USD/CAD Weekly Forecast: Will the Fed reverse the trend?

- Dollar Canada touches four-month low on Thursday at 1.2288.

- WTI sets a new seven-year high at $83.92 and close at $83.71.

- BOC expected to deliver another round of tapering.

- FXStreet Forecast Poll sees a short-term revival in the downtrend.

The long string of Canadian dollar gains received a check this week as the USD/CAD closed just points from Monday’s open despite crude oil’s seven-year high and a prospective reduction in the Bank of Canada’s bond purchases at its forthcoming Wednesday meeting.

Since finishing at 1.2763 on Friday, September 17, the USD/CAD has lost ground for five straight weeks, shedding 3.1% in total. This week’s loss of four points was the smallest in that run, though just barely, the pair lost six points in the five session's ending on October 1.

Surging crude prices have been a heady propellant for the resource-heavy Canadian economy and its currency.

In the five-weeks mentioned above West Texas Intermediate (WTI) has climbed 16.5%. Its close on Friday at $83.71 was a fresh seven-year high, one of many in the past year. Since the November 2, 2020 open at $35.90, WTI has soared 133.2%. It’s most recent surge from $61.82 on August, 23 to Friday’s finish, added 35.4%.

The Bank of Canada (BOC) is expected to deliver another $C1 billion cut in its bond purchases leaving the program at one-quarter of its original $C4 billion. The end of the BOC program is priced into the USD/CAD given its sharp gains in the past month.

After six months of preparation the US Federal Reserve is widely forecast to announce the beginning of its own taper program in two weeks at the November 3 meeting. Though the decision is anticipated, the amounts and scheduling are uncertain, leaving considerable room for movement in the US dollar. Federal Reserve officials have been unusually attentive to inflation in their recent comments, raising the possibility that the reduction might be more than than the $5 to 10 billion of recent speculation.

Canadian Retail Sales in August and consumer prices in September were a bit stronger than predicted but as a BOC bond program was already expected, they had no market impact.

Statistics were relatively spare in the US in the past week. Industrial Production in the US sank 1.3% in September, far worse than the 0.2% prediction and Capacity Utilizations dropped to 75.2% from 76.2%. These coincide with the Atlanta Fed’s declining estimate for third quarter GDP now at 0.5%. It is down from over 6% in early August.

The US housing market remained effervescent, with Existing Home Sales, representing 90% of activity, jumping 7%. It is possible the threat of rising mortgage rates has motivated buyers to complete their purchases.

Treasury rates in the US and Canada continued to rise. The US 10-year Treasury note added 6 basis points to 1.636% this week, bringing the yield increase since the September 22 Federal Reserve meeting to 31 points.

The Canadian equivalent bond yield also climbed 6 points to 1.648%. In the September 22 to the present period it has gained 42 points.

USD/CAD outlook

Commodity prices, particularly oil, and the highest inflation since 2003 can be expected to provide support for the loonie dollar in the week ahead. Canada’s employment picture is considerably brighter than in the US with all pandemic job losses recovered and few labor shortages.

The BOC has been more aggressive than the Fed in curtailing its bond program and in its rhetoric on inflation. That has built in expectations for a faster series of rate hikes, as many as three by year end.

If the BOC maintains its aggressive stance on Wednesday, the loonie will reassert its advantage over the US dollar but the downward trend is weakening.

American data is expected to support the Federal Reserve case for commencing the bond taper. The Personal Consumption Expenditure Price Index for September is forecast to jump to 4.7%, the core rate to 3.6%, both records if correct. The consensus forecast for the first reading on third quarter GDP is 5.4%. The discrepancy to the Atlanta Fed GDPNow projection of 0.5% is notable and unusual. It would probably take a result near the Atlanta estimate for the Fed to delay its taper announcement.

The wild card is the following week’s decision from the Federal Reserve. The potential for a more assertive inflation policy from the Fed has been growing for several weeks and the possibility should keep USD/CAD losses in check until the Federal Open Market Committee (FOMC) renders its decision.

The bias for the USD/CAD is neutral.

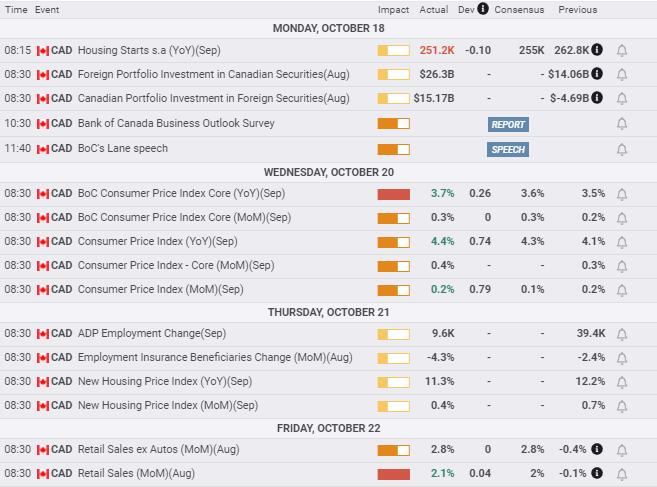

Canada statistics October 18–October 22

FXStreet

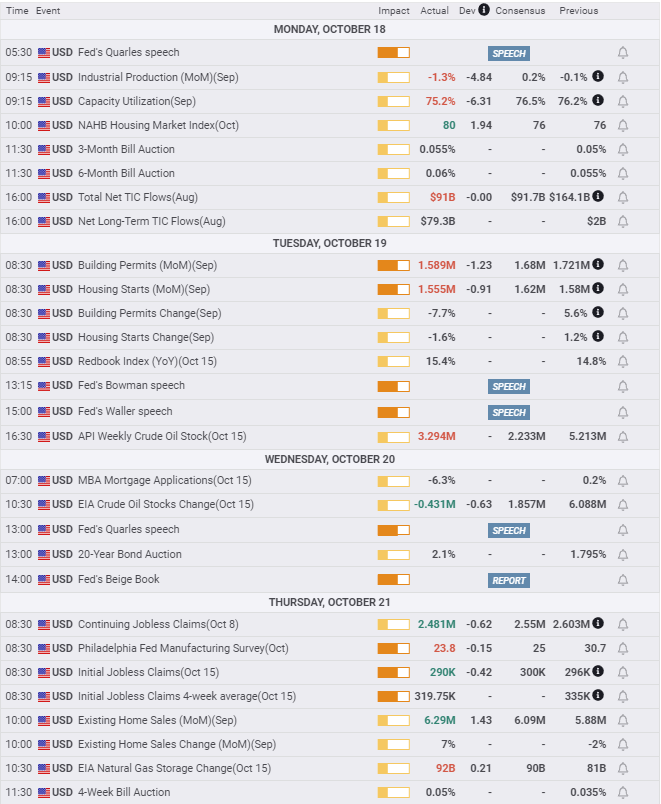

US statistics October 18–October 22

FXStreet

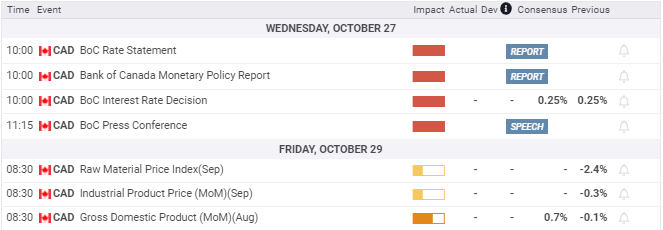

Canada statistics October 25–October 29

FXStreet

US statistics October 25–October 29

USD/CAD technical outlook

The downward pressure on the USD/CAD has eased somewhat with the MACD (Moving Average Convergence Divergence) and the Relative Strength Index (RSI) pulling back from their extremes of the prior week. The RSI dipped into overbought territory on Tuesday and Wednesday but exited on Thursday. Both averages retained their sell status for the USD/CAD. True Range momentum was diminished with the smaller daily ranges compared to the drama of the previous two weeks.

The 21-day moving average (MA) crossed the 50-day MA on October 15, presaging the steep USD/CAD decreases of the next six sessions. On Friday the 21-day MA decline reached the 100-day MA and is less than 20 points from the 200-day MA. These crosses are classic signs of an accelerating descent.

Resistance: 1.2400, 1.2440, 1.2500 (200-day MA), 1.2515 (21-day MA,100-day MA)

Support: 1.2320, 1.2270, 1.2180, 1.2135

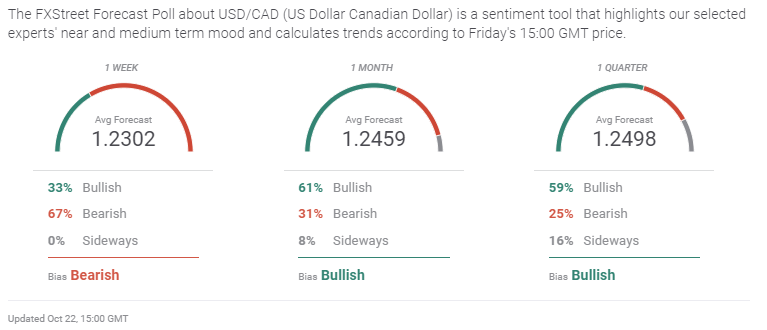

FXStreet Forecast Poll

The FXStreet Forecast Poll foresees an initial failure at resistance followed by a trend reversal.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.