US Manufacturing PMI: Factories rebound despite China virus threat

- Manufacturing PMI positive for first time in six months.

- First expansion in new orders since July, export purchases rise.

- Poll conducted during the January China health crisis.

The US manufacturing sector ended its five month contraction in January as the new orders, export orders and production metrics unexpectedly rebounded suggesting that business spending may be reviving after a year-long slump.

The purchasing manager’s index from the Institute for Supply Management rose to 50.9 last month from December’s upwardly revised 47.8. Analysts in the Reuters poll had forecast 48.5. It was the largest monthly advance since mid-2013.

Reuters

This is the first month since June where the result has been better than the consensus forecast. A reading above 50 indicates expansion. Manufacturing accounts for about 12% of US economic activity.

New orders jumped to 52.0, an eight month high, from 47.6 in December which had been the lowest reading in more than seven years and the third lowest since the recession. New export orders rose 6 points to 53.3 its best performance since 56.0 in September 2018.

Reuters

The production index jumped 9.5 points to 54.3 in January after five months below 50. Employment increased but did not reach growth scoring 46.6 in January up from Decembers 45.2.

Economic growth in the US slowed to 2.3% in 2019 the weakest rate in three years after registering 2.9% in 2019. The US is in its 11th consecutive year of growth the longest span in US history.

Consumer spending has held up well supported by the strong labor market and rising wages. The retail sales control group which is the consumption component of the GDP calculation averaged a 0.33% monthly gain from February to December.

Reuters

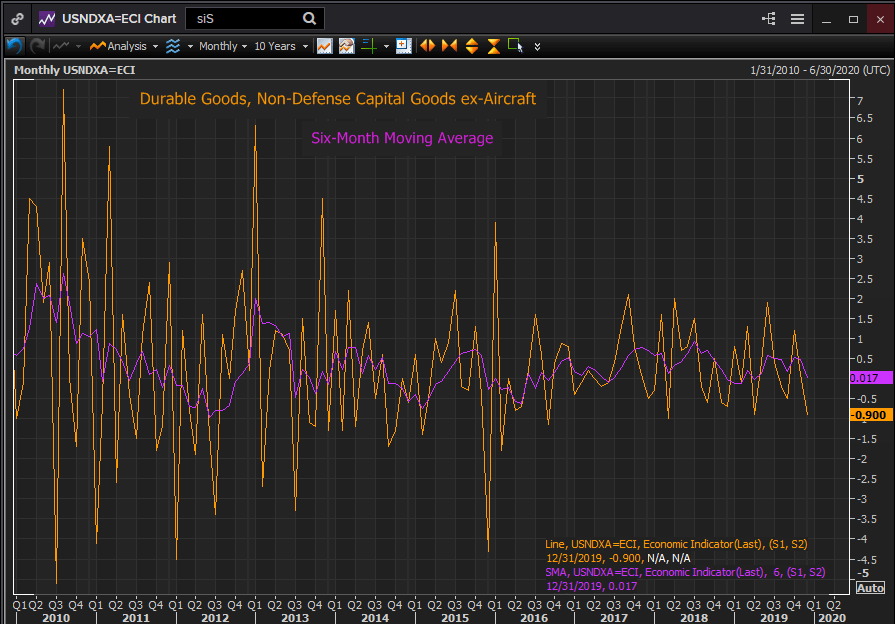

Business spending however declined sharply in the second half of the year. The durable goods category non-defense capital goods excluding aircraft, a common analog for business investment, dropped from a 0.567% monthly average in June to 0.017% in December. Overall business investment contracted for three straight quarters to the end of the year, the worst period since 2009.

Reuters

The US manufacturing sector was hard hit by the almost two-year long trade war with China. New hires for factory work declined from 264,000 in 2018 to 46,000 last year.

The US-China trade deal signed on January 15th in Washington has greatly reduced tensions between the world’s two largest economies. China has pledged to buy large amounts of American farm products and to eliminate some of its technology and ownership requirements for foreign companies and the US has canceled the imposition of new tariffs and lowed some existing ones.

China’s quarantine of several cities and temporary shuttering of factors and offices in an effort to prevent the spread of the corona virus will hurt mainland economic growth but to what degree is unknown as much depends on the success of the control measures.

News coverage of the health crisis in China has been widespread since the first week of January before the ISM survey* was sent out and answered. For January at least, the impact seems to have been minimal though it could erode sentiment in future months.

“We’re going to have to wait and see” whether the PMI continues to expand in coming months, Timothy Fiore, chair of the ISM’s manufacturing survey committee, said on a call with reporters as reported by Bloomberg. “Weakness in the inputs for January questioned demand for expansion in February and whether we’re at the beginning of sustained PMI expansion.” Additionally, the corona virus is likely to have an impact in February, he said.

Continued improvement and strength in manufacturing would indicate that the trade deal with China is having a positive impact on US factories.

*“The Manufacturing ISM® Report On Business® survey is sent out to Manufacturing Business Survey Committee respondents the first part of each month. Respondents are asked to report on information for the current month for U.S. operations only. ISM® receives survey responses throughout most of any given month, with the majority of respondents generally waiting until late in the month to submit responses in order to give the most accurate picture of current business activity,” noted the ISM report.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.