US Nonfarm Payrolls November Preview: Can we agree the labor market is healing?

- Stable payroll growth forecast at 550,000 in November, unemployment at 4.5%.

- Demand for workers remains high, labor and sales indicators are positive.

- Markets have been distracted by the Omicron variant, Fed statements.

- US dollar and Treasury rates should rise with NFP.

The US labor economy may have finally turned the corner. Economic growth in the fourth quarter has revived, consumers are spending despite inflation and employers have regained their hiring optimism.

American job creation should complete an excellent six-months on Friday when Nonfarm Payrolls (NFP) are expected to show 550,000 new employees in November following 531,000 in October. The unemployment rate is expected to drop to 4.5% from 4.6% and the underemployment rate is predicted to rise to 8.4% from 8.3%. Average Hourly Earnings should increase 0.4% in the month and 5% for the year.

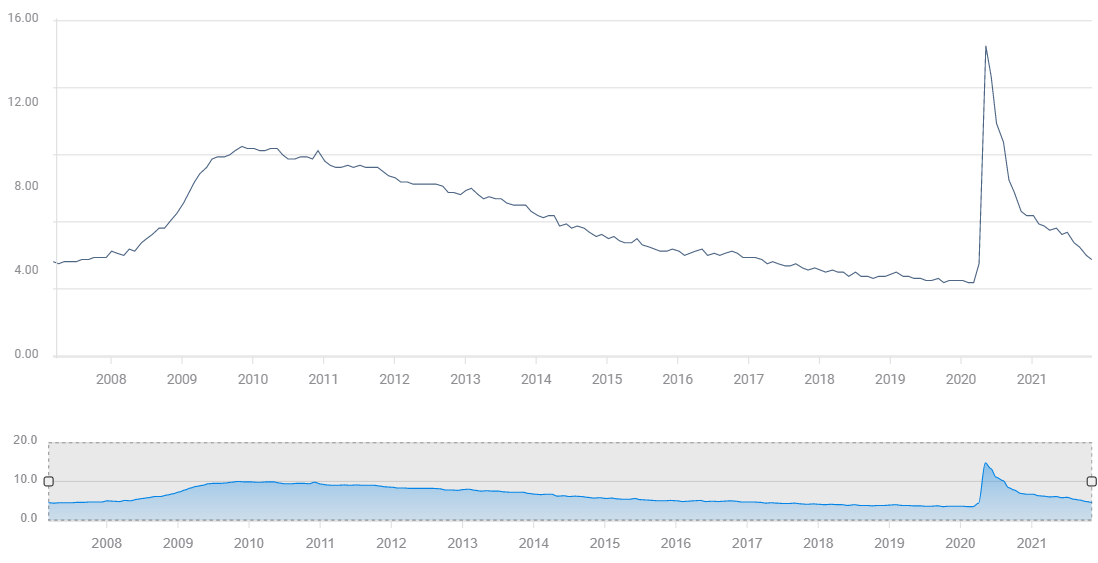

US Unemployment Rate (U-3)

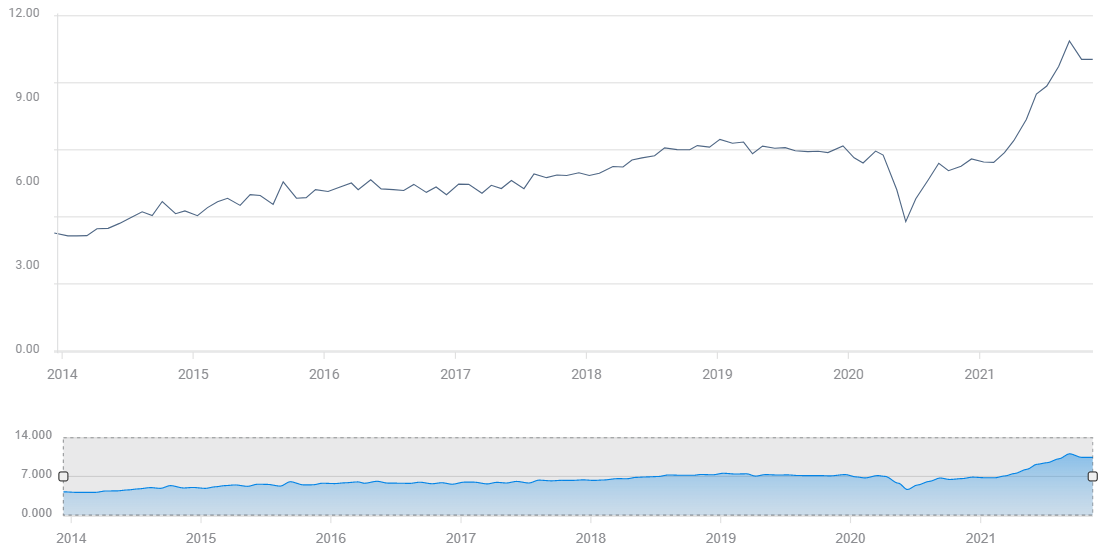

Labor Market indicators

From May through October Nonfarm Payrolls averaged 646,000 new employees. The US economy has added 3.9 million jobs in that period. That is the best performance since the initial lockdown recovery that began in May 2020.

Other information from the Employment Situation Report, the official name for the Labor Department data, has the same record of improvement. The unemployment rate (U-3) has fallen from 5.8% to 4.6%. The underemployment rate (U-6), which casts a much wider net for involuntary joblessness, has tumbled from 10.2% to 8.3%. Average Hourly Earnings (YoY) have increased 2.5 times, from 1.9% in May to 4.9% in October. The Labor Force Participation Rate is unchanged at 61.6%. Only Average Weekly Hours have slipped to 34.7 from 34.8.

Attendant labor market indicators are equally positive.

The private payroll clients of Automatic Data Processing (ADP) added 534,000 employees in November. Over the last seven months the average gain has been 598,000.

The Job Offerings and Labor Turnover Survey (JOLTS) has averaged 10.1 million unfilled positions each month from April through September. The previous all-time record for a single month was 7.6 million in January 2019.

JOLTS

FXStreet

Initial Jobless Claims dropped to 199,000 in the week ending November 19. That is the lowest total of new filings in over 50 years, since January 1969. The 4-week moving average was at 252.250, the lowest since March 13, 2020.

The Employment Purchasing Managers’ Index (PMI) for the manufacturing sector from the Institute for Supply Management (ISM) rose to 53.3 in November. That was better than the 51.1 forecast, up from 52 in October, and the highest reading since April. The service Employment PMI will be reported on Friday and is expected to rise to 52.2 in November from 51.6 in October.

American firms have continued to fill jobs left empty by last year’s lockdowns and the subsequent reluctance of workers to reenlist. The plunge in hiring in August and September which caused so much consternation was a brief hiatus, following two months where NFP placed more than two million employees. Jobless claims are approaching the full employment levels of the months prior to the onset of the pandemic.

Employers remain optimistic that more employees are needed, the JOLTS totals are more than two million above the prior record, and acquisitive, offering bonuses and wage increases.

The US labor market is fully functioning and unless new restrictions are implemented will soon regain pre-pandemic levels of employment.

Consumer Confidence, Personal Spending and Retail Sales

American consumers have continued to spend despite consumer confidence levels normally associated with recessions.

The Michigan Consumer Sentiment Index plunged from 81.2 in July to 70.3 in August and has not recovered. It has averaged 70.6 since August, with some of the lowest optimism readings in over a decade, scores that are comparable to 2010 and 2011, when the economy was still burdened with the financial crisis.

Consumers drive the US economy. Normally 70% of Gross Domestic Product (GDP) is ascribed to domestic consumption. Historically, consumer spending rises and falls with sentiment. Over the past several months that connection has been absent.

Americans are clearly unhappy, but so far that distress has not carried over to the family budget.

Personal Spending has increased 0.70% a month from August through November. In 2019, the last full year before the pandemic, this consumption measure averaged 0.36% monthly.

The contrast is even more pronounced than the simple spending comparison. For most of 2019 unemployment was at a record low, wages for many workers were rising at the highest pace in a generation and inflation was below 2%.

Despite those excellent economic conditions, reflected in the Michigan Survey which averaged 96 for the year, consumers were only spending about half as much as in the past four months.

Retail Sales offer the same judgement.

From August to November, sales climbed 0.58% each month. In 2019 the average gain for the entire year was 0.45%.

Retail Sales

Retail Sales and Personal Spending are the numbers that inform the manufacturing and services PMI outlooks and despite the pandemic media background, they remain strong.

The ISM New Orders Indexes also show healthy incoming business. Orders in the manufacturing sector rose to 61.5 in November, and except for October’s score of 59.8, have remained above 60 for 17 months. This is the longest stretch in the series’ history.

Orders in the service sector for November will be reported on Friday at 10:00 am ET. The index is forecast to drop to 64 from 69.7, which was the highest reading on record.

Traditionally, business sales estimates depend heavily on the consumer outlook. When consumers become despondent, managers expect sales to follow the outlook lower.

In the current somewhat unusual situation, many businesses are taking their cues from sales figures rather than worrying about consumer sentiment. As long as orders are flowing into a firm’s hoppers, managers have every reason to add staff and ramp up production.

Markets and the Federal Reserve

Markets have been more attentive to the Omnicron variant of the pandemic, panicky is perhaps a better description, than to comments from Federal Reserve Chair Jerome Powell that the central bank may speed up its exit from emergency support measures.

Several nations in Europe and Australia have already reimposed varying degrees of closures and the resulting diminution in global growth expectations has been greatly exacerbated by the fear of the Omicron variant.

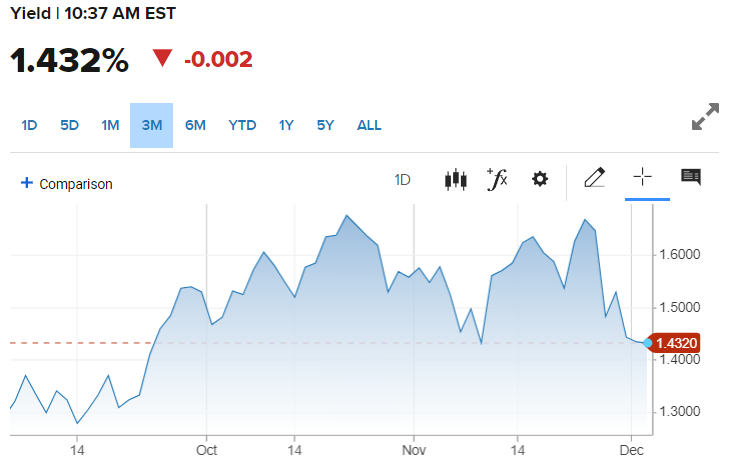

Treasury rates have responded to the threat, realistic or not, that the new variant may give governments a reason to restrict or shutter their economies. The US 10-year Treasury yield has lost 21.4 basis points since closing at 1.646% on November 23. Equities have tumbled around the world as the economic recovery again takes second place to pandemic mitigation.

US 10-year Treasury yield

CNBC

Risk aversion has returned to currencies, with the Japanese yen sharing the safety role with the US dollar, though the greenback has been somewhat undermined by the sharp drop in Treasury yields.

Conclusion

The November payroll report stands a good chance of performing better than forecast. Signs from the labor market and consumer economy point to a continued recovery in the United States. Growth in the US – currently running at 8.6% in the fourth quarter according to the Atlanta Fed – can be derailed if the states reimpose economic restrictions. At the moment that seems far fetched but there is no certainty.

Market response to the NFP report depends largely on the state of panic over the Omicron variant. If payrolls are better than expected they will support Treasury rates and the dollar, the caveat being the Omicron fear.

Even if job creation is weaker than expected but still positive, the dollar and Treasury yields should benefit because the Fed has indicated the labor market has sufficiently recovered to permit higher interest rates.

The recent sell-off in Treasury yields and equities is overdone. Payrolls are about to remind the markets that panic does not pay.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.