The inflation story continues to apply pressure on central banks to take heed

Outlook: Today we get the services PMI and revised composite, as already reported by other countries. Still important despite a big miss last month is today’s ADP private-sector jobs estimate. We also get the usual Thursday jobless claims, expected below 400,000 from 406,000 the week before. Tomorrow’s payrolls is expected at 674,000 after the crazy-low 266,000 in April. Both estimates from the WSJ.

We all imagine that with job openings so high (and so many states ending unemployment benefits early), claims should fall as expected and job recovery should boom as expected. This keeps the Fed on track to consider tapering in just a few months. Yesterday St. Louis Fed Pres Bullard said the labor market is tighter than we know. This might be interpreted as implying the Fed could accelerate the tapering announcement schedule. But another crushing disappointment like the NFP for April could throw a monkey wrench into that tidy scenario. The probability is low but not zero.

Meanwhile, the inflation story continues to apply pressure on central banks to take heed, even if inflation is secondary to job recovery. Today the top story in the FT is about food inflation, which the UN Food and Agriculture Organization says is up 40% y/y in May. Yikes, —40%. This is due to “China’s soaring appetite for grain and soybeans, a severe drought in Brazil, and the demand for vegetable oil for biodiesel” as well as disrupted supply chains. It’s “the biggest jump since June 2011, when the index rose 41 percent. The increase also brings the key benchmark for internationally traded agricultural commodities to its highest level since September 2011…. In 2020, the world’s consumer price inflation for food jumped to 6.3 percent, up from 4.6 percent in 2019, according to the FAO.”

The FT also features a story on how used car prices are a major contributor to US inflation, something Wolf Street has been complaining about for some time. See the chart. “The cost of used cars and trucks jumped 10 percent month-on-month in April, and was up 21 percent compared with a year earlier, making it one of the main drivers of the 4.2 percent year-on-year surge in the US Bureau of Labor Statistics consumer price index. Core inflation — excluding volatile food and energy prices — hit 3 percent.”

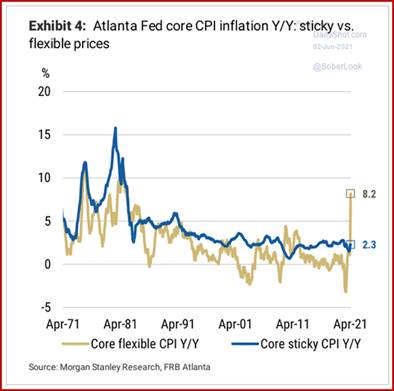

The bond market is right to accept the Fed’s explanation that these price rises are temporary and will get supplied away, or demand will fall on rising prices to reach something more like equilibrium. Besides, not everything is more expensive. How to judge? One of the best charts we have seen in donkey’s years from the WSJ’s Daily Shot—the Atlanta Fed’s sticky price chart. We admit we forgot about it—it’s released the same day as the CPI. This chart shows that a CPI basket comprised of sticky price items—those that change only very slowly—was up 5.5% annualized in April following 3.5% in March, but 2.4% year-over-year. This is not scary. Core sticky-price CPI rose 5.7% annualized and 2.3% y/y.

In contrast, the flexible-price basket rose a whopping 23.1% annualized in April for a y/y of 10.3%. Blimey. Men’s apparel is stickier than women’s but women’s gets a higher weighting. The paper notes that the predictive value of the sticky CPI is pretty good.

While inflation is yet to be known longer-term, by which we mean year-end, the press and especially the WSJ is suffering from schizophrenia. This is the best of all possible recoveries, and yet it will lead to secular stagnation. See the side-by-side headlines.

The recovery really is a historic first. It’s powered by consumers with trillions in extra savings, businesses eager to hire enormous policy support. Businesses and workers are poised to emerge from the downturn with far less permanent damage than occurred after recent recessions, particularly the 2007-09 downturn.

“New businesses are popping up at the fastest pace on record. The rate at which workers quit their jobs—a proxy for confidence in the labor market—matches the highest going back at least to 2000. American household debt-service burdens, as a share of after-tax income, are near their lowest levels since 1980, when records began. The Dow Jones Industrial Average is up nearly 18% from its pre-pandemic peak in February 2020. Home prices nationwide are nearly 14% higher since that time.”

The speed of the rebound is also triggering turmoil. The shortages of goods, raw materials, and labor that typically emerge toward the end of an expansion are cropping up much sooner. Many economists, along with the Federal Reserve, expect the jump in inflation to be temporary, but others worry it could persist even once reopening is complete.”

This is not a jobless recovery as we saw in 1990-1991, 2001, and 2007-2009. It’s not leading to a rise in rates or a drop in asset values, as before. (Well, it’s more like a natural disaster and didn’t come from a financial crisis.) Consumer spending is not retreating but instead booming. And the government was fast to deliver financial support, a real rarity.

So what can go wrong? The Biden budget admits that after gigantic gains this year (5.2%) and next (4.3%), the return to “normal” will seem like stagnation—only 2.2% in 2023 and under 1.9% for the next 8 years. This slide is due in part to demographics and slowing productivity. In other words, then we pay the piper. A word of caution—who says productivity will slow down? And a lot depends on whether the Biden plan can survive an obstructionist Republican party.

These issues are going to take on different coloring once we have the payroll report tomorrow. In fact, they will start to look different starting today with the jobless claims and ADP private sector forecast. Apparently, the whole world, including European equity participants, is hanging on these three numbers. As noted many times before, this is frustrating because the payrolls number is such a lousy number to begin with. At the least, it fails to count the gray economy, which is easily 10% of the total economy, meaning it undercounts a lot of things, including consumption, house prices, used car prices, etc. If all goes swimmingly, the expectation of Fed taper talk stays on schedule—late August hints for a September FOMC announcement. If payrolls disappoint, inflation takes the top spot and pressure on the Fed to reconsider its priorities.

A dollar upside bump is not out of the question. That’s why we always advise against holding a position overnight today into tomorrow. We always get over-reaction and then an over-reaction to the over-reaction. Unless you have fast fingers, get out and stay out.

Tidbit: Several countries are worried about a housing bubble and the accompanying potential moral hazard—New Zealand, Australia, Canada, the UK. This is not, apparently, the case in the US. Wolf Street worries about the abrupt drop in all the housing numbers—shouldn’t institutional investors be getting worried?

Yesterday it was a drop in mortgage applications in the latest week down 4% over the week before and to the lowest in a year. “This put applications for mortgages to purchase a home roughly in the middle of the range of 2019, having worked off the entire Pandemic boom…”

As for that shortage of existing homes—in April the inventory rose to the highest since November, and sales hit the lowest in April since July 2020—again, “having worked off most of the Pandemic spike.” Mortgage applications to refinance existing mortgages have also worked off the “Pandemic spike” and have fallen below the year-ago level.

We can’t blame mortgage rates, still at exceptionally low rates, and even so, refi’s are tanking, too. Wolf Street deduces that sky-high prices do contribute to the fallback, but the key is simply exhausted demand.

Best Tidbit: Trump shut down his blog after less than a month. Hardly anyone was reading it. Apparently, people need their dose of Donny on the TV screen or in person. Trump will be a speaker at the N. Carolina GOP party shindig later this week—while the grand jury in New York is already sitting and will decide whether to indict him, or the Trump Organization, or Trump officers, and/or the Trump kids, with crimes. Meanwhile, disgraced former national security advisor Flynn, who avoided jail on a presidential pardon, called for a military coup over the Memorial Day weekend—but walked it back very fast. Eeek.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat