncertainty.

However, there are signs that business leaders are beginning to worry. In Deloitte’s first 2015 quarterly survey of chief financial officers, the number one risk managers cite is the election and risk of policy change and uncertainty. Risk appetite among those surveyed is falling, and they report focusing on defensive rather than expansionary strategies. If a strong government that can instill confidence cannot be agreed post-vote this worry will continue, delaying investment plans.

Elsewhere, the Scottish National Party (SNP) and UK Independence Party (UKIP) are playing a significant role. Both have nationalist views – the SNP wants an independent Scotland and UKIP wants out of the European Union (EU). The SNP is likely to snatch the majority of Scottish constituencies from Labour, whereas UKIP is only set to win a handful. But the percentage swing from the Tories to UKIP has hurt Cameron's prospects of re-entering Downing Street and forced him to promise a referendum on EU membership.

Elsewhere, the Scottish National Party (SNP) and UK Independence Party (UKIP) are playing a significant role. Both have nationalist views – the SNP wants an independent Scotland and UKIP wants out of the European Union (EU). The SNP is likely to snatch the majority of Scottish constituencies from Labour, whereas UKIP is only set to win a handful. But the percentage swing from the Tories to UKIP has hurt Cameron's prospects of re-entering Downing Street and forced him to promise a referendum on EU membership.

The long-term impact these parties are having on the political makeup is important. The system appears fractured, and calls for power devolution from Westminster are spreading to regions outside Scottish borders. And the prospect that the country might possibly leave the European Union is tremendously worrisome to British markets and businesses.

Managing these cross-currents, while reassuring global investors, will be a challenge the next government must face. Expect at least some market volatility around voting day, the majority of which should settle down quickly once an agreement materializes. We will report back once the outcome becomes clearer.

Slow Off the Mark

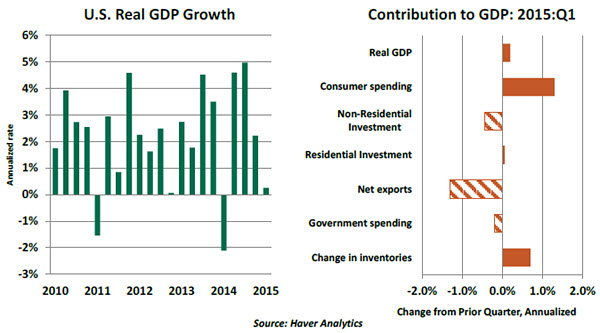

The U.S. economy barely advanced in the first quarter this year after three quarters of very solid growth. The key question is whether the weakness is temporary or represents the beginning of a new slowing trend. Details of the advance GDP report suggest that the winter drag should be a fleeting experience.

Bad weather hindered economic activity during the first quarters of both 2014 and 2015. But there was much more at play this time around.

A widening of the U.S. trade deficit to $521 billion from $471 billion on an annualized basis reflects a large drop in exports that was partly due to the dockworkers strike on the West Coast. With that strike settled, goods are flowing freely once again and should lead exports to increase more normally in the second quarter.

But the poor trade results are also partly due to a strong U.S. dollar, which is a more-lasting force. The dollar's value has stabilized over the past two months, but its gains since last summer will continue to weigh modestly on growth.

The sharp drop in oil prices during the second half of 2014 led to a nearly 50% plunge in oil industry investment that dragged down real GDP growth by an estimated 0.75 percentage point in the first quarter. Since the beginning of this year, oil prices have stabilized; and so the contribution of this sector to GDP growth should be less negative in the quarters ahead.

Consumer spending moved up at an annual rate of 1.8% in the first quarter, which is very modest when compared with the strength of the prior three quarters. But we expect consumption to increase more rapidly in the months ahead. Weather most likely held back auto sales during January and February, but activity recovered powerfully as the climate became more temperate. In addition, the trend of real disposable income shows a noticeable surge. This, combined with savings from lower gasoline prices and favorable household net worth, suggests a solid outlook for consumer spending.

Consumer spending moved up at an annual rate of 1.8% in the first quarter, which is very modest when compared with the strength of the prior three quarters. But we expect consumption to increase more rapidly in the months ahead. Weather most likely held back auto sales during January and February, but activity recovered powerfully as the climate became more temperate. In addition, the trend of real disposable income shows a noticeable surge. This, combined with savings from lower gasoline prices and favorable household net worth, suggests a solid outlook for consumer spending.

There will be those who will take the first-quarter GDP report and predict a renewed bout of economic stagnation. But we think we are more likely to get a repeat of last year's experience, when an artificially soft first quarter gave way to renewed vigor.

Waiting for Liftoff

The U.S. economy entered 2015 on a very strong note, in the wake of impressive job growth and solid consumer spending in the latter portion 2014. In March, the Federal Reserve placed all meetings, starting from June, on the table for a rate hike. But in the wake of incoming data, tightening seems to be off the table for a while.

This week's Fed meeting concluded without a significant change in policy language. While the language acknowledged the soft performance in the first quarter ("growth slowed in the winter months," "job gains moderated," and "business investment…softened") the group also affirmed more positive forward thinking ("Although growth…slowed during the first quarter, the Committee continues to expect that…economic activity will expand at a moderate pace"). Risks to the outlook are still seen as "nearly balanced."

Wednesday's statement from the Federal Open Market Committee was the first in a very long time that did not include some "calendar-based" guidance on monetary policy. There was no mention of specific months or considerable periods. From here forward, decisions will be "data-dependent."

Some have packaged this as some kind of paradigm shift, but the reality is that the Fed has always been data-dependent. Progress toward their dual mandate will determine both the timing and trajectory of any move to tighten credit.

The first side of this mandate is full employment. While the March payroll number was a disappointment, it stands in contrast to very strong readings for the 12 months prior. Jobless claims remain very low, and the number of workers on disability rolls has been declining for six months in a row.

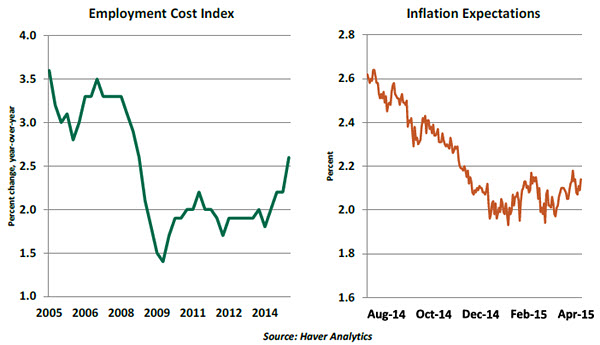

The Fed has identified employee compensation as a lingering sign that labor markets still have considerable slack. Hourly wage growth has been stuck at 2% for several years now. But the first quarter Employment Compensation Index showed accelerated gains in both wages and total compensation. This suggests that full employment may be nearing.

The Fed's other mandate is the achievement of 2% inflation. Actual performance has fallen short of this objective for 35 consecutive months. But with energy prices and the dollar stabilizing, the downward pressure from these two ingredients on the price level has started to diminish. And inflation expectations, shown above, are beginning to stabilize and advance after last year's retreat.

The Fed's other mandate is the achievement of 2% inflation. Actual performance has fallen short of this objective for 35 consecutive months. But with energy prices and the dollar stabilizing, the downward pressure from these two ingredients on the price level has started to diminish. And inflation expectations, shown above, are beginning to stabilize and advance after last year's retreat.

Monitoring developments on these two fronts will provide the keys to when the Fed might move, and how quickly. On the basis of the soft first-quarter GDP report, markets have pushed the first interest rate increase from the Fed out into 2016.

While we're giving the matter an updated look, we are likely to affirm our expectation of change before the end of this year. Like the Fed, we are looking beyond the first quarter to a more positive future. Rate increases may be back on the table sooner than many suspect.

Recommended Content

Editors’ Picks

EUR/USD clings to gains above 1.0750 after US data

EUR/USD manages to hold in positive territory above 1.0750 despite retreating from the fresh multi-week high it set above 1.0800 earlier in the day. The US Dollar struggles to find demand following the weaker-than-expected NFP data.

GBP/USD declines below 1.2550 following NFP-inspired upsurge

GBP/USD struggles to preserve its bullish momentum and trades below 1.2550 in the American session. Earlier in the day, the disappointing April jobs report from the US triggered a USD selloff and allowed the pair to reach multi-week highs above 1.2600.

Gold struggles to hold above $2,300 despite falling US yields

Gold stays on the back foot below $2,300 in the American session on Friday. The benchmark 10-year US Treasury bond yield stays in negative territory below 4.6% after weak US data but the improving risk mood doesn't allow XAU/USD to gain traction.

Bitcoin Weekly Forecast: Should you buy BTC here? Premium

Bitcoin (BTC) price shows signs of a potential reversal but lacks confirmation, which has divided the investor community into two – those who are buying the dips and those who are expecting a further correction.

Week ahead – BoE and RBA decisions headline a calm week

Bank of England meets on Thursday, unlikely to signal rate cuts. Reserve Bank of Australia could maintain a higher-for-longer stance. Elsewhere, Bank of Japan releases summary of opinions.