US Third Quarter GDP Preview: How slow is slow?

- Economic growth predicted to edge lower in the third quarter.

- Consumer spending has slipped despite a strong labor market.

- Business spending remains moribund awaiting China and Brexit.

The Bureau of Economic Analysis, a part of the Commerce Department will release its preliminary estimate for annualized gross domestic product (GDP) in the third quarter on Wednesday October 30th at 12:30 GMT, 8:30 EDT.

Forecast

Annualized GDP is predicted to slow to 1.7% in the third quarter from 2.0% in the second quarter and 3.1% in the first. The range of estimates in the Reuters Survey is 1.0% to 2.2%.

Consumer spending, confidence and jobs

Consumer spending in the third quarter declined from the prior three months but remained positive. The control group category of retail sales which is the BEA’s consumption component averaged a 0.57% gain in April, May and June. This dropped to 0.4% monthly in the third quarter. All the increase was in July (0.9%) and August (0.3%) with September flat. October’s sales figures will be released on November 15th.

Consumer confidence also ebbed in the third quarter. The Michigan Consumer Sentiment index averaged 98.46 in the second quarter and 93.8 as the second half began.

Reuters

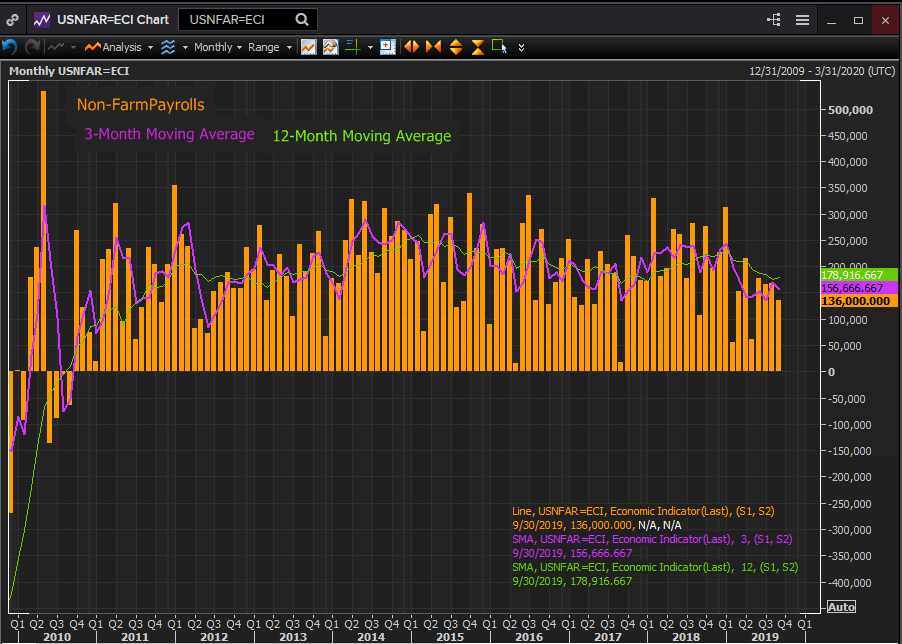

Job creation improved slightly in the third quarter rising to 157,000 in July, August and September from 152,000 in the previous three months. October’s figures will be released on Friday November 1st, 90,000 is forecast for non-farm payrolls.

Despite the stability in the middle half of the year, payrolls have declined from 245,000 in the three month moving average in January to 157,000 in September with the 12-month average falling from 235,000 to 179,000.

Reuters

Business confidence and investment

The US trade war with China and the pending but not consummated departure of Britain from the European Union and their potential impact on the global economy have been the overriding factors taking businesses sentiment from last year's most optimistic view in a decade to September’s near recessionary outlook.

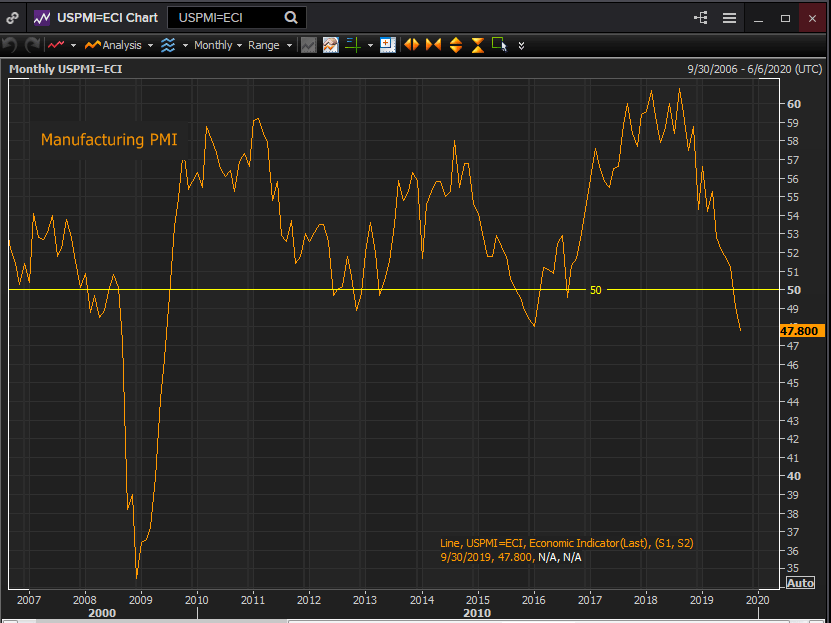

The purchasing manager’s index for manufacturing from the Institute for Supply Management has plunged from 60.8 in August 2018 and 56.6 in January of this year to 49.1 in August and 47.8 in September.

Reuters

These are the lowest scores in three years and the first months below the 50 demarcation between expansion and contraction since the run of October 2015 to February 2016.

Confidence in the much larger service sector which comprises about 85% of US economic activity, has not fallen into contraction but the decline has been as steep, if not as far.

This purchasing managers’ index has dropped from 60.8 in August 2018 to 59.7 in February and 52.6 in September. That is the lowest reading since August 2016 just before the two year surge that began with the November Presidential election.

Business capital investment has reflected the precipitous decline in confidence. The durable goods category of non-defense capital goods ex-aircraft, an oft cited proxy for business spending, has fallen from an average 0.27% gain in the second quarter to a 0.37 decline in the third. Business investment was negative in August and September following a flat July.

Conclusion

Of the three spending categories that support GDP, consumption, business investment and government procurement only two, government and the consumer contributed to economic growth in the third quarter.

The strong pace of consumer spending (retail sales control group) in April, May and June of 0.57% per month combined with moderately rising government expenditures and the weak but positive 0.27% a month growth in business investment was sufficient to propel GDP to 2.0% in the second quarter

But the drop in consumption to 0.4% a month in Q3 and the direction from 0.9% in July to 0.3% in August to flat in September coupled to the 0.37% monthly decline in business investment in July, August and September means that even the modest pace of second quarter GDP is out of reach. Considering the movement of consumer and business spending within the quarter, even the 1.7% median forecast may be too optimistic.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.