Week ahead: US GDP and PCE numbers take centre stage

The path for future interest rates in the US remains uncertain, with some Fed officials even talking about the possibility of rate hikes if inflation continues to increase. From six rate cuts to less than two (-39bps), the hawkish repricing in the swaps market for the Fed funds target rate this year has reinforced a dollar bid. According to market pricing, September’s policy-setting meeting is eyed for the first -25bp cut, though November’s meeting is also on the table. Similarly, investors have continued to pare back rate-cut bets for other G10 central banks.

Tensions in the Middle East also remain at the forefront of markets. Escalation between Iran and Israel has thankfully been limited following attacks from both sides earlier this month. Given Iran’s contribution to oil production (it provides approximately 3.3% of the world’s oil supply), further escalation may fuel a rise in oil prices (as well as gold prices and the US dollar [USD] on safe-haven appeal). A considerable bid in oil could also have wider-reaching implications that fuel inflationary pressures and perhaps lead to interest rates remaining higher for longer.

Therefore, the Research Team will continue to monitor the 2-year and 10-year UST yields for signs of softness, the US Dollar Index, and energy markets, specifically oil and gold.

This week in a nutshell

On the data front, the headline events are the US GDP Advance estimate on Thursday and the PCE Price Index on Friday. Also out of the US, albeit considered 2nd-tier data, durable goods orders is scheduled to hit the wires on Wednesday, along with housing metrics: New Home Sales on Tuesday and Pending Home Sales on Thursday.

We also have April’s S&P Global PMIs to look forward to for Europe, the UK, and the US on Tuesday. Additionally, Asia Pac markets will be closely watching CPI inflation data from Australia on Wednesday and the Bank of Japan (BoJ) rate announcement on Friday.

On the earnings front, equity markets welcome earnings data from big tech companies such as Tesla (TSLA), Microsoft (MSFT), Meta (META), and Google (GOOG) starting on Tuesday. Major US equity markets ended another session in the red last week; the S&P 500 market average slumped -3.0% (the largest one-week decline since March 2023), with the index down -5.5% MTD.

US GDP poised for an upside surprise?

The first estimate for US GDP for Q1 2024 is anticipated to reveal cooling economic activity. Expectations heading into the event indicate real GDP growth will slow to an annualised rate of just north of 2.0%, down from the annualised rate of 3.4% in Q4 2023 and 4.9% in Q3 2023. Interestingly, though, the Atlanta GDPNow model estimates real GDP growth in Q1 of 2024 to be 2.9%, presenting the possibility for a beat in data this week. An upside surprise here would likely bolster demand for the USD and could also prompt further hawkish repricing in rates markets (the US Dollar Index is up +1.5% MTD, on track to record a fourth straight monthly gain).

The PCE price index

The headline Personal Consumption Expenditure Price Index (PCE) is expected to have risen +0.3% in the month of March, matching the previous month’s report. Similarly, Core PCE data between February and March is also expected to have risen by +0.3% (matching prior data). Year on year, headline PCE data is anticipated to have increased to +2.6%, up from +2.5%, while the Core measure is forecast to have slowed to +2.7% from +2.8%.

With CPI inflation data stalling and continuing to print above economists’ estimates for the past four months, in addition to some Fed officials highlighting the scope to increase the Fed funds rate if inflationary pressures persist, the PCE release will be widely watched this week. An upside surprise in the data is likely to fuel demand for the USD on the back of rates potentially remaining restrictive for longer. This could also fuel further downside in stocks and bonds, pushing UST yields higher. Conversely, a miss on the data would likely have the opposite effect: a dovish repricing in rates.

BoJ: Attention on rate statement and outlook report

Following the Bank of Japan (BoJ) raising its short-term Policy Rate by 10bps at its last meeting to 0.0% and ending yield curve control (YCC), market pricing suggests policy will be maintained at this week’s meeting. Consequently, the focus is on the accompanying rate statement for any language change and, of course, the quarterly report detailing the central bank’s outlook on economic activity and inflation.

Will the BoJ intervene? The beleaguered Japanese yen (JPY) ended the week refreshing multi-decade lows against the US Dollar, recently prompting warnings from top officials that they would ‘step in’, similar to late 2022. However, despite comments triggering a fleeting JPY bid, it has done little to stem its decline. As of now, signs of intervention have been limited, but this certainly weighs on the minds of traders and investors as the USD/JPY exchange rate continues to find acceptance in higher terrain. Technicals suggest the currency pair could be headed as far north as ¥160 – levels not seen since the 1990s!

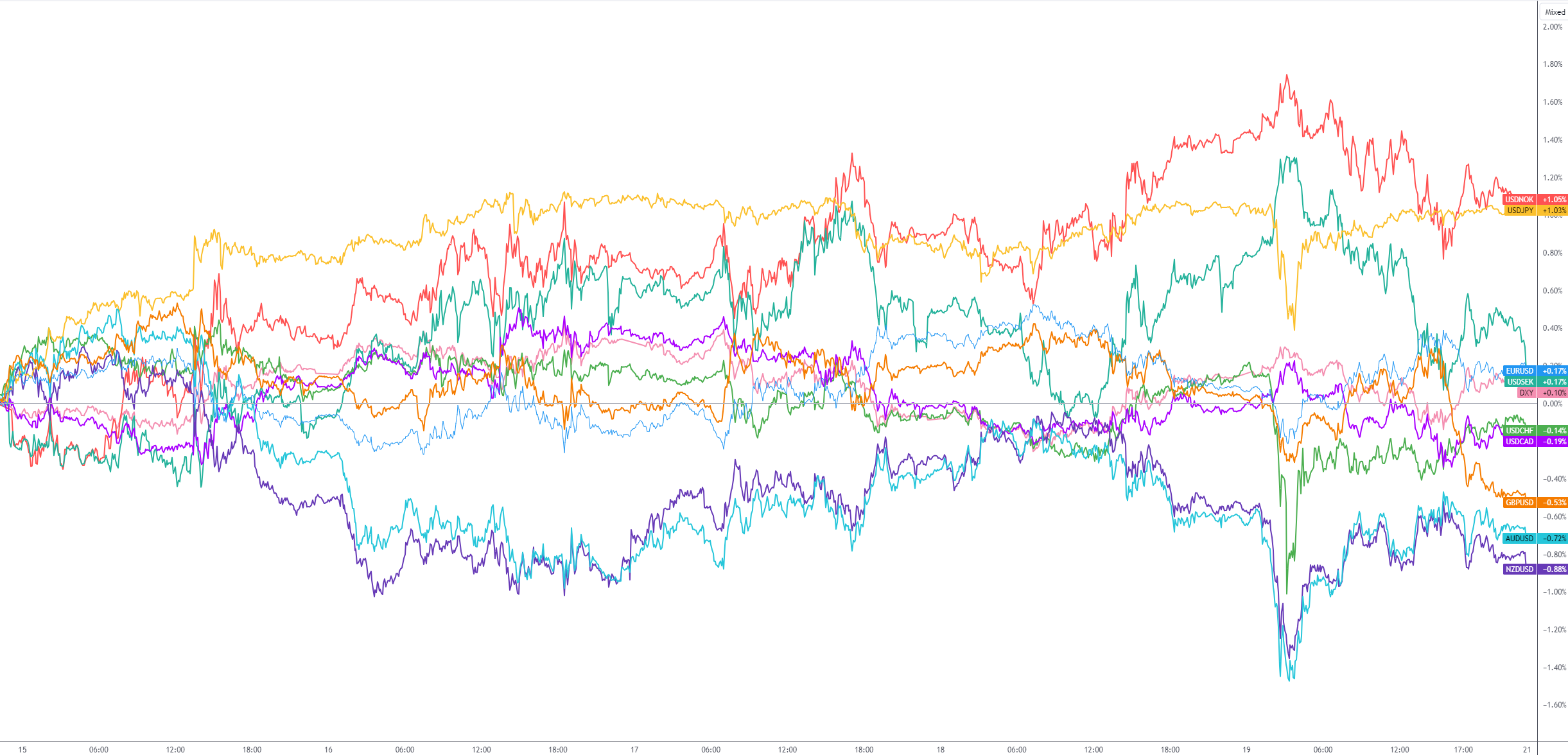

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,