US Retail Sales December Preview: ‘Twas the month after Christmas

- Retail sales expected to have the best holidays in three years.

- Control group sales a GDP component predicted to rise 0.4%.

- Labor market continues to foster robust consumer sentiment.

The US Census Bureau will release the advance report on Monthly Sales for Retail and Food Services for December on Thursday January 16th at 13:30 GMT, 8:30 EST.

Forecast

Retail sales are projected to increase 0.5% in December after November’s 0.1% gain. The retail sales control group, the Bureau of Economic Analysis’ GDP component, is expected to rise 0.4% following its 0.1% increase in November. Sales ex-autos are predicted to increase 0.5 after a 0.1% gain in October.

Retail sales and the labor market

Wages, income and payrolls are the main struts of consumer spending. If wages and income are steady or rising, and if individuals are confident that they can find a new job if needed then the natural tendency toward consumption can be indulged.

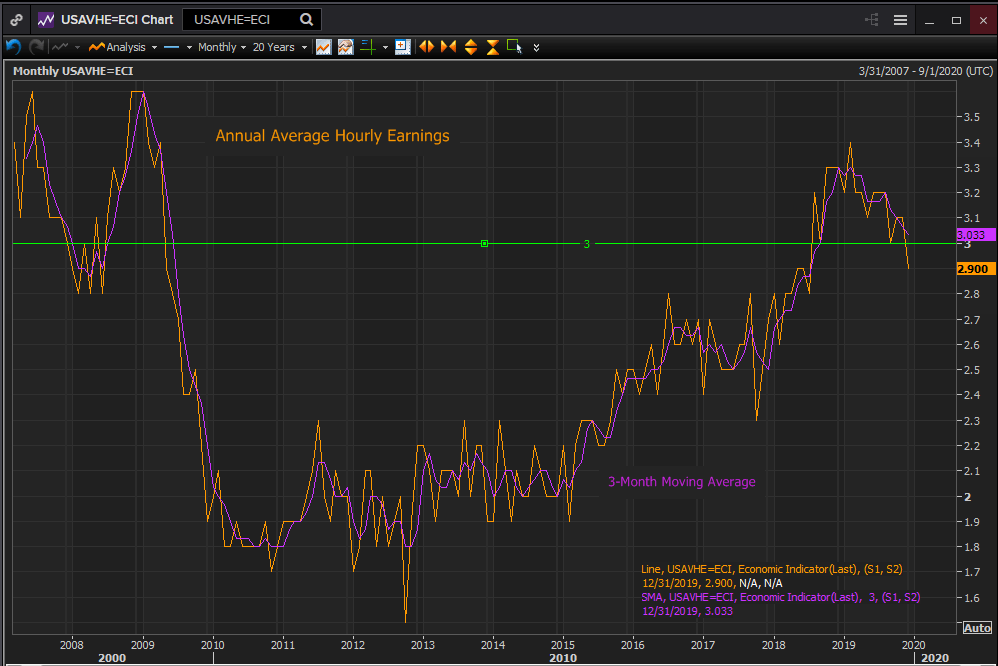

Average annual wage gains were 3% or higher for 16 months from September 2018 to November 2019, the longest span in the series which goes back to March 2007. Earnings fell to 2.9% in December.

Reuters

Personal income which includes wages, social security and pension payments and business and dividend income rose 0.5% in November, 1% in October and 0.3% in September. While gains are down from a 0.6% peak in February they remain a reliable addition to household finances.

The economy created 256,000 job in November and if the December total of 145,000 was a disappointment it is only so in the context of the 176,000 monthly average for the year. With unemployment at 3.5% and initial jobless claims at 224,000, both near 50 year lows, individual and households can be more than reasonably sure of improving income in the year ahead or finding new work should that be necessary.

Consumer spending is closely connected to income and the availability of jobs. The long-running expansion of the labor market has, over the past year, brought workers the benefits of rising income it is almost inevitable that some of that returns to the economy as consumption.

Consumer sentiment

Not surprisingly consumer attitudes and outlook reflects the sanguine state of their finances.

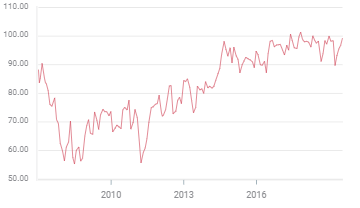

The Michigan Consumer Sentiment Index registered 99.3 in December and is forecast to remain there in January when the month’s figures are released on the 17th. That is the highest score since 100 in May and it brings the survey back to the highest reaches of the last three years. The country has not been so happy with its economic status in almost two decades.

Michigan Consumer Sentiment

With income and wages rising, inflation low and jobs a buyers’ market, consumers can reasonably be expected to spend in the holiday season.

US-China trade

The phase-one deal between the US and China which will be signed on the 15th in Washington will ameliorate the trade antagonism of the last two years. Chinese consumer products will not be subject to tariffs as the US had threatened and American farm products will return to the mainland market.

As important as the specific terms of the agreement should be the change in the relationship between the two great powers. The danger of the trade dispute has been in the background of most of the economic conversation since it began in January 2018. Its end should benefit attitudes, high and low, on both sides of the dateline.

Federal Reserve and the dollar

The Fed governors predicated their policy in the second half of last year on preserving the economic expansion and protecting the labor market. The 75 basis points of rate cuts from July to October, perhaps surprisingly, did not end the dollar strength.

From early August to the low on October 1st the dollar gained a bit more than 2% against the euro, modest but impressive with a newly adopted central bank looser rate policy. Again it was the acrimonious trade war that until the October 13th announcement of an agreement seemed headed to further escalation that brought the greenback the buyers of the safety trade. Once that danger was removed the dollar returned to the level of late July, just prior to the Fed’s change in policy, where it currently sits.

Fed policy is firmly on hold with its own economic projections seeing no rate adjustment until 2021. The dollar will get no benefit or penalty from the central bank this year unless that policy changes. Economic statistics and the state of the US, European and Japanese economies will determine the competitive relationship of their currencies.

Conclusion

Income, wages and the job market should continue to enable a healthy consumer economy. Removing the lingering fear of an ever worsening trade war with China should bolster consumer attitudes and return business spending and manufacturing jobs. Equity prices can only add to the general sense of economic well-being.

The ingredients are in place for a burst of consumer spending.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.