US Consumer Price Index December Preview: The inflation sideshow

- Monthly CPI core and headline rates expected to be stable.

- Annual inflation predicted to rise, core to be unchanged.

- Fed policy is not, rhetoric aside, dependent on inflation.

The Bureau of Labor Statistics will issue the consumer price index (CPI) for December on Tuesday January 14th at 13:30 GMT, 8:30 EST.

Forecast

The consumer price index (CPI) is predicted to rise 0.3% in December as it did in prior month. Annual inflation is expected to rise 2.3% in December after a 2.1% gain in November. Core inflation is projected to be unchanged at 0.2% monthly and 2.3% annually in December.

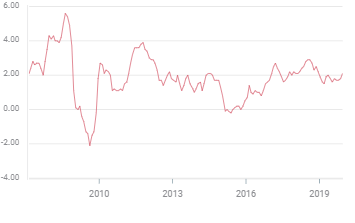

US Inflation

Price changes in the main US inflation gauges have been quiescent over the past year. In 2019 the headline CPI measure varied 0.6% from 1.5% to 2.1%. The personal consumption expenditure price index (PCE) has been even narrower shifting from 1.3% to 1.6%.

CPI

FXStreeet

The core versions of each have shown the same limited range: core CPI moving from 2.0% to 2.4% and core PCE from 1.3% to 1.6%.

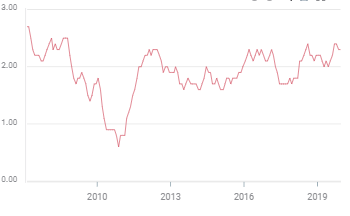

Core CPI

Neither gauge has exhibited a distinctive trend. The Fed’s main concern has been that inflation is below its 2% target and to note that the governors expect their policies will return inflation to its symmetric goal in the future.

Wages and inflation

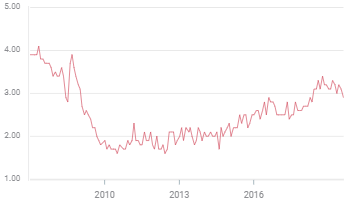

Wages in the US show no sign of incipient upward pressure. Despite the five decade low in the unemployment rate at 3.5% annual hourly earnings have hovered around 3% for more than a year and fell to 2.9% in December. The direct implication is that there is yet considerable slack in the labor market. Payroll growth has slowed about 20% this year. If employers are not offering higher wages because they do not have to.

Average Annual Earnings

The historically low labor force participation rate of 63.2% with its picture of underutilized workers may be more telling for wage inflation than the unemployment rate.

Workers generally demand higher wages when consumer inflation becomes an issue for household expenditures. A feedback loop is created where in order to fund higher wages employers raise prices, which in turn spurs workers to ask for yet more money. This cycle is not evident in the current US economy.

Inflation: CPI vs PCE

The consumer price index and the personal consumption expenditure price index (PCE) are different measures of the variation in consumer prices over time.

Information for CPI is collected and tabulated by the Bureau of Labor Statistics, a division of the Labor Department. It is the older measure with figures back to 1914. The PCE index is calculated by the Bureau of Economic Analysis, a part of the Commerce Department with charts back to 1959.

The CPI is more commonly cited in the press and its rates are used to adjust social security payments and some financial contracts, but core PCE is the gauge used by the Fed in setting rate policy.

The measures are similar though not identical. Both indexes use a comparison of the prices of a basket of goods over time. If the cost of the goods rise from one month to the price index goes up. The main difference is the composition of each basket and the weight given to each the item. The CPI basket is based on household consumption; the PCE is taken from what business are selling. The PCE index also attempts to account for substitution between goods when one rises in price and consumers replace it with a cheaper item.

Consumer price indexes have produced a higher inflation rate. According to the Cleveland Federal Reserve CPI has run about 0.5% higher this century.

From a market aspect the chief interest of CPI, which is released first each month, is as an early indication for the core PCE gauge and its impact on Fed policy.

PCE for December will be released on January 31st

Inflation: Core vs headline

The central difference in the two versions of each inflation index is the inclusion or not of items whose prices have been subject to recurring temporary and sometimes violent price changes from external non-economic factors. In most core price indexes food and energy cost are excluded,

Crude oil is the classic example. In 1973 under the first OPEC embargo the price of a barrel of West Texas doubled in a matter of months. In the year before the financial crash crude again more than doubled

Neither oil shock had a long term effect on prices. From 1980 to 2000 crude prices remained in a $15 to $35 range and it was not until the rise in usage in the 2000s, largely from China that prices moved permanently higher. It remains to be seen if the advent of North American fracking will force prices lower for a substantial time.

Food availability and prices are subject to drought, storms and other natural occurrences hence their exclusion.

The Federal Reserve uses the core PCE index for its inflation measure because it helps to isolate the long-term trends in prices from their daily static. The European Central Bank utilizes an overall measure noting that the impact of inflation on consumers and on economic performance in general is governed by the actual prices paid and received, and energy and food are large components of consumption.

Fed policy and inflation targeting

For the US Federal Reserve it is the long term inflation trends that matter to the economy. Inflations expectations are key to those price movements.

The Fed official adopted a 2% symmetric target for inflation under Chairman Ben Bernanke in 2012, though it had an unofficial goal since 1996 and Alan Grenspan.

Fed representatives from the Chairman on down have devoted considerable rhetoric to their inflation goals and the studied underperformance since the financial crisis. One of the purposes of quantitative easing under Ben Bernanke was to prevent the inflation expectations in the economy from slipping into permanent dis-inflation, that is, ever lower rates of inflation.

Conclusion: Fed policy and the dollar

Inflation remains quiet in the American economy. Neither prices nor wages are moving beyond their ranges of the past several years. The Feds effort under Ben Bernanke to use liquidity to drive the inflation rate higher was largely ineffective.

Under Jerome Powell the emphasis has switched to supporting the economic expansion and the labor market. Inflation is a sidelight, often mentioned but never the direct policy objective.

There is a sense in current Fed analysis that economic growth is the most effective way to push inflation back to its 2% target. Demand for workers and goods will naturally raise prices more than liquidity applications whether from rate cuts or quantitative easing.

Inflation's impact on rate policy has, at least temporarily, ceased to be a driver of the dollar. The Fed will be no more likely to raise the fed funds rate if inflation rises above 2.5% than it will be to cut rates if it slips below 1.5%.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.