Shouldn't the Fed wait for effects before Fed funds surpasses inflation?

Outlook: The big day this week is Wednesday, when we get the Reserve Bank of New Zealand rate decision (likely a 25 bp hike), UK inflation (likely a moderation), Germany’s IFO (likely less bad) and the Fed minutes (already out of date).

On Friday it’s Japanese inflation after Tokyo tipped the game to the upside, and the US PCE and core PCE inflation. Before then we get May PMI flash readings, which can be too much information.

It might be short-sighted, but we imagine the central question is what the Fed has in mind. The whole world is hanging on to every word of any Fed speaker (and we get another four today, although none are voters). The press is by no means united in its interpretation of the Friday remarks. Powell said inflation remains “far above” the target and the Fed remains committed to bringing inflation closer to the 2% target. In other words, another hike.

Then speaking with forked tongue, he also said “We’ve come a long way in policy tightening and the stance of policy is restrictive and we face uncertainty about the lagged effects of our tightening so far and about the extent of credit tightening from recent banking stresses. Having come this far, we can afford to look at the data and the evolving outlook to make careful assessments.”

Bloomberg says this means Powell said the most likely course of action is a pause at the June meeting. “Investors pared bets on a rate hike next month to around 13% after Powell’s comments compared with 33% before he spoke.”

To be clear, Powell did not promise a pause. He did say that the already-begun credit crunch could mean activity and inflation could go down some more. If data shows that, a pause might be the right thing. But he also said that if data shows inflation not continuing to moderate, the data consideration will include a hike.

Net-net, the probability lies on the side of a June hike unless inflation falls really hard and/or the credit crunch starts contracting activity really hard. The statement that the “risks of doing too much versus doing too little are becoming more balanced” is not evidence of a pause for the simple reason that we don’t yet have evidence of having done too much.

Reuters says the part about the risk of doing too much means the Fed will pause, and cites Minneapolis Fed Kashkari yesterday saying he can support holding rates steady at the next meeting. (Coming from the most famous dove, this is hardly surprising, just as it’s hardly surprising that the most famous hawk, Bullard, is still talking hike.) Reuters reports “Futures markets see more than an 80% chance of a June pause and still price almost 50bp of cuts by yearend.”

For its part, the FT homes in on the looming credit crunch as the central reason for the Fed to pause.

For what it’s worth, the rest of the Friday conference addressed the neutral rate and while there is some evidence the neutral rate has risen from 2%, the current inflation rate at 4.6% is still a far cry from any neutral rate, raised or not.

Bottom line, we have Bloomberg, Reuters and the FT deducing a pause, but the WSJ and NYT deducing a hike if the stars line up. PCE on Friday will offer clues—see the chart from Reuters. By the time Fed funds is above inflation, shouldn’t the Fed wait for the effects to come in?

We might also say that the smallish dip in the dollar implies the FX market is also deducing a pause, although that tangles up cause and effect too much to swallow. Far clearer are the hawkish Lagarde remarks: “ It's a time when we have to really buckle up and look at this target that we have and deliver on it. We will take all the measures in order to bring inflation back to 2%. We will do it, no question about it."

Forecast: A Fed pause and a refreshed hawkish ECB together imply a euro gain of some size. It doesn’t help to understand sentiment that the euro quickly got oversold on the daily chart and also wants to skitter around the 50% retracement line on the 8-hour chart.

Tidbit: Sometimes an opinion backed by data from the commentariat is worth looking at. Wolfstreet had a doozie over the weekend:

“Treasury yields and mortgage rates rose essentially all week and passed some milestones for the first time since the collapse of Silicon Valley Bank:

The six-month yield hit a 22-year high (5.38%).

The one-year Treasury yield edged above 5%.

The 10-year Treasury yield rose to 3.7%.

The 20-year Treasury yield edged past 4%.

The 30-year Treasury yield rose to nearly 4%.

The average 30-year fixed mortgage rate rose to 6.90% (Mortgage News Daily).

But what is really interesting is the action in the six-month yield (securities that mature in November): Buyers and sellers in this section of the bond market got over their bank-panic and now are starting to price in another rate hike.

The six-month yield now prices in one more rate hike.

The six-month yield closed at 5.36% on Friday, after the 5.38% close on Thursday, both the highest closing yields in 22 years (January 2001), having now entirely shaken off the spooky collapse of Silicon Valley Bank.

The effective federal funds rate (EFFR), which the Fed brackets within its target range between 5.0% and 5.25%, has been at 5.08% since the last rate hike. Another 25-basis point rate hike would bring it to 5.33%. That additional rate hike would put the EFFR just below where the six-month yield is already today.

The part of the bond market that is trading the six-month maturities, after calming down from the bank panic and then re-reading the tea leaves that the Fed put out there, is now starting to see another rate hike over the next few months – if not in June, then at one of the following meetings. And it is getting ready for that rate hike and is starting to price it in. That’s what the six-month yield shows.

…. “The six-month yield reflects securities that mature in November, and the debt-ceiling turmoil doesn’t impact it. That turmoil and the risk the US might default in June has thrown the one-month yield into utter chaos though.

The part of the bond market that is trading in long-dated securities is often hilariously wrong. Remember when it took the 10-year yield down to 0.5% in August 2020, betting on the 10-year yield going negative as it had already done in Europe.

Banks, which are a big part of the bond market, believed this nonsense too, and they loaded up on long-dated bonds and MBS, and then when yields began to rise in reaction to the first signs of big inflation, banks doubled down, believing the Fed’s nonsense about inflation being “transitory,” and when the Fed ate its words and started hiking rates, they continued to buy long-dated bonds instead of dumping them, and then several of these banks collapsed because of their stupid decision to pile into long-dated securities as inflation was rising. So that’s part of the long-dated bond market.

But the other end of the bond market is trading short-term, with securities that mature over the next few months to a year. And they watch what the Fed is actually doing, and they listen to the short-term guidance the Fed gives through its policy decisions, the press conferences, the meeting minutes, and the countless speeches Fed governors give. And by the time the rate hikes or rate cuts take place – unless they’re a surprise – the short-term yields have already mostly or totally priced them in.”

The Debt Ceiling Debacle: Ezra Klein writes, in the NYT, one of the best summaries we have seen:

“The debt ceiling might be the single dumbest feature of American law. Congress decides to spend money and then, later, schedules a separate vote on whether the government will pay its bills. If the government doesn’t pay its bills, calamity ensues.

“Moody’s Analytics estimates that even a short debt ceiling breach could cause a recession. An analysis by the White House’s Council of Economic Advisers modeled a more protracted default and foresaw a crash on the order of the 2008 financial crisis — the stock market falls 45 percent, unemployment rises by 5 points and America’s long-term borrowing costs are much, much higher. All of this to pay money we already owe and can easily borrow. Madness.”

The 14th Amendment says “the validity of the public debt of the United States … shall not be questioned.” Harvard law professor Tribe says it’s not about Biden’s power to apply it, but rather his duty. But for Pres Biden to invoke the 14th Amendment will surely end up taking the case to the Supreme Court, and we know how ornery they can be.

“The White House is open to budget negotiations but opposed to debt ceiling brinkmanship. Republicans are the ones threatening default if their demands are not met. They are pulling the pin on this grenade, in full view of the American people. Biden should think carefully before taking the risk of snatching it out of their hands and holding it himself.”

Pres Biden said on Sunday he was not likely to try the 14th Amendment route because there is not time enough to get through the legal obstacles, and later in the day, a new negotiation was announced to take place between the two principals only.

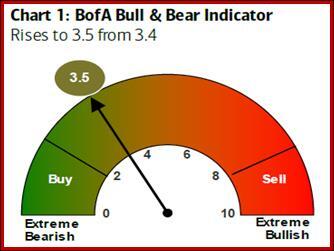

Tidbit: On Friday, the S&P closed up nearly 10% year-to-date and his year and hit its highest level in nine months. Reuters reports “Bank of America on Monday lifted its yearend forecast for the index by some 300 points to 4,300 - another 3% higher from here.”

Tidbit: The display of flags is from a Reader. We don’t know if this is accurate, but it sure does feel good. The text is separate and includes these nuggets (edited). Language use implies it was written by a Ukrainian who learned British English.

“Russia is effed and there is no way out. They started the war with the 2nd biggest armoured force on the planet. They had biggest reserves or missiles. Strong economy fuelled by rising energy prices.

“They were feared and everyone was thinking that Putin is master strategist. Now their armored forces reduced to a fraction of what they were. Their troops committing suicides on the battlefield. Their attacks scaled down to a taking 60k city over 9 months. Their … mercenary army is cursing and blaming regular armed forces for running away and not giving enough ammo.

“Their missile stocks are decreased to bare minimum and whatever they fire gets intercepted by the us provided air defenses. Their VDV [Air Force] is laughed at. The forceful mobilization out hundreds of thousands of men out of their homes into a meat grinder without adequate training and equipment. They are pulling out T55 tanks.

“Their economy is shattered and reserves are frozen. Putin is wanted for war crimes for stealing children. Only talk about counteroffensive makes Russians mumble and cry in fear. Ukrainian counter offensive hasn’t started yet and our new offensive brigades are yet to be seen on the battlefield with new equipment.

“Ukraine only received fraction of what NATO countries can provide. Ukraine is about to get F16. Ukraine just received long range 500kg warhead missiles. Moscova & Crimea Bridge...special underwater operation… Russia is effed.”

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat