The Fed has a serious problem on its hands

Outlook:

We are surprised by the muted response, so far, to the latest North Korean provocation. Earlier in the summer Trump had said the US would respond with "fire and fury." We have no reason to suppose the US response will be anything less this time, although it won't be words, it will be deeds. Former CIA director Panetta said the US should demonstrate it can blow missiles out of the sky. Can we do that? Can Japan? More than one geopolitical expert has said war is inevitable. If so, we can assume that the dollar/yen will be stronger as war approaches, but the path of the dollar against other currencies is murky.

We probably do ourselves a favor by sticking to our knitting, specifically the central banks response to fresh "fast" data as it emerges. We already see that rising inflation in the UK is giving the Bank of Eng-land an itchy trigger finger—and a retracement of the Brexit crash in June 2016 of more than 50%. In fact, this week sterling has "filled the gap" following the Brexit news. As we wrote at the time, that gap was not your ordinary, everyday gap but a runaway gap, and they hardly ever get filled. See the chart. If sterling continues to recover on the rate outlook, it could rise to the 62% retracement level at 1.3833. An appreciation like this might cool the BoE's fervor—or might not. It takes many months for the so-called J-curve effect to get a grip and longer for it to reverse, and meanwhile, the BoE has a job to do.

In the US, it's not a dead cert the Fed got enough push from yesterday's inflation report to restore a rate hike this year, although the CME FedWatch tool puts the probability at 50.9% this morning from 31% a week ago and 46.9% a month ago. Anything over 50% is "strong." But be careful. We still have the Uni-versity of Michigan consumer sentiment and inflation expectations, August retail sales and industrial production today to get through. Retail sales are expected at a a lousy 0.1% after 0.6% in July, and in-dustrial production only 0.1%, too, with capacity utilization remaining at the same sub-par 76.7%.

No matter what today's data shows, the Fed has a serious problem on its hands. Chief Yellen has to guess that the two hurricanes are going to boost inflation, even if temporarily and in limited ways, so how do you watch the US economy as though these effects are not happening? Leaving rates on hold for the remainder of the year, the market forecast until yesterday, risks overheating and a later too-fast catch-up in rates. A too-fast catch-up makes the Fed look foolish and worse, does not serve the "financial market stability" mandate.

As far as we can tell, the Bank of Canada is the only central bank that considers abandoning the 2% target, which is now universal, despite masses of academic papers debating possibly permanent chang-es in the "natural" rate. At the heart of the problem is that pesky Phillips curve, which was disproven and discredited in the 1970's but never replaced. The point here is that actual inflation keeps failing to match expectations in the current recovery cycle. With unemployment at a 16-year low, core inflation should be higher.

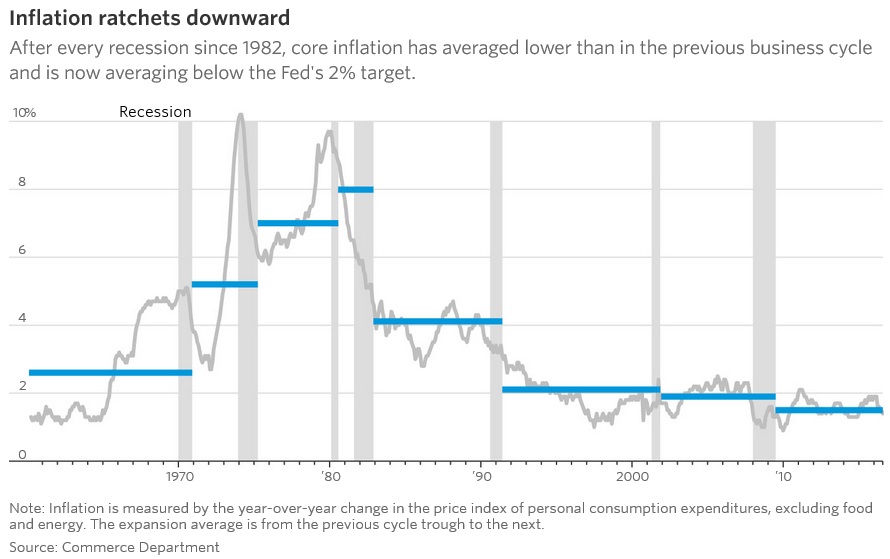

The WSJ's Ip, who is a cocky pest but a decent analyst, says there are three leading explanations. First is that we don't actually have full employment. A rising tide of stories about labor shortages belies this one. Second, there is too much noise in the data, including Yellen's cellphone cost drop. But one-time price events are not a trend and we do have a trend. That's the third point. "Trend inflation has fallen. Until recently, Fed officials scoffed at the possibility. They noted surveys that suggest the public still expects inflation to return to 2% and credit their oft-repeated promise to hit their 2% target. But are they fooling themselves? Expectations of inflation are determined in great part by what inflation actual-ly has been, and after every recession since 1982, core inflation has averaged less than in the previous business cycle: 4.1% in the 1980s, 2.1% in the 1990s, 1.9% in the 2000s, and 1.5% since 2009."

"Lower trend inflation has much graver implications for the economy than appreciated. In recent dec-ades, it has taken ever bigger swings in unemployment to affect inflation. Some critics say this is proof the Phillips curve is nonsense; central bankers conclude that in fact, it has simply flattened.

"The alternative is to ditch the 2% target and accept 1.5% as the new inflation trend. Besides shredding the Fed's credibility, that would mean lower trend interest rates and thus less rate-cutting ammunition to fend off the next recession. If history is any guide, that recession would push trend inflation down further.

Both options are unappetizing, but the second distinctly more so. If Ms. Yellen eventually concludes lower inflation reflects a trend rather than noise, prepare for unemployment to drop much more and interest rates to stay low for a lot longer—with an attendant rise in financial and economic volatility." Much of this argument seems to be sourced by Ip in Fed Gov Brainard's work. We therefore do not know whether the Fed is seriously considering a change in the inflation target. And in any case, with the change in asset purchases the Next Big Thing at the Sept meeting, we won't be hearing about it anytime soon.

We now have two credible scenarios. Trend inflation remains low and soft and eventually the Fed acknowledges it with a lower target. This is the "low rates forever" version that is mostly what the fixed income market prefers. The other scenario is wild inflation, if in a limited number of goods and services and in a limited number of geographic locations but big enough to have a spillover effect. We already see gasoline prices higher in the Northeast even though there is no change in shipments of re-fined goods to that location—shortages are confined to the South. We dismiss spillover effects at our peril.

Our guess is that the Fed stays its hand in September but watches spillover effects like a hawk, enabling it to return to a third hike story by December and allowing it to dismiss the idea of changing the infla-tion target. The big problem with this idea is that the government runs out of funding again at end-Dec, a week or two after the last Fed meeting of the year. Bad timing for the Fed. So we could get the situa-tion—and we have had it before—where the Fed should hike on a realistic interpretation of the data but can't and doesn't because the data is not compelling and the timing is inconvenient. And during this same period to the Dec meeting, Yellen could get fired, too.

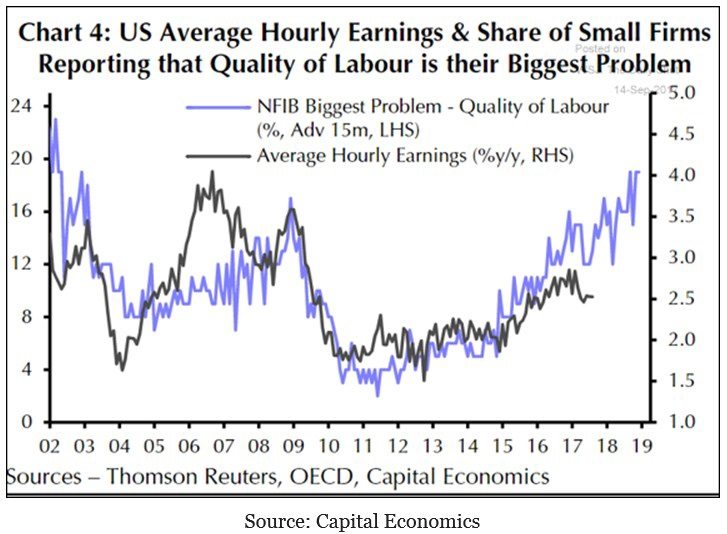

Bottom line: the new acceptance that the Fed is back on the hiking trail is not justified. A probability over 50% sounds nice, but it doesn't fit the other circumstances. And there are structural considerations, too. Yesterday the Daily Shot (from the WSJ) had a chart from Capital Economics showing that even as small firms raise wages, the problem of a shortage of qualified skilled labor is getting worse. Somebody should really revise that Phillips curve, and PDQ. If we are right about the Fed, it's a mis-take to see a dollar recovery except in the mildest and briefest way to clear out oversold positions.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.31 | LONG USD | 09/13/17 | WEAK | 110.05 | 1.14% |

| GBP/USD | 1.3608 | LONG GBP | 09/07/17 | STRONG | 1.3075 | 4.08% |

| EUR/USD | 1.1947 | LONG EURO | 06/28/17 | WEAK | 1.1218 | 6.50% |

| EUR/JPY | 132.99 | LONG EURO | 09/13/17 | STRONG | 131.76 | 0.93% |

| EUR/GBP | 0.8779 | SHORT EURO | 09/13/17 | WEAK | 0.9033 | 2.81% |

| USD/CHF | 0.9604 | SHORT USD | 08/10/17 | STRONG | 0.9655 | 0.53% |

| USD/CAD | 1.2164 | SHORT USD | 08/24/17 | STRONG | 1.2533 | 2.94% |

| NZD/USD | 0.7266 | LONG NZD | 09/13/17 | WEAK | 0.7282 | -0.22% |

| AUD/USD | 0.8016 | LONG AUD | 08/17/17 | WEAK | 0.7931 | 1.07% |

| AUD/JPY | 89.22 | LONG AUD | 09/05/17 | WEAK | 87.30 | 2.20% |

| USD/MXN | 17.6890 | SHORT USD | 09/15/17 | NEW*WEAK | 17.6890 | 0.00% |

| USD/BRL | 3.1194 | SHORT USD | 09/05/17 | WEAK | 3.1409 | 0.68% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat