The end of an era: the financial crisis is over

Outlook:

The calendar is nearly empty—we get US housing starts this morning. Something to ponder is Japan recovering its status from China as the country holding the biggest amount of US Treasuries, $1.13 trillion (down $4.5 billion). China comes second for the first time in two years, with $1.12 trillion, the lowest since 2010 and down $41.2 billion, according to the WSJ's analysis of the Treasury report.

China may has shed more than what shows on the surface, according to a Jeffries economist cited in the FT. If you add Belgium's holdings, some of which are China's, you might subtract another $67.1 billion. China has lost or spent quite a lot, perhaps as much as a quarter from the peak, driven by intervention and capital flight. Former IMF economist Prasad told the FT "This pattern is unlikely to be reversed in the near future, especially with US and Chinese economic fortunes and monetary policy stances continu-ing to diverge. The days of China providing abundant and cheap financing for US budget and current account deficits through the purchases of Treasury securities may have come to an end."

Also worth mulling over is US inflation and inflation expectations. Yesterday CPI came in at 0.2% m/m after 0.4% in Oct, down on lower energy prices. On the y/y basis, CPI is up 1.7%, the most since Oct 2014. Core CPI rose 0.2% after 0.1% in Oct, led by rents, but the y/y is the same 2.1%. Remember that the Fed's preferred PCE version is at 1.7%.

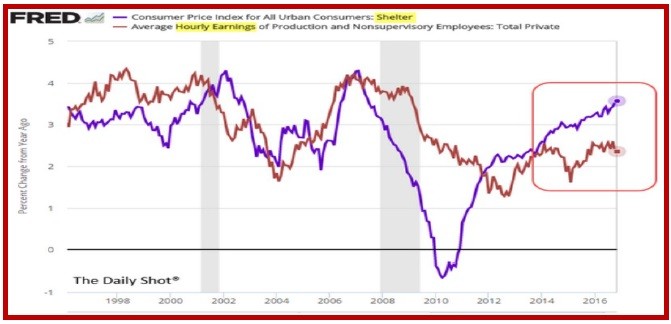

See the chart. We say you can't forecast anything from this chart but some analysts say it implies infla-tion will be hitting the Fed's 2% target long before the Fed sees it coming.

One tidbit: housing costs are rising faster than wages and other prices, with "Owners' Equivalent Rent of Residence CPI" at 3.5%. Rental costs are up 4%. The WSJ "Daily Shot" notes that for seniors, a cohort for which the government has its own CPI, inflation is already near 2% and housing, nearly 3%. And the cost of living bump this year is a measly 0.3%, because Congress decided not to use the senior cost-of-living measure so carefully created for that purpose (higher weights for medical and lower for educa-tion, for example). The senior index was created in 1987 but is still considered "experimental." Bah.

An era has ended. The great financial crisis is over. We might say the crisis actually ended a year ago at the first rate hike, but the four hikes forecast in the dot-plot at the time came under withering attack, and rightly, as it turned out. After a year of uncertainty, the dot-plot is credible. It may even understate expected Fed activism. Some commentators think it was the Trump election that marks the transition, but look at almost any chart—equities and the dollar were already on the upswing before Trump. And before Trump gets sworn in, we have a period of almost one month more to cavort in imagined good things to come.

That's if Trump doesn't ruin it first. After the inauguration, what will be the nature of the next year? Disruption. Sometimes markets like disruption when it takes the form of change that benefits the bot-tom line. Most folks think rising US inflation—from a skilled labor shortage, oil or Trumpian fiscal boosts—will drive the Fed to faster hikes, if not more hikes. At some point equities won't like it, but that's for later in the year.

And while monetary policy divergence has lost its charm as a headline, it's still the relevant theme and the basis for forecasts of euro parity. ING, among others, says it's only a matter of time. Citibank and Deutsche Bank concur, and Goldman calls the dollar one of the top trades for 2017.

Ah, but we have been here before. Just when every shoeshine boy advises you to buy, it's the right time to sell. We have seen numerous occasions when every single fundamental factor pointed to a ris-ing dollar but it crashed on some minor addition to the database. The dollar overreacts to bad news while the euro is Teflon and shrugs off bad news that would fell a lesser currency. This time we imag-ine it will be some stupid Trump statement or action, but it's not necessarily going to be political risk behind a dollar retracement. Sometimes it's just "position adjustment" without a specific news trigger.

Meanwhile, we need to look for cracks in the bigger wall. One of them is China, which is holding up okay on the economic front but with a financial crisis boiling under the surface and capital flight an ongoing problem. Another is the UK and Brexit. The British are bumbling, to be charitable. Warned by Europeans that the window to get a transition plan is only about a year, they are ignoring that timetable and seeking a longer transition. They are not listening. And in their infinite wisdom, sent Chancellor Hammond to S. Africa, Japan and S. Korea to try to forge favored-trade status.

We don't know quite how these two issues, or something else that is now an unknown unknown, will affect the dollar. But you can count on it—parity will be very hard to achieve and to hold.

Politics: The tiresome Trump is still trying to upset the Establishment with appointments of peo-ple to high office who are unqualified or controversial or both. For ambassador to Israel, he may pick a guy who opposes the two-state solution that US diplomacy has been working toward for decades. As for chairman of the Council of Economic Advisors, the sycophantic Larry Kudlow may be the choice. Kudlow used to have influence in the Reagan years, although one of his books admits supply-side ideas did NOT work, something he forgot later as a CNBC commentator. Kudlow keeps trying to push "king dollar," i.e., making the level of the dollar a centerpiece of all other policies, forgetting it had disastrous consequences in the 1970's. A little economic history never hurts.

| Current | Signal | Signal | Signal | |||

| Currency | Spot | Position | Strength | Date | Rate | Gain/Loss |

| USD/JPY | 118.10 | LONG USD | STRONG | 11/10/16 | 106.47 | 10.92% |

| GBP/USD | 1.2444 | LONG GBP | WEAK | 12/05/16 | 1.2717 | 0.00% |

| EUR/USD | 1.0453 | SHORT EURO | WEAK | 12/10/16 | 1.0605 | 1.43% |

| EUR/JPY | 123.45 | LONG EURO | STRONG | 11/03/16 | 114.30 | 8.01% |

| EUR/GBP | 0.8399 | SHORT EURO | STRONG | 11/14/16 | 0.8598 | 2.31% |

| USD/CHF | 1.0278 | LONG USD | WEAK | 11/10/16 | 0.9678 | 6.20% |

| USD/CAD | 1.3349 | SHORT USD | STRONG | 12/06/16 | 1.3259 | -0.68% |

| NZD/USD | 0.7035 | LONG NZD | STRONG | 12/06/16 | 0.7173 | -1.92% |

| AUD/USD | 0.7355 | LONG AUD | WEAK | 12/06/16 | 0.7438 | -1.12% |

| AUD/JPY | 86.87 | LONG AUD | STRONG | 10/06/16 | 78.48 | 10.69% |

| USD/MXN | 20.3464 | LONG USD | STRONG | 10/31/16 | 18.9054 | 7.62% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat