USD/JPY Forecast: Risk, if it's not getting worse, can it get better?

- USD/JPY falls as funding rush risk positioning ebbs.

- Equity recovery may have taken edge from market crisis.

- US stimulus and support package restores some confidence in economy.

The dollar rally faded this week as the panicked funding rush abated, the return on the 3-month US Treasury dipped below zero for the first time in history and the Federal Reserve’s purchase program lowered rates across the yield curve.

Dollar yen opened the week at 110.92 and for three days moved not at all, closing one point lower each day from Monday’s finish at 111.23. The passage by the Senate on Wednesday evening of the $2.2 billion stimulus and relief package after days of wrangling set the stage for Thursday’s decline to a 109.62 close and Friday’s continuation to 108.00.

A powerful equity rally that started on Tuesday in anticipation the Congressional rescue package had restored 21.3% to the Dow by the close on Thursday raising the 30 stock index from 18,591 at Monday’s finish to 22,252 three days later. Friday’s 800 point drop in the average did not return risk-off sentiment to the dollar yen which finished at 108.03.

Federal Reserve liabilities, bolstered by the central bank’s newly revivified asset purchase program, are now more than $5 trillion, above their level at the height of the financial crisis. Treasury rates have fallen across the term spectrum with the yield on the 3-month bill dipping below zero for the first time in history in the latter part of the week but regaining the positive on Friday.

Friday’s close in the USD/JPY was at 107.87 just above the 107.70 support line which held from mid-October until the Coronavirus inspired rush to Treasuries began in the first week of this month.

Dollar yen has been subject to flow and risk based changes of unusual rapidity over the past five weeks all related to the progress and perception of the Coronavirus pandemic. When the economic risks associated with the virus stabilize or become quantified, which is mostly the same thing, the safety premium will continue to leak from the US dollar. We have seen the beginnings of that recalculation this week.

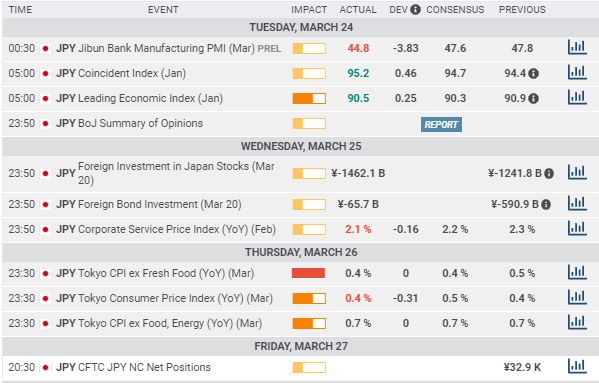

Japanese statistics March 23-27

Tuesday

The Jibun Bank manufacturing PMI preliminary figure for March came in at 44.8, below the median consensus for 47.6 and February’s 47.8 score

The Coincident index for the Japanese economy in January was 95.2 a bit stronger than the 94.7 estimate and December’s negatively revised 94.4 result.

Thursday

Tokyo CPI for March was almost as predicted: 0.4% on the year vs a 0.5% forecast and 0.4% in February; Core CPI 0.7% equal to the prediction and the February rate.

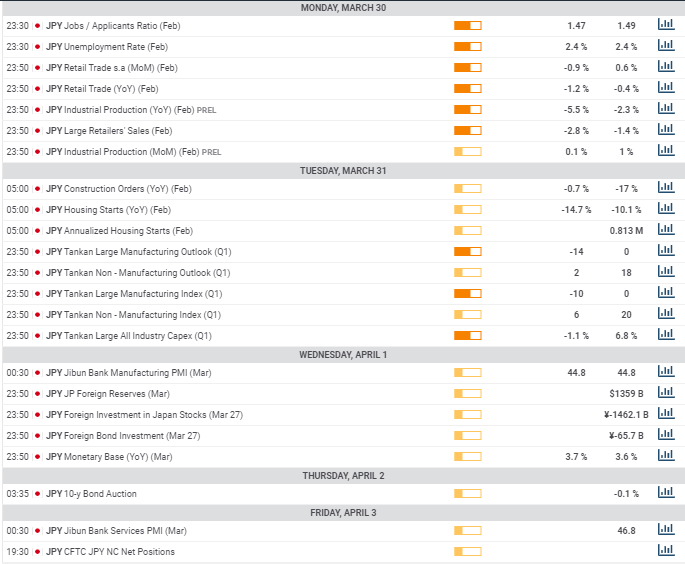

Japanese statistics March 30-April 3

Tuesday

February’s unemployment rate is expected to be unchanged at 2.4%. It has been between 2.2% and 2.5% since January 2018

Retail trade on the month in February will drop 0.9% after January’s 0.6% gain, annual trade will fall 1.2% following a 0.4% decrease in January. It has fallen for four months.

Industrial production for last month is predicted to rise 0.1% after January’s 1% increase. It would be the third gain in a row after -4.5% in October and -1% in November.

Wednesday

The Tankan Survey from the Bank of Japan for the first quarter is expected to deteriorate in outlook across all categories: large manufacturers’ outlook -14 from 0 in the fourth quarter; large manufacturing index 6 from 20; non-manufacturing outlook 2 from 18; non-manufacturing index 6 from 20; all large industry capex -1.1% from 6.8%.

Japan statistics conclusion

Two number for March in particular spell trouble for the Japanese manufacturing sector. The Jibun PMI at 44.8 was the lowest reading since the first half of 2009 during the recovery from the financial crisis. A revised figure will be released on April 3 and is expected to be unchanged at 44.48.

The Tankan survey from the BOJ is one of the most widely followed industry gauges in Japan. If the predictions are accurate both the large manufacturing index and outlook would be the lowest since the recovery from the financial crisis in 2009 and 2010.

More information from March will be available in the second week of April with the Eco Watchers Survey, PPI, consumer confidence, bank lending and machine tool orders.

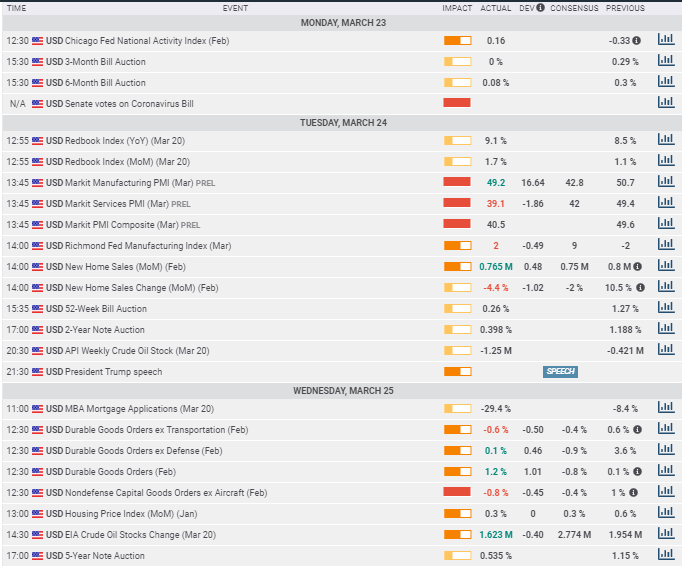

US statistics March 23-27

Tuesday

The Redbook index of year-over-year same store sales for the March 20 week at 1.7% on the month and 9.1% on the year were both better than the prior month, 1.1% and 8.5% respectively. They indicate for the stores polled, which represent 80% of the Department of Commerce’s retail sales figures, no drop in sales as yet from the public health crisis.

The Richmond Fed Manufacturing Index for March rose to 2 from -2 in February missing the 9 forecast.

Wednesday

Durable goods orders in February were stronger than forecast in the headline 1.2% vs -0.8% and in the ex-defense category 0.1% vs -0.9% and weaker ex-transport -0.6% against -0.4% and in the business capital goods group -0.8% vs -0.4%.

Fourth quarter GDP was unchanged as anticipated at 2.1%.

The Kansas City Fed Manufacturing Activity Index was much poorer than predicted at -18 on an estimate for 2 and the February score of 8. It was the lowest reading since June 2015.

Initial jobless claims broke all records for the week of March 20 as 3.283 million Americans filed for unemployment benefits. This was more than four times the previous high from 1982 of 695,000.

The Michigan Consumer Sentiment Survey for March dropped to 89.1 on revision from the 90 preliminary score and 101 in February.

US statistics March 30-April 3

Monday

The Dallas Fed Manufacturing Business Index is forecast to climb to 6.2 in March from 1.2 the prior month.

Tuesday

The Redbook Index of same store sales for the week of March 27. The previous week had increases of 1.7% on the month and 9.1% on the year.

Conference Board Consumer Confidence is predicted to drop to 112.00 in March from 130.00 in February.

Wednesday

ADP employment change for March is projected to be down 150,000 after adding 183,000 jobs in February. It would be the first loss since October 2010.

The ISM manufacturing Index for March is forecast to be lower in the overall at 44.3 from 50.1, lower in employment 45.4 from 46.9 and higher in the new orders index to 50.2 from 49.8.

IHS Markit’s manufacturing index for March is predicted to be unchanged at 49.2 after revision.

Thursday

Challenger job cuts for March which tracks announced corporate layoffs is issued at 7:30 am EDT. They were 56,660 in February and 67,735 in January

Initial jobless claims for the week of March 27 are projected to be 3 million after last week’s record shattering total of 3.283 million crisis forced filings.

Friday

Non-farm payrolls are forecast to shed 123,000 positions for the first negative month in almost a decade and the unemployment rate is expected to jump to 4% from 3.5%. Average hour’s earnings will fall on the month to 0.2% from 0.3% and to be stable at 3% on the year.

The ISM Non-Manufacturing Purchasing Managers’ Index for March will fall modestly to 55.1 from 57.3, the new orders index will drop to 56.6 from 63.1 and the employment index will slip to 53.7 from 55.6.

US statistics conclusion

The past week’s economic numbers produced their share of horrors led by the astronomical initial jobless claims of 3.283 million which is expected to repeat this coming Thursday.

The other March numbers were mixed. The Rebook Index of retail sales rose in the March 20 week as did the Richmond Fed Manufacturing Index, though missing forecast and the Kansas City equivalent fell far more than expected. The Michigan Consumer Sentiment Index fell slightly on revision.

Jobless claims produced little effect in the markets as it had been widely anticipated and though a record was no surprise.

The coming week should produce more evidence of what the viral shutdowns have inflicted on the American economy. Initial claims, payrolls, unemployment and purchasing managers’ indexes in manufacturing and services are bound to be unpleasant but at this point markets have run so far ahead with their negative speculation and positioning that anything less than the unexpected disaster might buoy market attitudes and bring a tinge of risk sentiment back to trading.

USD/JPY technical outlook

The near mirror reversal of the USD/JPY over the past month has brought the RSI neatly back to the uncommitted 50 line after reaching overbought on February 19, 20 and 21 and oversold on March 6 and 7.

The same indecision is pictured in the moving averages with the longer two flat, at 109.00 in the 100-day and the 200-day at 108.30. The 21-day crossed both to the downside this month the 100 on March 9 and the 200 on 13. After a brief five days of relative stability the 21-day turned down again on Thursday and Friday's following the dollar yen's 3% fall at the end of the week.

Resistance:108.40, 109.00 109.60

Support: 107.70, 107.25, 106.50

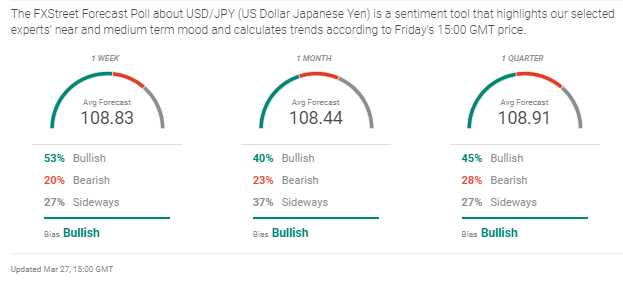

USD/JPY sentiment poll

This weeks sentiment poll is an excellent example of the reversion-to-mean tendency of most forecasts and many indicators.

The USD/JPY close on March 20, last Friday at 110.92 completed a two week 7.6% run higher from the close on March 9 of 103.08. Sentiment greeted this move with universal bearishness: 20% to 50% in the one week; 12% to 58% in the one month; 20% to 77% in the one quarter.

The 2.7% fall this week in the USD/JPY has reversed that equation. The one week is now 53% to 20% bullish, the one month is 40% to 23% and the one quarter is 45% to 28%. In normal conditions with speculative trading profits the primary market concern reversion is a useful concept. In fundamental and risk driven markets it can lead one astray from true motivation.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.