Rates spark: Injecting some volatility

/stock-market-graph-gm523786073-51379002_XtraLarge.jpg)

A hopeful read on Chinese headlines, strong data, and still hawkish central bankers are keeping rates markets on their toes. Injecting market volatility is not the end all and be all of a central bank’s policy tightening, but an unavoidable consequence that should pressure riskier bonds wider.

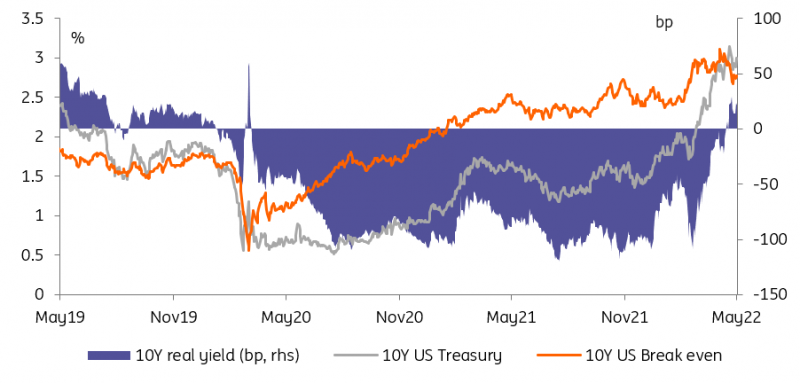

US real yields on the rise again

The US 10yr is back within touching distance of 3%. No big surprise here. The driver remains the real yield, which is back up to the 25bp area in the 10yr. Inflation expectations have also made a contribution, albeit moderate, and are settling in the 2.75% area. The direction of travel is for the 10yr real yield to continue to trek towards 1% in the next number of months, maintaining upward pressure on traditional market rates.

10Y real yields are back above 20bp

Source: Refinitiv, ING

Inflation expectations don't need to do much initially, which will result in net upward pressure on market rates. But ultimately inflation expectations should come under downward pressure if real rates really do continue to motor higher. We'll get a bit of a near-term steer on this from Thursday's 10yr TIPS auction, (following today's 20yr conventional auction). As TIPS pay a real yield (plus inflation), there will be a direct reference to the drivers noted above.

The front-end wakes up again, with Europe in the lead

A conjunction of factors has allowed global rates to resume their rise. Stronger than expected UK employment data had markets re-think the amount of cooling down the Bank of England needs to achieve to get inflation back on target, and another barrage of hawkish European Central Bank comments had the EUR front-end re-price higher too.

As we discussed in yesterday’s Spark, Europe hasn’t yet seen its ‘peak inflation’ moment, so it would have been surprising for central bankers to step off the brink already. The tightening of global financial conditions suggests their strategy is working but the bonds rally seen last week confirms that central banks need to deliver on near-term hike expectations. This is more obvious for the ECB which likely won’t hike before July, while the BoE has hiked four times already.

Rates volatility and the compensation demanded by investors (yields) continue to climb

Source: Refinitiv, ING

To be fair, one shouldn’t understate the importance of hopes that lockdowns in Shanghai may be nearing its end. This has allowed global-growth sensitive Europe to look to a less gloomy future, and helped 10Y Bund yields test the 1% level once again.

Volatility is not the end goal, but an unavoidable consequence

This also lent some credibility to hawks piling pressure on front-end rate markets. Knot was the latest ECB member to flag the possibility of 50bp hikes, although his base case remains for a 25bp move in July. We wouldn’t dismiss the relevance of this comment as a fringe idea (so far only mentioned by Robert Holzmann and Klaas Knot, both well-known hawks). They confirm that the odds of a 50bp hike is low but higher than 0%, which in turn means that markets will increasingly consider 25bp hikes as a minimum.

More broadly, if the comments aren’t rowed back, this should inject an additional dose of volatility in broader EUR financial markets. The debate around 75bp hike increments at the Fed was an instructive one. It seems to matter a lot whether a central bank is on a tightening course set in advance, or if investors are left to guess the degree of tightening that will be implemented on a meeting-by-meeting basis.

Rates direction is converging but curves are diverging

Source: Refinitiv, ING

We do not share the (slightly sadistic) idea that injecting volatility is the end all and be all of a central bank’s policy tightening… but it can be helpful to keep markets cognisant of the risk of faster hikes should inflation fail to cool down. More to the point, we reiterate our view that it is too early to expect central banks to leave markets off the hook. This should translate in a shaky performance of the riskier corners of rate markets (eg peripheral bonds), and continue jolting yield curves between flattening and steepening phases.

Read the original analysis: Rates spark: Injecting some volatility

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.