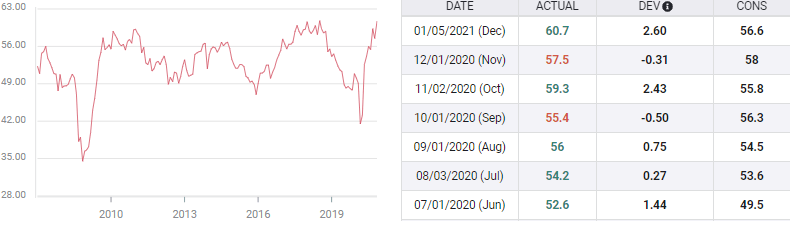

US Manufacturing PMI: Setting the stage for NFP

- PMI expected to slip to 59.5 in January from 60.7 in December.

- Business outlook has remained strong in fourth quarter.

- Retail Sales and the faltering labor market have been ignored.

- Manufacturing PMI has focused on the pending recovery.

- Dollar will be supported by a good PMI but Friday's NFP is the main chance.

American business attitudes have remained resolute in the fourth quarter with firms investing for the recovery even as Retail Sales turned negative in the holiday season.

The Purchasing Managers' Index (PMI) from the Institute for Supply Management (ISM) is forecast to drop to 59.5 in January from 60.7 in December. The New Orders Index was 67.9 and the Employment Index was 51.5 in December.

Manufacturing PMI

In the seven months since the recovery from the spring collapse began in June the Manufacturing Index has averaged 56.3. The three-month moving average of 59 is the best since October 2018.

These indexes were pioneered by ISM and have been issued continuously since 1931 with a four-year hiatus during the Second World War. They are diffusion indexes, originally developed to identify business cycle turning points, that indicate month-to-month change. The index is formulated with the division between contraction and expansion set at 50. All later indexes have followed this model.

The manufacturing Index is considered an indicator for the overall economy despite the factory sector only being about 15% of GDP.

Manufacturing PMI

Since the Manufacturing Index unexpectedly returned to expansion in June it has outperformed forecasts in five of seven months. This has continued despite Retail Sales turning negative in the fourth quarter at -0.73% per month. The two major labor market statistics, Initial Jobless Claims and Nonfarm payrolls also reversed in November and December.

Reuters

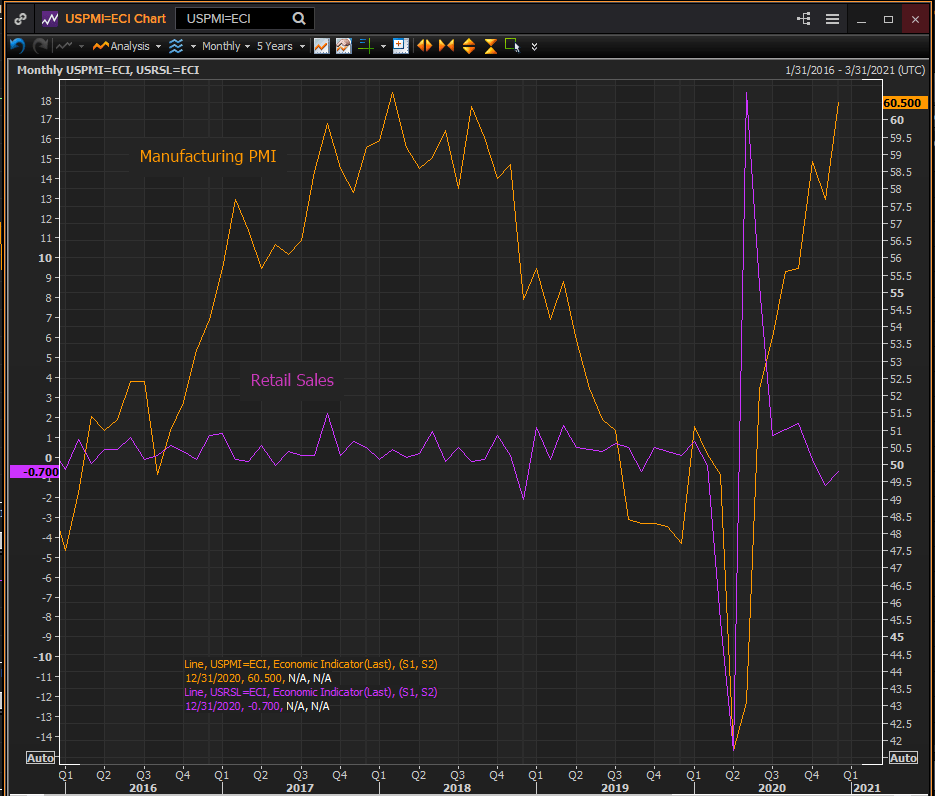

Retail Sales and the labor market

Consumption recovered smartly from the lockdown plunge of 22.9% in March and April by soaring 26.9% in May and June. That surge continued in July, August and September with a three-month average of 1.4%, excellent in any era.

However, rising viral counts in many states, a stringent lockdown at the end of the quarter in California and increasing layoffs and faltering job creation in November and December struck consumers in their most vulnerable and worrisome point, employment. Retail Sales have followed the labor market down.

Initial Jobless claims in the first and last weeks of November were 711,000 and 716,000, the lowest of the pandemic. But the two middle weeks averaged 767,500. Even with totals for half the month increasing sharply, the November average of 740,500 was the seventh straight month of improvement and 58,000 lower than October.

Claims had had similar brief increases in July and in August that did not signal a general rise in layoffs or a drop in hiring. At the end of November the labor market was still improving.

That ended in the first week of December when claims rose to 862,000 followed by 892,000, the highest seven-day total in two-and-a-half months. December's average jumped to 837,500, the highest in 12 weeks.

Nonfarm Payrolls reflected the deterioration in the job market. Payrolls dropped to 336,000 in November from an average of 660,500 in September and October.

In December the market lost 140,000 positions, the first negative month since April and a reversal on the 71,000 forecast.

Claims have continued at a much higher pace in January averaging 867,500 through January 22 and are forecast to be 830,000 for the January 29 week due this Thursday.

With layoffs continuing at a higher level in January than December, the current 85,000 estimate for this month's payrolls, to be issued on February 5, is optimistic.

Conclusion

The business community is preparing for the recovery with investment and inventory build convinced that the retreat of the pandemic will not only enable a return to normal but encourage a burst of relief spending.

The optimism has not yet carried over into hiring. Employers are waiting for proof that the projected surge in consumption takes place before committing to new workers. The ISM employment Index has been the laggard of the Manufacturing Indexes only reaching 52.1 in October.

Reuters

Dollar will be supported by strong ISM numbers but the main game this week is the payrolls report on Friday.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.