Should we be expecting a dollar slump?

Outlook:

Today we get the Bank of Canada meeting outcome—likely about the same as last time (trade is a problem). Bloomberg puts the chance of a hike at a mere 20%. Then there is a joint press conference by Japanese PM Abe and Trump. Aside from Trump already retreating from wanting to re-join TPP after having dinner with Abe, we don't know what to expect from the meeting.

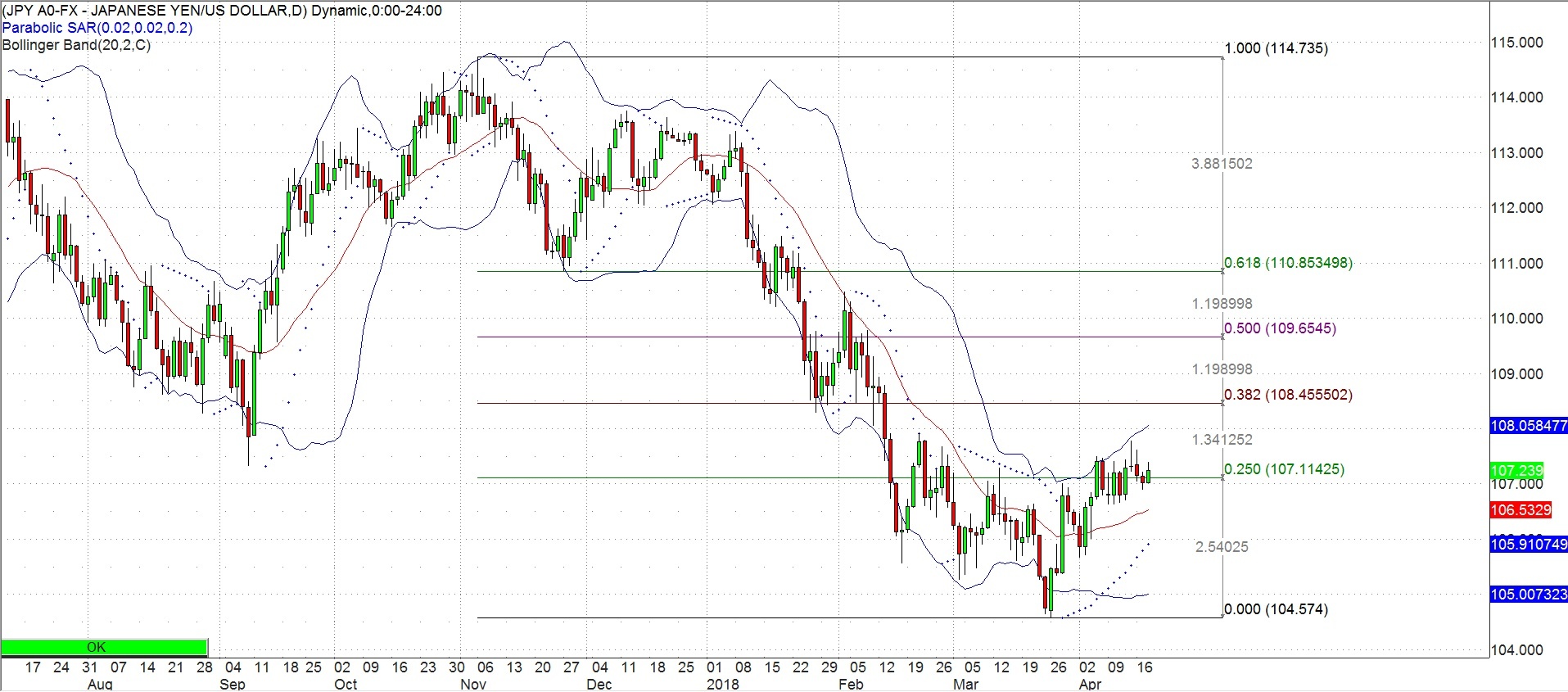

Traders in dollar/yen don't know, either. The dollar/yen fell from 114.74 on Nov 16 last year to a scary 104.57 on March 26, and then corrected by about 25% to the 107 territory--but has been stuck there, more or less, for the last ten days. This is not all that rare and we are not suggesting the MoF has been quietly advising Tokyo traders to cool it, but surely Mr. Abe would not like the yen to be getting weaker at just the time he is speaking to a guy who has railed and ranted against other countries manipulating their currencies for trade advantage.

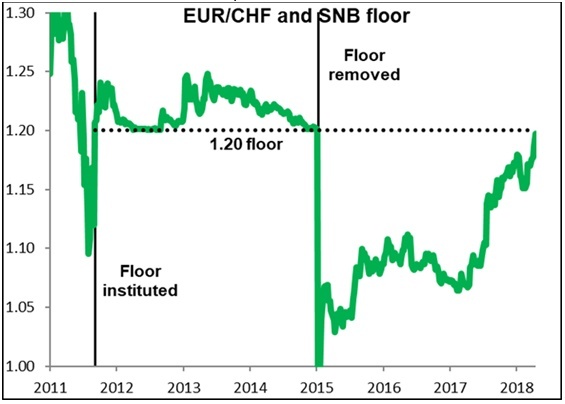

Weirdly, the yen and Swiss franc, both haven currencies, continue to diverge. The Swiss National Bank cares more about the Swiss franc against the euro than against the dollar. At the moment, the euro/CHF is nearly at the old floor of 1.20, the limit that was removed in Jan 2015 to so much shock and dismay (and retail broker bankruptcies). Marshall Gittler at ACLS Global has one of his dandy charts. Most analysts, including Gittler, believe the SNB is well as truly out of the intervention business and fully intends to wait until the ECB initiates normalization before it acts, implying the Swiss has only one direction to go against both the euro and the dollar.

If our model for FX behavior is "buy dollars on risk aversion" but then Trump takes actions that on the whole seem to reduce risk, should we be expecting a dollar slump?

You must admit that the secret trip to N. Korea by CIA director Pompeo and S. Korea's statement that it is formulating a peace agreement are impressive changes. We may never know what was going on behind the scenes to advance this situation after 65 years. Trump will claim credit whether he deserves it or not, but we have tacked 180 degrees from N. Korea lobbing missiles toward Japan and threatening to hit the US mainland with nukes.

It would be apples and oranges to talk about the trade war in the same breath as the Korean situation. Or maybe not, since China is a central player in both situations and today is the Chinese imposition of a 179% tariff on US sorghum. China imported $960 million of the stuff last year to feed livestock and make liquor. You can imagine guys in a back room saying "Let's pretend there is a trade war and pick one thing to make headlines, but secretly we are agreeing China will be mostly let off the hook on trade as long as it brokers the Korea deal." Or maybe we read too many spy novels.

So, we have a relaxation of economic/financial influences out of the White House, but two roadblocks stand in the way of imagining any kind of normalcy. The first is Trump taking back the promise of new sanctions on Russia announced Sunday morning by US Ambassador to the UN Haley. Trump continues to favor Russia for reasons nobody can fathom. Just as perhaps Trump said something to N. Korea to change its mind, maybe Putin said something to Trump to make him his poodle. There is a glimmer of a suggestion that Putin may have frightened Trump into a corner by threatening an oil price war... see below. It's a stretch, but if so, a powerful threat. Don't forget, Russia is in cahoots with the OPECE leader, Saudi Arabia, on controlling oil prices.

Secondly, Trump thinks he owns the stage, and sometimes he does, but the central player for financial markets is the central bank. This is a day for Fed speeches, again, and this afternoon we get the Beige Book. One set of headlines yesterday invites despair: "Fed's Williams sees U.S. inflation at or above goal for years. Fed's Evans sees little pressure pushing inflation beyond 2 pct."

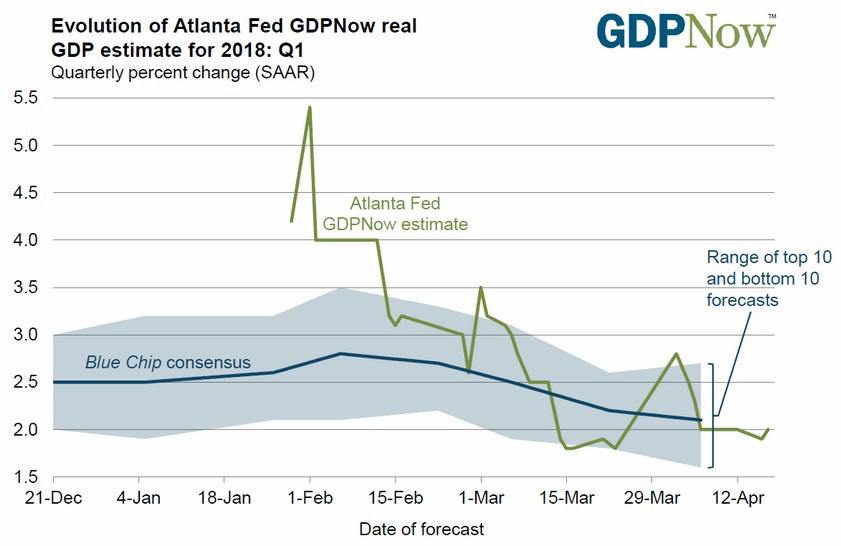

We continue to note the absence of genuine inflation or inflation precursors. The dog is not barking. We can start with overall growth. Yesterday the Atlanta Fed's GDPNow model raised the estimate of Q1 GDP from 1.9% to 2.0%, led by consumer spending and nonresidential investment. This does not promise inflation from growth exceeding capacity.

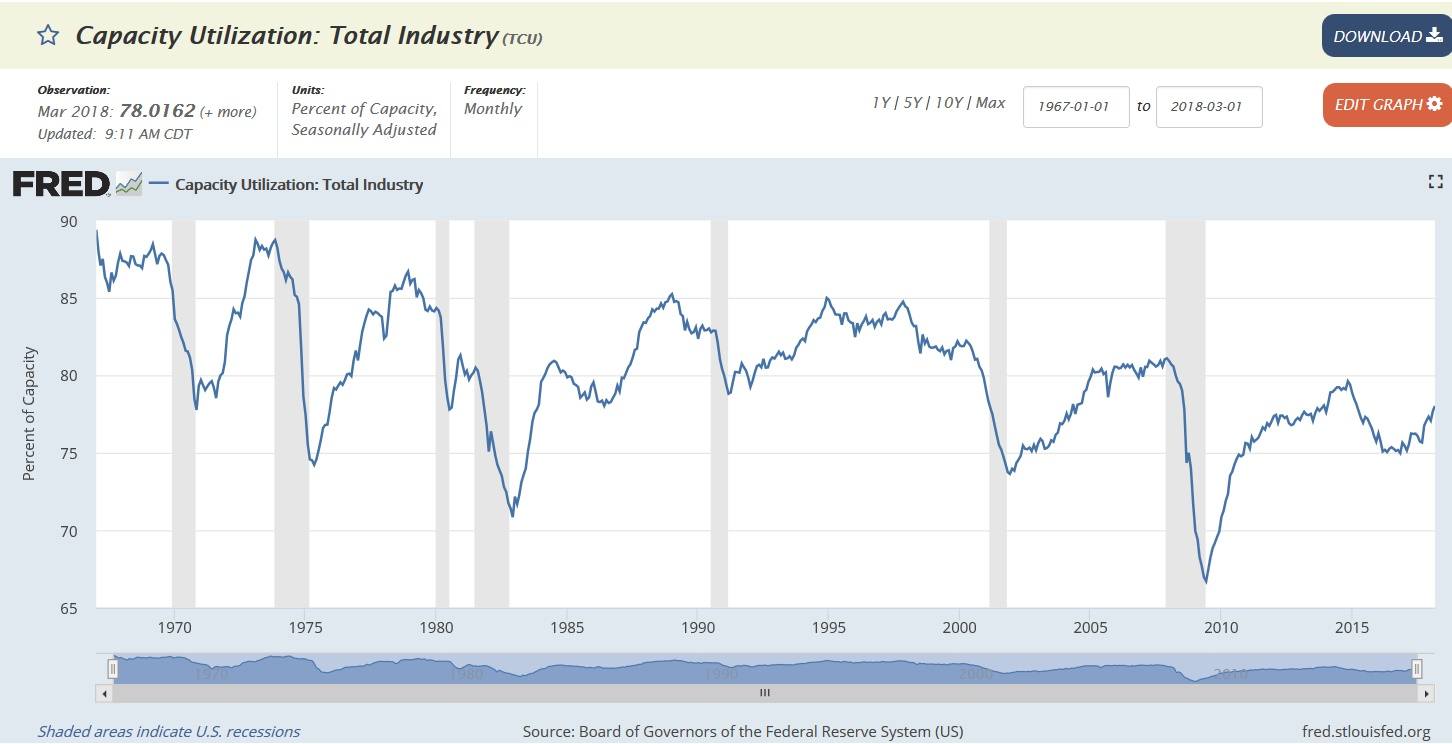

In fact, as noted above, yesterday's capacity utilization rose to 78% from 77.7%, a hair over the fore-cast, but still well under the levels seen in March-Nov 2014. See the chart. Lots of things push infla-tion but stretched capacity utilization is the most reliable one, and we don't have it.

In fact, check out the longer timeframe chart. Two points: capacity utilization has been falling since the 1970's. Can't blame China for everything. Second, look at utilization falling off the cliff in 1979-1980, when inflation was at its worst and Fed Chair Volcker torched Fed funds to nearly 20%. See the next chart if you don't remember those days! We were on the Fed funds desk at the height of it. It was excit-ing to be backstage but not if you needed the money/liquidity. How soon we forget.

There is another point here—at the same time inflation and Fed funds were soaring, and capacity utili-zation was tanking, we had the 1979 oil crisis. History books say the oil crisis was the drop in output caused by the Iranian revolution, but it was really the panic. Some sources say output fell by only 4-5%, at least initially. By the time of the Iran-Iraq war, which everybody has completely forgotten, oil prices had doubled.

We may live in different times, what with Saudi Crown Prince Salman instituting real reform at home and making a charm tour of the US, but market behavior is remarkably consistent... we may have in-stant news and data today that we didn't have then—oh, how we used to pay through the nose for news and data!—but we still possess the same lizard brain. It's never fight—it's always flight.

So if we get inflation over 2% as Fed Williams accepts, it won't be from stressed capacity utilization. It won't be from the Phillips curve finally delivering high household spending from wage gains, either. But it might be from oil scaring the pants off everybody. We could see hoarding and runs on toilet pa-per and Ritz crackers. Some people gave up expensive heating oil altogether and shifted to wood-burning stoves, now the chic thing but once a necessity.

This is not the scenario we believe. We are more inclined to see a gradual decline in activity punctuated by some bright spots (like housing), a change so gradual we barely notice it. But we fear oil price-induced hysteria. Or some other shortage blown out of proportion. Lithium, maybe. The outcome could be stagflation, low growth beleaguered by high inflation. Never has the Trump reflation trade seemed more desirable. And to be fair, the tax cuts have yet to kick in.

We really dislike the oil inventory reports... the API reports one thing and the Energy Dept reports something else entirely when they should be in sync. It's fishy. One of the two is doing a bad job of measurement or is lying. Yesterday the API reported all the inventories fell last week, crude, gasoline and distillates. Crude supplies fell by 1 million barrels, less than 1.4 million forecast. US crude imports were lower by 644,000 barrels per day to 7.9 million bpd. Oil prices fell but bounced right back this morning. We shall see that the EIA has to say.

What is the long-term forecast? Bloomberg sees $63.50 in 2019, $65 in 2020 and $67.50 in 2021. BMI just came out with a far higher forecast, $75 next year, rising to $78 in 2020 and $80 in 2021 and 2022. The basis for the rising forecast is "market rebalancing and strong sentiment-driven support." In the near-term, BMI sees stabilization as OPEC output cuts are obeyed and pushed out to Dec at the June 22 meeting, and US output fades a bit. Here's the key sentence: "We believe bullish expectations regard-ing US production growth are overblown due to a lack of readily available high-grade rigs and pressure pumping capacity."

Aha! It's not overall industrial capacity utilization that counts, it's capacity utilization in the US oil industry.

What if BMI is wrong... and we return to oil at over $100, as we saw only a few years ago ($107.13 on 2/21/11). We could be in the weird situation of looking to Prince Salman to open the spigot and main-tain prices lower than that. OPEC and Russia are due to meet in Saudi Arabia this week to talk about price stability, with the wider OPEC meeting June 22.

We like to think that the environment-damaging fracking industry in the US has given OPEC a come-uppance, but while OPEC suffers from all the problems of any cartel, chiefly enforcement of quotas, this time the quotas have mostly been obeyed. The US produces about the same as Saudi Arabia and Russia, and still imports nearly the same amount as it produces. OPEC has not lost its sting and is re-gaining power by the minute.

We could also be looking to Russia and the Saudis to prevent supply-disrupting war in the Middle East, especially in producing countries like Iran, Iraq and Syria. Nobody much cares if the Saudis obliterate Yemen, which has rapidly diminishing oil reserves, anyway. The balance of power is shifting to the Russia-OPEC camp. This may account for Trump's obsequiousness to Russia, although we hesitate to impute anything so sophisticated to someone so crass (who says thing like "I'm a genius.")

Bottom line, the bond market doesn't see inflation and doubts the Fed's resolve. Maybe the bond mar-ket should take a closer look at the all-too-real threat of oil-driven inflation. Again. Unless Trump pre-vails in making oil-price deals behind the scenes... but surely this is giving credit where none is due. Right?

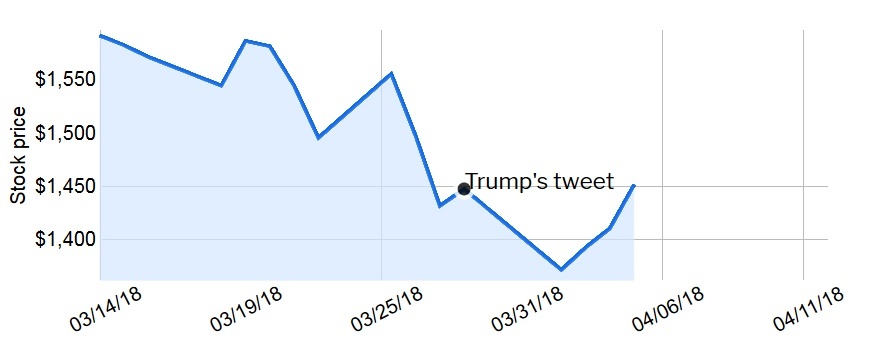

Tidbit: Time magazine offers a new feature—see how Trump's impulsive and informed tweets affect specific stocks, like Amazon. Go to time.com/tweet-stocks.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat