Sell-on-the-news: CAD likely to fall following BoC rate hike

Outlook:

We get the Beige Book, TICS and industrial production today, as well as the API in-ventory report after the close. The dominant news is likely the Bank of Canada decision at 10 am. A hike would be the third since July and is generally priced in. If the BoC defers action today, it might be because of potential fallout from Nafta being dismantled or otherwise getting screwed up. The BoC could say it's feeling hawkish on the data but wants to wait until Nafta is settled, a position named a "hawkish hold."

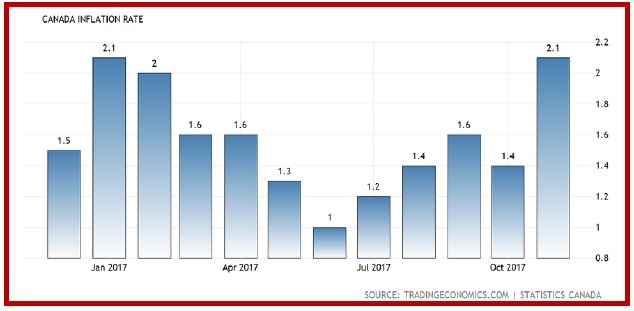

You have to ask whether this is how central banks make decisions. The answer is no. Central banks have clear mandates on price stability and employment, and hardly ever use political events as deciding fac-tors. So, if the BoC sees the data as justifying a hike, a hike it will be. Ah, but should the BoC be wor-ried about inflation? See the chart from tradingeconomics.com. The latest reading is for Nov and shows 2.1%, the same as in Jan 2017 but more than double the rate in June. It's an ambiguous chart. The core CPI is not bad at 1.3% y/y, but up from 0.9% the month before. If the BoC is looking at the rate of change accelerating, a hike it will be. We will likely get the usual seemingly perverse FX response of the CAD falling after the decision on a "sell on the news" effect.

The folks at the ECB will no doubt be watching Canada. The two camps are continuing to form up, dovish Constancio vs. hawkish Weidmann. Weidmann said yesterday he'd like to see tapering to year-end and a rate hike as early as mid-year next year. This is more a revulsion against QE than anything data-based. Eurozone core inflation is averaging 1.15% over the past four months, from 0.9% for most of the year—not enough to set anyone's socks on fire.

Inflation is not justification—but it's not justification in the US, either. Besides, the eurozone is infest-ed with banks holding massive amounts of nonperforming loans and automatic rate increases on them would presumably set off an avalanche of outright bankruptcies. As we have noted before, allowing such a high level of non-performings is a misguided form of socialist management.

This is why Constancio's comment should be respected that there is little likelihood of a policy change next week. He couches it in terms of not choking off growth too soon, but it's really a relief bridge while banks scramble to fix their balance sheets. It's hard to know how fast they are working on it. Meanwhile, the current plan to keep QE going to at least Sept at €30 billion per month. Talk of tapering before then is probably wishful thinking, although Mr. Draghi may bridge the divide with a mention of small changes to forward guidance. Just not next week. It's only January, for heaven's sake.

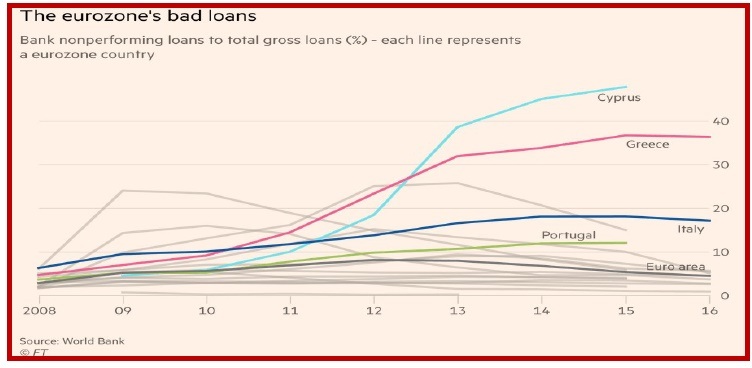

The most recent graphic for nonperformings is from the FT in December. The article then indicated the ECB is not making much progress prodding banks to clean up their balance sheets. There might be something brewing here below the surface that we don't know about.

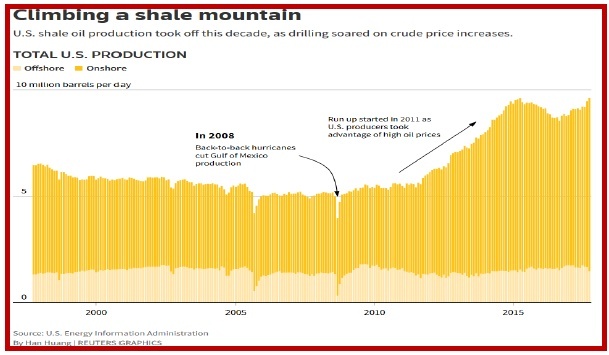

To return to the subject of oil and its inflationary push, see the chart here. To the extent that US output keeps climbing, prices will moderate. The US is a big enough producer (and exporter) now that we should expect a moderating effect in oil prices to permeate all prices in the economy. Granted, the Fed looks at other inflation data and resolutely excludes oil and other "volatile" prices, but as a practical matter, if we can see a cap on oil prices, we need not forecast higher prices generally. What this means is that the Fed will be hard-pressed to justify rate hikes past March.

Questioning the Fed's ability and propensity to keep hiking is a dollar-negative.

Fun Tidbit: We now have the embarrassing situation of two senators and a cabinet secretary denying the president called Haiti and all of Africa shitholes. We expect public officials to lie, but generally they do it a whole lot better. The comment is not important in its own right except as showing the presi-dent a racist, but rather as the rallying point for a knock-down fight in Congress over immigration that could end up shutting the government down at noon on Saturday. It's an entirely unnecessary fight and a crying shame. We continue to think these people will come to their senses and avoid a shut-down, but uncertainty over it is surely a factor holding the dollar down.

Before this latest outrage, The Economist magazine cover story is titled "Is the Trump presidency really this bad?" The editorial says no, because "... Mr Trump has not carried out his worst threats." Oh, dear. Further, it's going to be well-nigh impossible to get rid of him, as it should be. "... Mr Trump is a deeply flawed man without the judgment or temperament to lead a great country. America is being damaged by his presidency/ But, after a certain point, raking over his unfitness becomes an exercise in wish-fulfillment, because the subtext is so often the desire for his early removal from office."

The Economist advises us to ignore the telenovela and judge on actions. Oh, like appointing grossly unqualified persons for high office, drilling for oil in the Arctic, taking millions of children off health care subsidies, groping women, removing worker safety and consumer protection regulations, or profit-ing from foreign governments currying favor by staging events at Trump venues?

The WSJ reports that watchdog group Public Citizen documents "64 politicians, interest groups, corpo-rations and entities affiliated with foreign governments that used Trump-branded properties in the past year," including Saudi Arabia, Kuwait, Tukey and Malaysia. Domestic companies include the Koches and 16 trade groups such as the U.S. Chamber of Commerce.

"Government-ethics specialists say that because the president continues to profit from his business in-terests, it is important to catalog who is spending money at them. Trump can access the extra earnings, perhaps $4 million from the Washington hotel alone, any time. "A group of lawyers including several ex-White House ethics counselors sued the president alleging he is violating a clause of the U.S. Con-stitution that prohibits officials from accepting payments from foreign and domestic governments. A federal judge in Manhattan threw out that suit in December, saying the plaintiffs failed to show how they had been harmed. Similar lawsuits are pending."

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat