US ISM Non-Manufacturing February PMI Preview: The Fed, US Treasuries and the dollar

- Services PMI forecast to slip in February but remain expansionary.

- Employment index projected to rise despite China health crisis.

- New Orders index expected to stable with a small increase.

- Fed rate cut underlines US and global risks.

The Institute for Supply Management (ISM) will issue its Non-Manufacturing Purchasing Managers’ Index for February on March 4th at 15:00 GMT, 10:00 EST.

Forecast

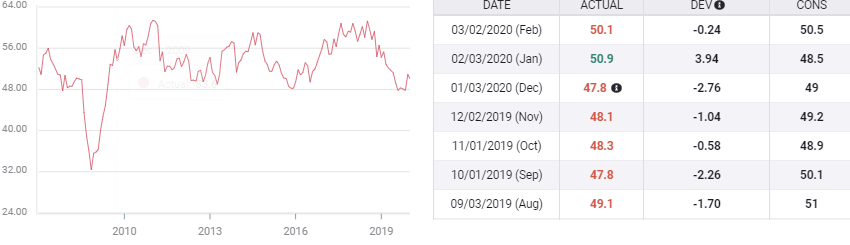

Services PMI is projected to fall to 54.9 in February from 55.5 in January. The new orders index will rise to 56.3 from 56.2. The employment index is predicted to increase to 54.1 in February from 53.1 the prior month. Prices paid will drop to 54.5 from 55.5 in January.

Purchasing managers’ indexes, manufacturing and services

Manufacturing has absorbed the brunt of the sentiment difficulties from the US-China trade war.

The overall PMI was in recession for five months from August to December last year and the low of 47.8 in September and December was the weakest reading since the recession. New orders and employment indexes were equally poor through the late summer and fall. The unexpected rise to 50.9 in January, far ahead of the 48.5 median forecast, was due owed to the long-awaited US-China trade pact which was signed on January 15th.

US Manufacturing PMI

Despite the virus induced plunge in February’s official PMIs in China to 29.6 in services and 35.7 for manufacturing, the impact the US has been limited though that could change if the supply disruption prolongs. Indeed, the very size of the mainland collapse in sentiment argues that it is artificial and will recover.

China Manufacturing PMI

FXStreet

Manufacturing PMI in the US managed to stay just above contraction in February at 50.1. Much for US sentiment will now depend on the Chinese government’s success in controlling the Coronavirus and the speed which shuttered production can be revived. Preliminary signs for both appear promising.

Sentiment will also depend on the extent of the virus spread in the United States and the potential plant and office closures.

Optimism in the service sector declined along with the factories but not as far. The 2019 high was in February at 59.7 and the low in September at 52.6. Notably this was just before the US-China agreement was announced on October 15th. Since then January’s 55.5 has been the top.

The new orders result for January, 56.2, is intriguing and its projection for February for a slight gain to 56.3 seems to suggest that the viral crisis in China has had little impact on new business in the United States, an opinion that requires confirmation.

US labor market, wages and consumer sentiment

The well known facts of the labor market, job creation, rising wages, half-century lows in unemployment and jobless claims have supported consumer sentiment which in turn has kept the 70% of US economic activity tied to consumption firm enough for 2.3% average growth last year.

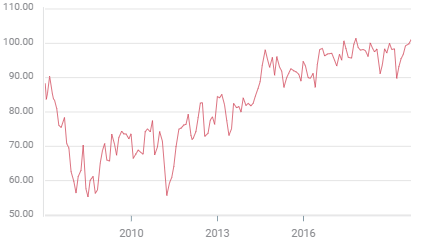

Consumer sentiment figures for February from Michigan University, 101, and the Conference Board, 130.7, remain among the highest post-recession reading and above the vast majority of scores for the past two decades.

The March preliminary figures for the Michigan Survey due on the 13th are expected to show a drop to 97 which, if accurate would not change the assessment of the present US consumer as one of the happiest in the last 20 years.

Michigan Consumer Sentiment

FXStreet

Conclusion and the dollar

The arrival of the Coronavirus in the United States, even if of negligible economic impact thus far, is certainly on the minds of most citizens. Its course in the US is unknown and the degree of work and life constriction that it could force might have a serious effect on consumer sentiment and by degree on GDP. The Atlanta Fed’s GDPNow model does not depict any drag, first quarter growth was estimated at 2.7% on March 2nd.

The Federal Reserve unscheduled rate cut on the 3rd may have underlined the potential threat to the economy but its immediate audience was the equity and credit markets which have moved dramatically to incorporate their perceived risk into prices. Its impact on consumer sentiment will be negative but limited, consumers do not generally take their cues from Fed governors but from the labor market and inflation and to some degree the media.

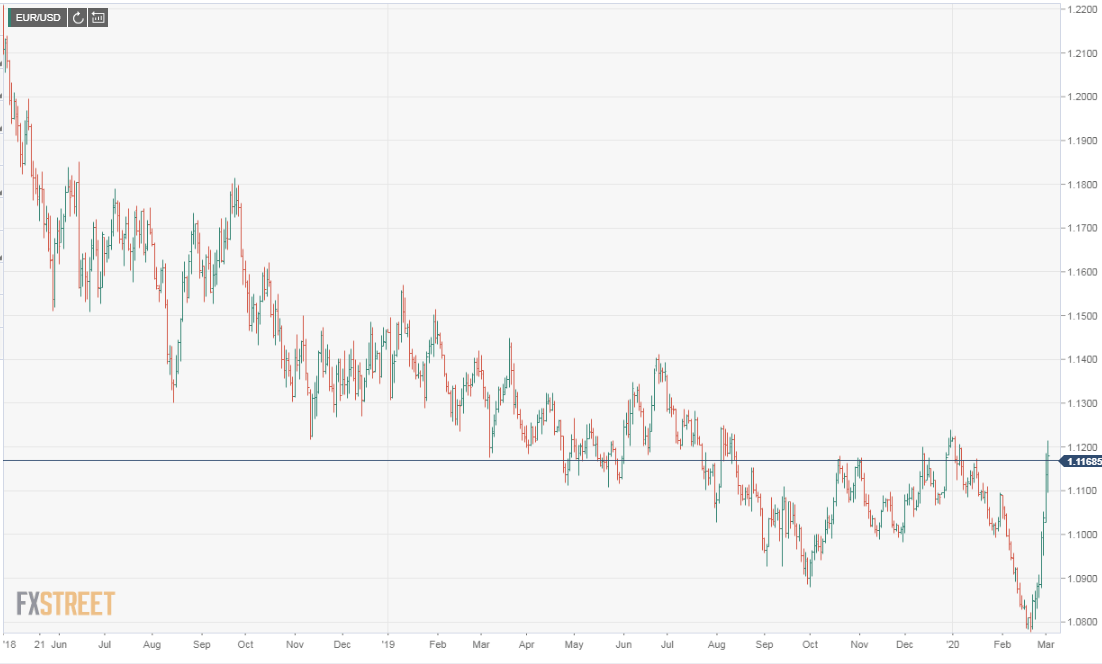

Currency markets have sold the dollar as the collapse of US Treasury rates under the pressure of demand for US government securities has completely overwhelmed the previous safe-haven interest. Since closing at 1.0783 on February 20th the euro has gained 3.6% against the greenback finishing at 1.1171 on March 3rd.

American Treasury rates continued to fall on Tuesday with the 10-year Treasury at a record low of 0.978%. Until the equities recover from their viral frenzy and the credit markets from their apparent conviction that the Coronavirus will have a substantial impact on the global economy, the dollar will continue to pay for the safety status of US Treasuries.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.