Stock Markets facing increased risks as divergences threaten the current recovery

Should you go ahead and buy stocks right now? Should you be concerned about the future performance of your investment portfolio?

When it comes to financial markets, I have learned that sometimes we cannot have a straight answer to our questions. Instead, we should be able to think in different dimensions, it’s not just a matter of being a “bull” or being a “bear” but, also a matter of “when”, “what” and “where”.

“When” are you going to need your capital in the future? Will you need to have access to your funds, in 5 years, 10 years or longer? It is crucial to define this.

“What” is your risk profile? Can you accept a higher risk for a better return or, are you very risk averse?

“Where” are we currently in the business cycle? Is the real economy topping out, expecting lower performance within the next few years or, is the economy bottoming and better days are ahead?

These kind of questions are important, since they can lead to a better understanding, about “how” to structure our investment approach and portfolio moving forward. Right now, at the time of writing this article, the stock market especially in the US, looks strong in the short term and many investors and analysts have a bullish bias. If you are a short term day trader, you definitely need to go with the trend tactically and “ride the wave”!

But what happens, if you don’t trade or invest short term and you cannot just trade tactically in and out every day? How should you structure your investment portfolio with a 5y-10y horizon in mind?There is the need to do some smart choices NOW that will impact your portfolio later in the longer term.

You need to be aware of the risks ahead, where we are currently on the business cycle and where are we heading. Based on macro fundamentals, it looks we are deep into the end of the current economic cycle. That practically means in the next 2 to 5 years, we are expecting lower returns in the stock market.

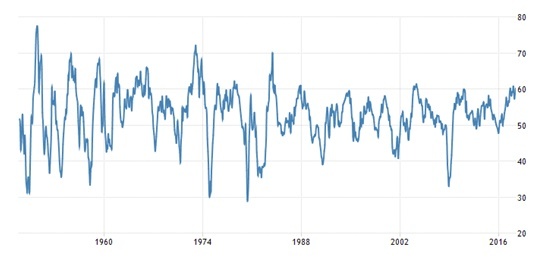

Please take a look at the US ISM PMI, a leading indicator for GDP growth in the economy.

Right now, we are at a 4 month high, a sign of strong activity and growth in the economy. But, please take also another look, all the way back to the 1960’s. Notice what happened 3-5 years into the future, after the index was printing higher values into the 60’s area. You will notice how the economy started contracting again, after a peak around the 60’s level.

So, my concern is that if you go ahead and have a portfolio with a decent exposure in equities, history suggests to expect lower returns in the future. It is more likely the current cycle will start moving lower, as we move forward.

If we make our investment framework a little more complex and add more factors for consideration, we cannot be very optimistic, regarding future expected returns in the equity markets.

It’s not just the extremely expensive valuations in the equity markets, any valuation measure you decide to use. Value alone is not a reason sufficient to have a recession.

But if we take into account the expensive valuations, combined with the macro environment then things look different. We are faced with high valuations, debt levels that are expected to keep rising even more over the next decade, a slightly inflationary environment with a hawkish central bank that is determined to push interest rates higher. That doesn’t spell “opportunity” to me! It is actually a risky environment.

Again, due to recent developments, stock markets might keep pushing higher, in the short term. We are not trying to identify the trend here but, rather how you can create significant value and outperformance in your portfolio. If your decisions are affected only by the short term trend and your sentiment is affected every single day by the financial news then you are setting yourself up for disappointment.

Of course, the trend is important but only in conjunction with other factors too, as we said you need to be multidimensional.

As we mentioned before, at the time of writing this article, equity markets in the US are enjoying a risk-on sentiment and they push higher, as there are positive expectations about the economy. At least that’s the prevailing popular sentiment right now.

I will respectfully disagree and would like to bring to your attention a few other factors to consider too.

China and Emerging Markets combined together account for 74% of Global GDP growth. In simple English, global growth is coming from China and Emerging markets. In contrast, the US accounts for 11% of Global GDP growth. And I can safely tell you that right now the global economy is slowing down, from Europe all the way to China and Emerging Markets.

Please take a look at the Shanghai Composite Index.

The Shanghai Index has moved -24% lower from the Highs since the peak in January 2018. The definition of a bear market is when we have a move bigger than -20% from the highs, so we are officially in bear territory, when it comes to Chinese stocks.

Take a look also in the Emerging Markets ETF.

The EEM ETF has already printed a -20% Low from the peak and there is potential to move even lower.

The S&P500 in the US is performing much better. There is optimism and positive expectations regarding the economy, at least in the short term. The reason I am cautious has nothing got to do with direction. It’s all about reward vs. risk and how we can generate significant outperformance, in our portfolios.

This is the S&P500 chart.

Could the index move higher? Of course.

Is this a good area to “do business”? Absolutely not. Not if you have a decent size portfolio and a longer time frame in mind.

We are currently testing an important resistance and the potential gain vs. the risk is not worth it. Not when China and Emerging Markets are in bearish territory and Europe is seriously slowing down.

Please pay attention to the fact that while the US overall market Indices are moving highe,r there are very significant sectors of the economy that do not “share” the overall excitement.

When you study the US markets, the “canary in the coalmine”, the sectors that would be particularly sensitive to changes in the real economic environment, is the Homebuilders Index (Real estate), the Industrials and the Transportation index.

So, while the S&P500 and the Dow Jones are moving higher, let’s take a look at these three sectors.

Here is the Home Construction ETF ITB.

It is correcting a little bit now but, it has already printed a -20% drop from the High’s since the beginning of 2018. It has also broken the rising trend line, signaling a change in trend is in place.

This is the Industrial Sector ETF XLI.

The Industrials are down -10% from the peak since the beginning of the year, also breaking the trend line to the downside and printing lower highs.

Finally, this is Transportation Average IYT, a very important sector, as it provides clear signals about the real “health” of the economy.

The Transportation Index is down -10% from the peak and it is moving towards the lower range of a triangle, a technical pattern that signifies a change in trend, especially if you come across it at the end of a trend.

Now that you are aware about these let’s consider again the overall status. The US Indices are moving higher but the rest of the world is diverging against this trend. There are also very significant sectors in the US economy that do not move higher together with the bigger indices, signaling a divergence also within the US economy. We expect higher rates, a slightly inflationary environment, international trade wars, geopolitical turbulence, higher debt and a very tough environment for businesses, as profit margins are pressured.

I am not claiming to be an oracle but, this is not an environment where someone can generate significant outperformance in his/her equity portfolio in the mid to longer term.

You need to be very careful.

My recommendation would be a healthy portion of your investment portfolio to be held in cash, 30% to 50% cash depending on your profile and putting together a conservative well diversified portfolio that tactically rebalances to reflect the changes in the economic regime.

How we go ahead and put together that all-weather portfolio?

That’s material for another article! It’scoming soon!

Trade well and trade safe.

Author

Fotis Papatheofanous, MBA

Fotis Trading Academy

Fotis, as you would expect from his name is the key trainer at the Fotis Trading Academy. Fotis is a highly reputed, driven and successful Global Macro Trader and Portfolio Manager.