Rising oil amid an economic slowdown

Jeff Currie is the Global Head of Commodities Research for Goldman Sachs. He was recently on CNBC to talk about inflation. With regards to commodities prices, Jeff stated, “this is absolutely not a head fake. This is very different than what we saw in 2008. This is a molecule crisis. We’re out of many different commodities...it’s a lack of supply.” It has since been argued by some that in order for the economy to grow and to be able to service its debt, it needs to consume more energy and commodities. This, along with the lack of supply is going to drive commodities higher, and be the backbone of a new, secular inflationary trend. On the surface it makes sense, if the economy is going to grow, consumption of natural resources needs to rise, which will push prices even higher than they already are. As oil gets more expensive, it will pull along with it the prices of most other items as well. However, when you dig under the surface a little bit, you uncover some major holes in this analysis. First, real economic growth peaked in Q2 and is already slowing. If the economy is slowing, where is this implied demand going to come from? Also, what are the implications of rising energy prices amidst an economic slowdown? Let’s dig a little deeper and find out.

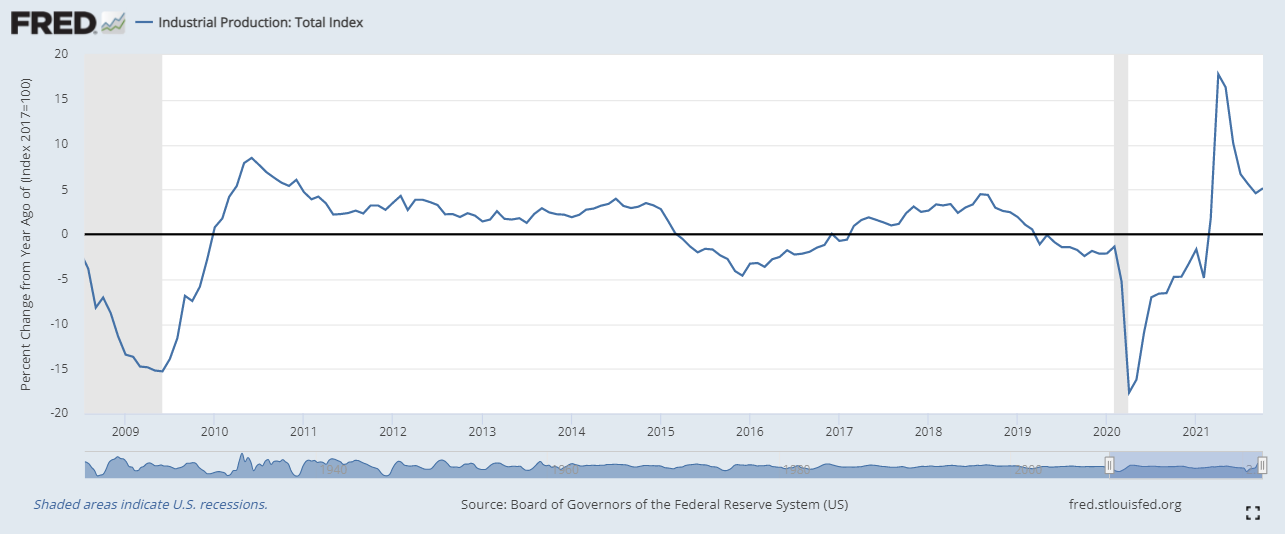

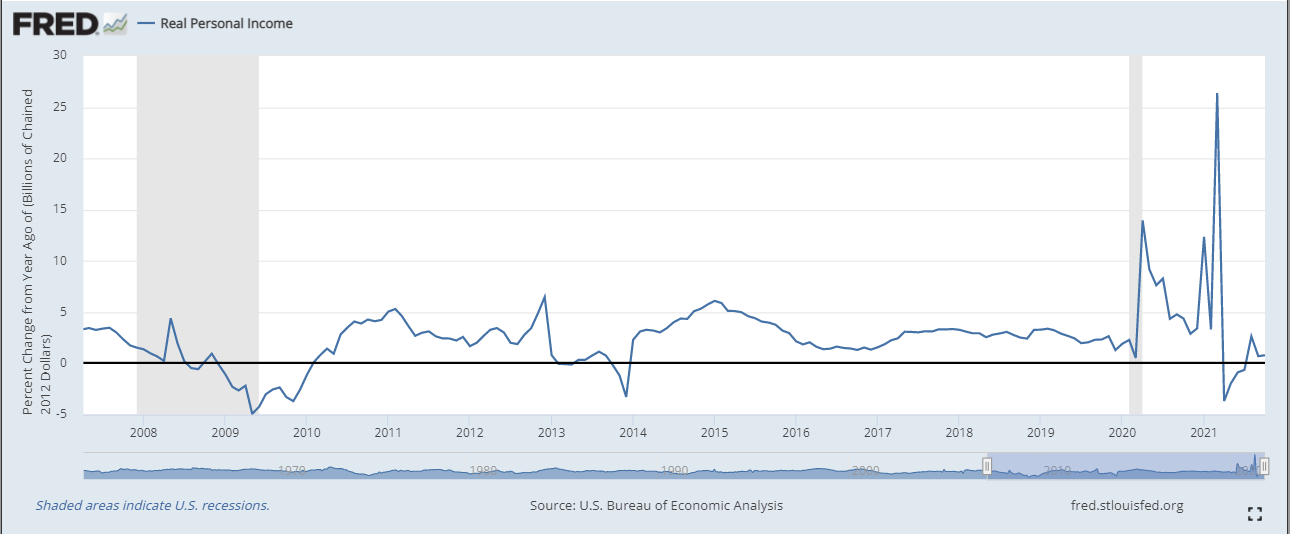

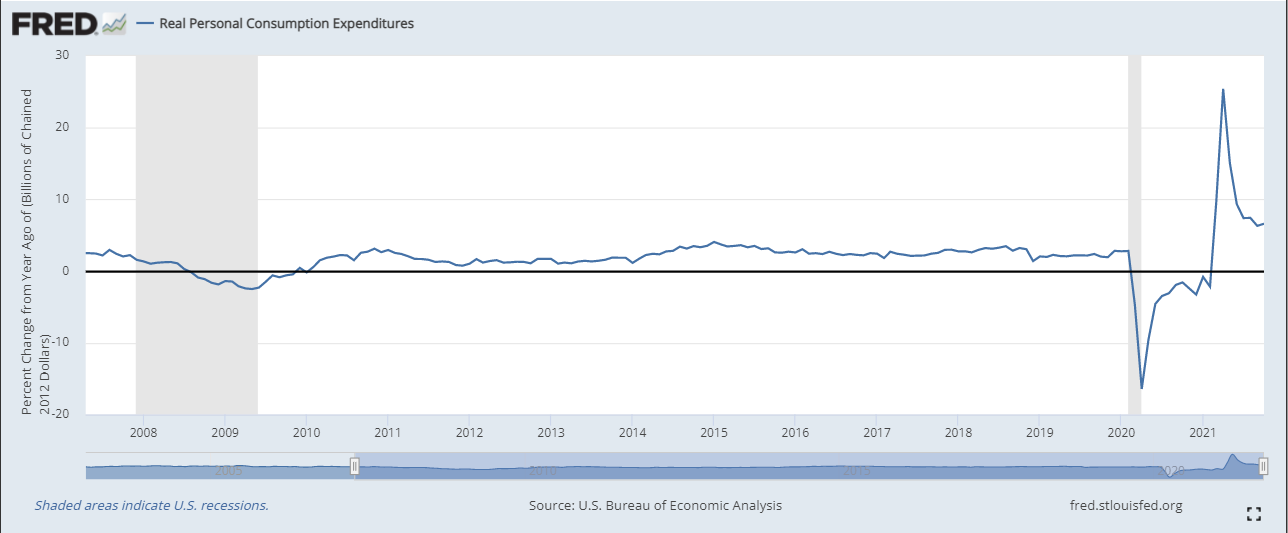

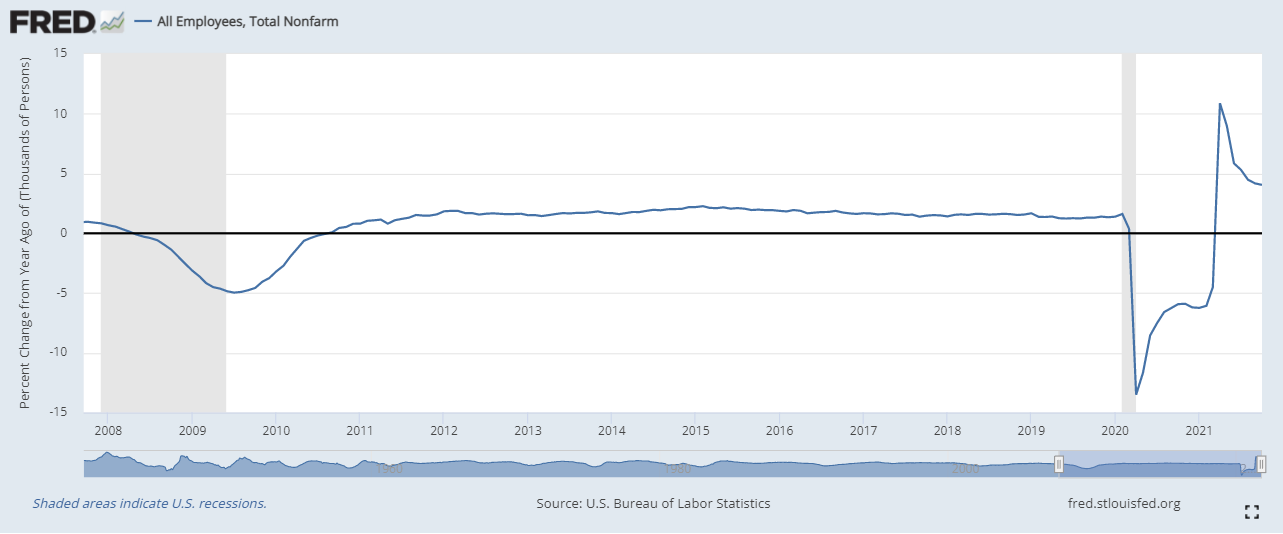

First, let’s take a look at the slowing economy from an economic perspective. Eric Basmajian of EPB Macro Research often talks about the ‘four corners of the economy: industrial production, real personal income (adjusted for inflation), real personal consumption (adjusted for inflation), and employment (nonfarm payrolls). If you look below, I have charted all four of these indicators. Industrial production, real personal consumption and employment peaked in April of this year, with real personal income having peaked in March. Since then, they have all been on steady declines, indicating a slowing economy.

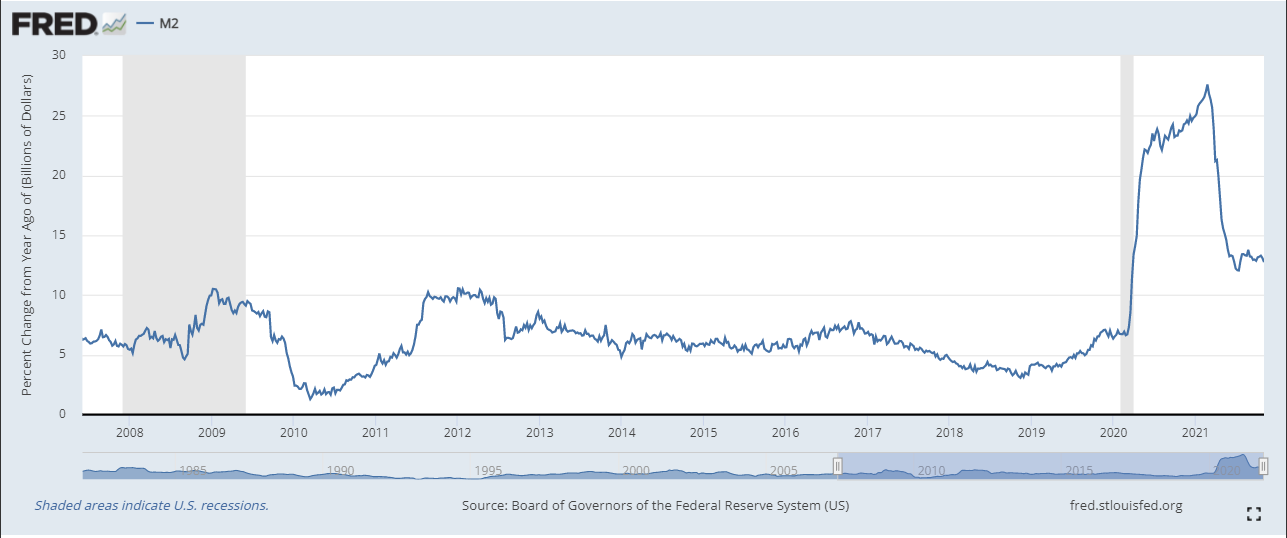

Even though industrial production is not a major component of US GDP, it can be quite volatile; therefore, driving fluctuations in GDP. Employment, real personal income, and real personal consumption provide us with a quality representation of the private sector. Since the private sector drives the economy, if these sectors are slowing, so too will the economy. We can also take it one step further and look at the M2 money supply. Now, if you have read my articles (article 1 and article 2) on the money supply, you know the money supply metrics are NOT a good measure for determining the actual supply of dollars. However, since the M2 is mostly made up of domestic depository accounts, it can give us a good idea if money is flowing into the accounts of consumers. If so, we would expect private consumption to rise, if not, we would expect it to fall. If you look below, I have a chart of the M2, which peaked at the end of February, preceding the slowdown by a couple of months. Since there has been a sharp decline in not just the M2, but in personal consumption as well. Combine the declines in the ‘four corners of the economy with the decline in the M2, and we have a clear economic slowdown on our hands— one which has shown no signs of picking back up.

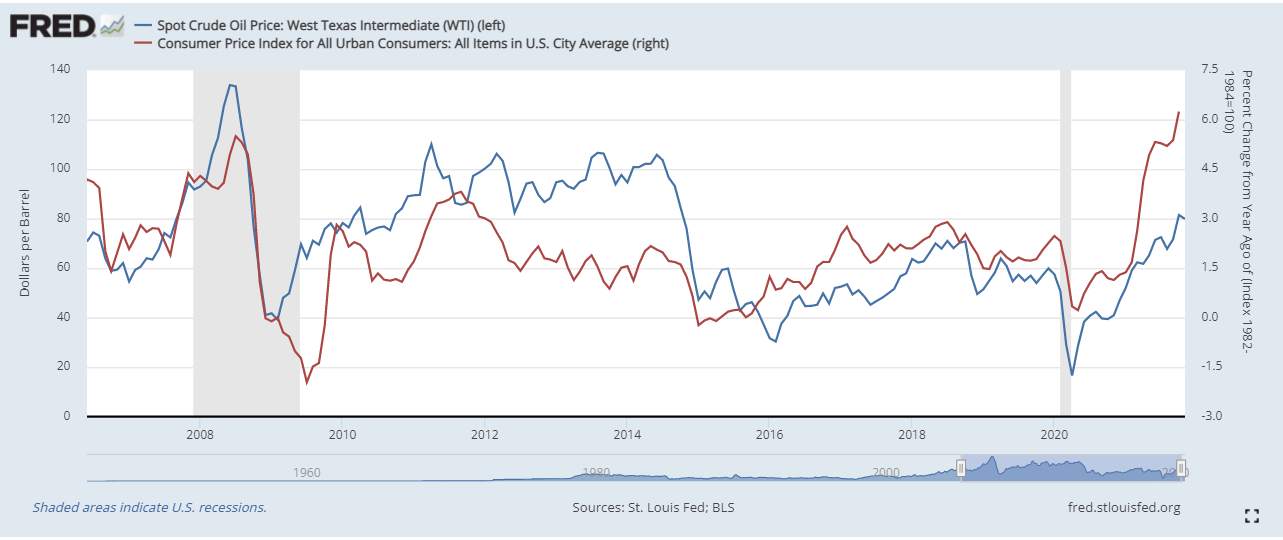

This is where oil comes into play. Oil is the most sought-after commodity in the world. It is needed in various ways, for various industries that drive the global economy. Because it is so widely used, its price influences the prices of various other commodities, products, and services. So, if oil is rising sharply (like it has been), then we should expect it to pull up the prices of other goods and services. If you look below (first chart), you will see oil alongside the CPI. They have moved alongside of each other very well since their bottoms back in April 2020. Now, oil has pulled back in the last few weeks, but from a technical perspective, it is still clearly in an uptrend because it has not broken below its pivot low (second chart below).

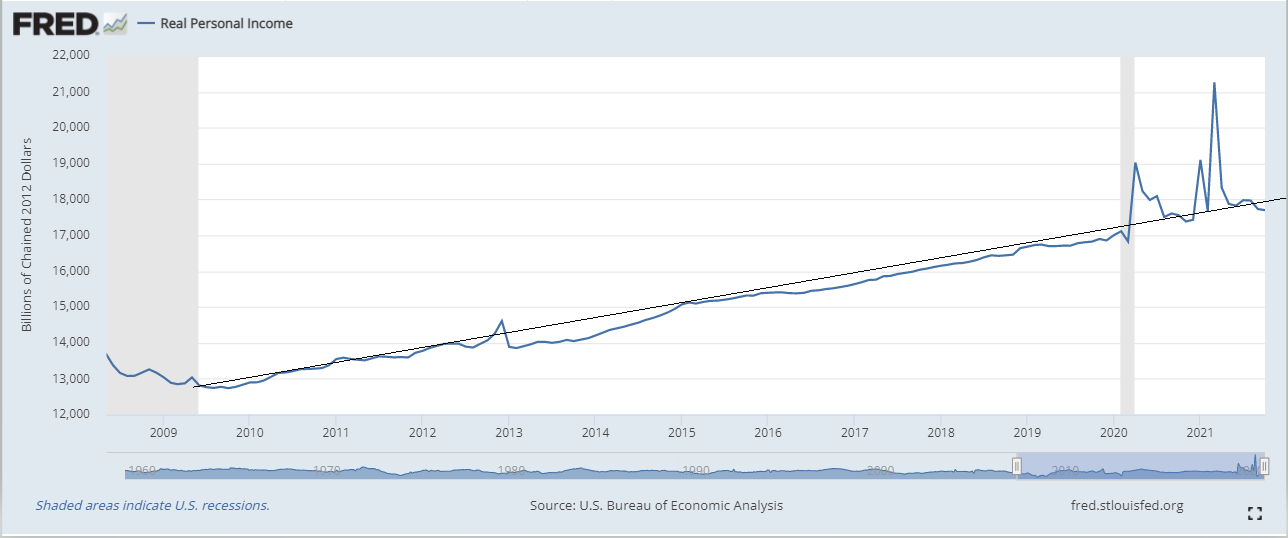

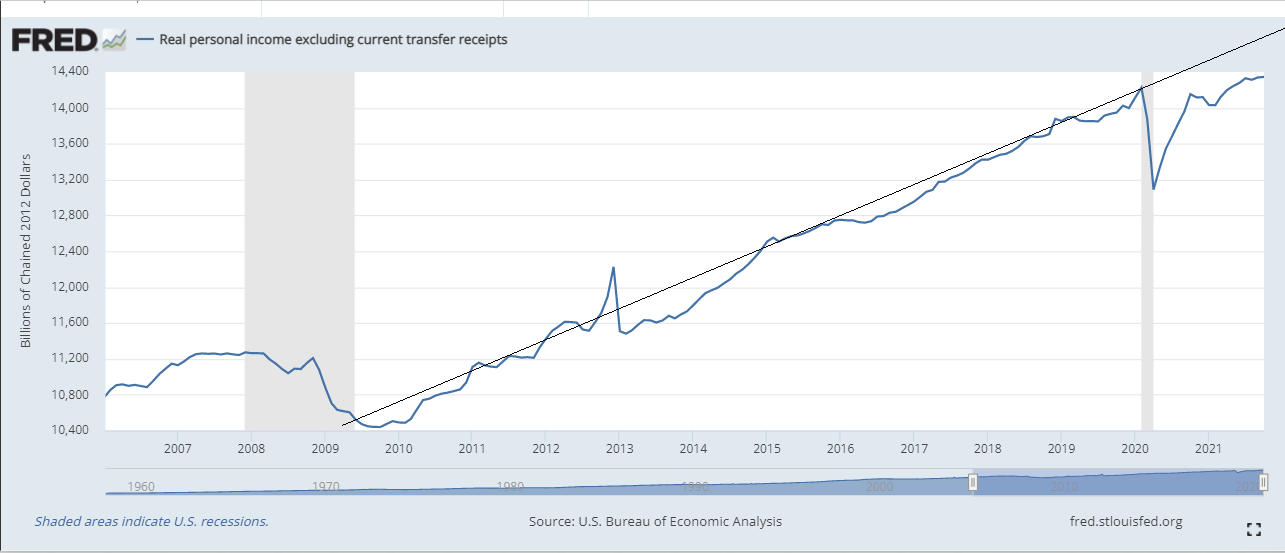

Now, the question remains, if the economy is slowing, where is the demand going to come from to fuel economic growth and a consistent rise in energy, and thus, inflation? Many are overlooking this aspect. Because as it sits, it is very clear that rising energy prices are fueled by supply chain bottlenecks (along with other commodities) and OPEC’s (Organization of the Petroleum Exporting Countries) hesitancy to increase oil production by any significant amount (OPEC did meet yesterday and today to discuss production output, so watch out for any developments there). With elevated inflation levels, as the economy slows, real incomes will continue to fall, and if energy prices continue to rise, it is going to have serious economic consequences. Let’s take a closer look at real incomes, because with falling real incomes, higher consumer prices cannot be sustained. Real personal income in the chart above was on a year-over-year basis. Now, let’s take a look at the bigger picture. Below (first chart), you can see that real personal income has fallen below its post-GFC trend. Real income is nowhere near its pre-GFC trend, that’s why I am specifying its post-GFC trend. This chart INCLUDES government transfer payments (social security, unemployment, stimulus checks, etc.). Despite all the additional debt, the government has taken on, the additional unemployment checks, and stimulus checks, real personal income is still below its trend. Now, if you look at the second chart below, I have real personal income EXCLUDING government transfer payments, and as you can see it is even further below trend than real personal income including government transfer payments. So, I’ll ask again, where is the demand going to come from to boost growth and keep inflation levels elevated long-term? By now, some of you my be screaming, “the Fed! QE! Money printing!” But, we already know that the Fed is not printing any money. I will not get into that here because I already did extensively, here.

As energy prices and inflation rises, the economy slows and real incomes continue to fall, it is going to further hamper demand. Energy is a major monthly cost for consumers. If energy prices are rising (causing other goods and services to rise too), with falling real incomes (reduced purchasing power), consumers are going to be forced to reallocate capital to non-discretionary purchases like gas and food, pulling spending away from discretionary goods and services, like durable goods and entertainment. Depending on the rate of change of rising prices versus falling real incomes, the reallocation of spending from “unnecessary” items towards those that are, will at least somewhat offset the inflationary impact of rising energy prices. More importantly than that, as this trend of rising oil and higher consumer prices continues while growth is slowing, causing real incomes to fall, it is going to continue to pull capital and resources from different parts of the economy into a narrowing funnel – only purchases that are necessary. I have only been talking about consumers, but the same will hold true for businesses as well. As the economy slows, businesses will not be able to pass along the entire increase in prices, because consumers will not be able to afford it due to their reduced purchasing power. That means businesses will have to absorb at least a portion of the higher prices, hurting their bottom line. Because of this, wages will not be able to keep up with inflation, so expect real incomes to continue to fall.

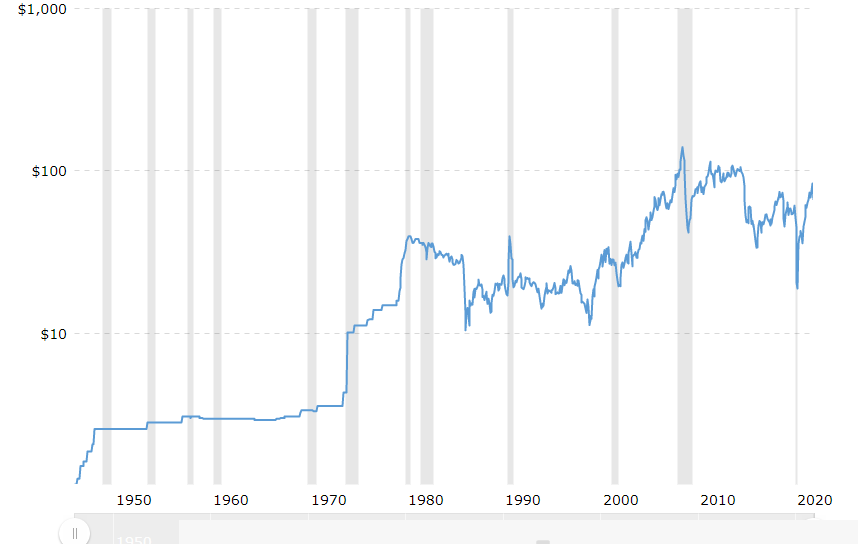

Rising oil combined with a slowing economy never has good outcomes. Yes, I know, this time is different because of X, Y, and Z. It is always different. But, for historical context, I do not think it is a coincidence to see rising energy prices just prior to most recessions. Look below, I have the price of oil dating back to about 1946. Nearly every recession (shaded gray area) is preceded by a sharp rise in oil. Energy prices seem to lag quite a bit, meaning they are still rising while many other indicators like bond yields and the ones mentioned earlier in this article are pricing in an economic slowdown and/or recession, sometimes a year or more in advance. Now, I am not saying rising energy prices necessarily cause recessions, but there is a very clear and strong correlation between the two. However, I think it is more than fair to say that rising energy prices, especially as economic growth is slowing, is definitely a contributing factor to the cause of a recession and/or to the severity of it. In 2008, oil got to its highest ever price of almost $150 a barrel, and it was followed by the worst economic crisis since the Great Depression.

I am not suggesting that an economic crisis will happen tomorrow, because oil and inflation could certainly run a lot higher over the coming months, because supply chains still need time to work themselves out. The problem is, without economic growth to absorb these higher prices, they cannot be sustained. Something will eventually give way, and when it does, expect a sharp decline in energy prices as well as consumer prices, and a potentially nasty recession. If 2008 is any indication, it would appear that the higher the price of oil goes, the nastier the recession will be because the higher it goes, the higher it pulls inflation with it, causing more and more capital and resources to get plucked from other parts of the economy, further hampering growth.

Author

Ryan Miller

Ryan Miller Trading Economics

Ryan Miller received a Bachelors Degree in History from William Paterson University. Through his studies of U.S. history, he developed an interest in the implications the financial markets have on the economy.